Hello All,

22th sep AGM of virat

any one is going?

Amit

Hello All,

22th sep AGM of virat

any one is going?

Amit

has anyone attended the AGM . pls give sm inputs if any.

http://investr.co.in/chart.html?id=9926

Observe that their topline has been falling for the last 4 qtrs. That could be the reason for the fall in stock price.

This company hasnt gone anywhere in the past few years and i suspect their future prospects are no better. This despite the fact that they are in a great industry which is in desperate need of a good player. Happy socks have proved that; they came in and have been able to build a brand in a short period of time. Their socks at 400/- per piece are still quite expensive and there is clearly a space for a company with a good quality product in the price range of 150-400.

I dont think Virat Industries is that company. Their promoters are investing in buying Ola Cabs and are clearly not aware or not interested in scaling up their existing business - http://www.thehindubusinessline.com/news/director-by-day-driver-by-night/article9086407.ece

Which is a shame given the potential of this business

Hello All,

Virat’s capicity utiliztion is 94-95%. and no plan to any expansion

Mgt is very very conservative

Amit

Sales highly increased to 9.19 cr in June’17 quarter. Company installed latest machines and spent good amount for CAPEX in FY17. Is it due to increase in the volume/price (which is a good thing for the company) or any one-offs?

The promoters are consistently selling shares in the markets… That is a

worry…

not consistently ,they have sold less than 1% and that is after july 2017. before that if i recollect they increased their holding from @32% (2006-7) to 49% (2017).

promoters just like us may have different needs(so selling by promoters shouldn’t be reason to ignore stock,it may even be opportunity to buy sizable qty.) we already have examples of page and eicher where promoters sale is followed by good rise in price due to business fundamentals.

near term earning are under pressure due to exchange rate (INR appreciation) while business fundamentals are improving(sales improving due to new investments.

good domestic business traction is visible and may continue

till date promoters are shareholder friendly and have maintained good clean balance sheet with no debt and good dividend payout.

last but most important valuations at cmp of 125 it is available at PE of 15 (assuming normalized EPS of 8 Rs.and dividend yield of 2%)

disc: hold as tracking 1% position.

Lord Walker Socks , brand of Virat Industries is available at the outlets of a premiun store Jade Blue. Jade Blue being a premium Mens Fashion Store keeps only Premium Products , which implies Lord Walker is one of the finest quality socks. Topline for 9MFY18 is at 27.32 crs compared to FY17 entire year sales of 25.66 crs , hence it is safe to assume a 30% increase in the topline YoY.

Having such a low base , i feel scalability is huge and with such sound fundamentals and a strong and clean balance sheet , can be a multibagger in the for sure.

Disclosure : Invested

Anyone know what is happening with this company? FY19 has seen major decline in revenue from 36cr in FY18 to 24cr in FY19.

Hi

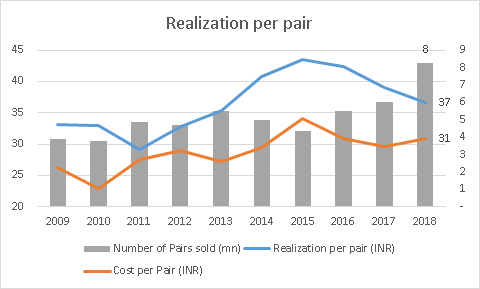

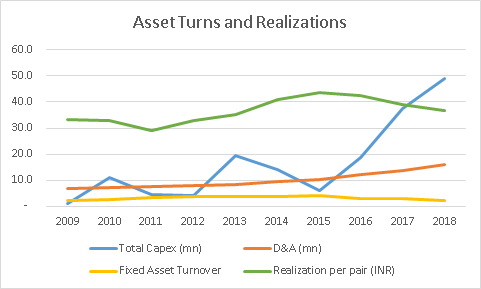

Looked to be an interesting play with domestic branded foray as well getting into into supply of niche football socks. However, their realizations per pair have not matched management commentary -

Company’s major margin drivers are fluctuations in exchange rate, export duties and changes in RM costs, all of which cannot be passed on to the customer, since Virat competes with companies from Bangladesh, China and Turkey, who all have different movements in exchange rates, RM prices and duties (eg. Turkey and Bangladesh have no import duties in EU). Its customers source socks from the lowest cost producers who meet the quality parameters.

Virat Industries is similar to BRKs initial textile business. The benefit of all the capex on technological advances eventually went to the final customer as the commodity nature of the product negated differentiation, while the business swallowed cash as the entire industry continued to upgrade to the newest equipment.

in virat’s case too -

you can read the entire thesis here -

2019 AR would be an interesting read considering the significant changes in company’s fundamentals -

| Year | 2016 | 2017 | 2018 | 2019 | Decline |

|---|---|---|---|---|---|

| Sales | 258 | 257 | 341 | 241 | -29% |

| PAT | 30.4 | 35.2 | 34.7 | 6.5 | -81% |

| Share Price | 95 | 130 | 176 | 59 | -67% |

Pretty interesting development happening in this company. Bhavook Triphati seems to be merging his company with Virat Industries. Also he already owns close to 25% stake in it.