Most companies has dedicated thread on Valuepickr but here’s quick thesis

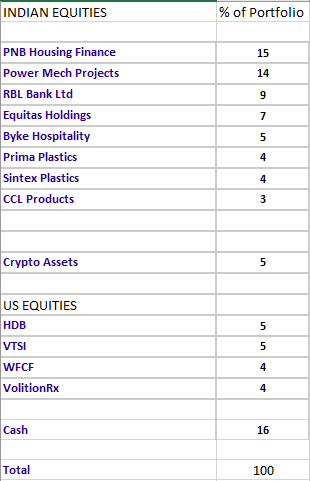

PNB Housing Finance : 35-40% Grower with decent management in good sector. Decrease in cost/Income ratio will help boost ROA.

Good Industrt Tailwind with subsidy on interest, tax benefit, RERA, etc.

Downside - With too many players, it has been competitive and RBI also raised concern on housing finance.

Power Mech Projects : Earlier company was hit badly due to overrun of domestic projects. All those projects are closed now so margins in domestic business will improve. They started getting decent international business with great margins too.

Increase in high margin projects along with 15-20% sales growth, this company can still surprise positively.

RBL Bank : 35-40% compounder with good management. After exiting from IndusInd bank due to size, I needed another compounder to replace. That’s when I found this gem. It’s buy and forget stock.

Equitas Holdings : Good Management with decent growth. Management smartly increased non-MFI [mainly secure lending] business in last 2 years. MFI book is 28% of book and will decrease to 20%. Focus is on increasing secured lending. Market is not valuing this business properly - Just look at valuation of other SFBs focused on secured lending.

It shall grow at 35-40% book for next few years with low opex ==> Decrease in cost/Income ratio and hence profit shall increase disproportionately.

Byke Hospitality : Quality company with decent management and valuations. Only Challenge is growth. Management kept on targeting higher number of properties, rooms through leased or franchise option. Somehow it didn’t work out well so far - Hopefully with turnaround in hospitality sector, they find their mojo back. I am ready to give some more time.

Prima Plastics - I allocated decent money on this one at Rs.50-55. This was also part of bull run and crazy valuations as part of small/midcap frenzy cycle. I sold majority part of portfolio - reason to keep small allocations is their big expansion in Cameroon and India.

They ended with very high Inventories and debtors along with debt. That’s risk along with oil prices

Sintex Plastics - Management had been working hard to restructuring business and focus on retail and high margin products.

Cutting down on infra business, paying down debt, increasing retail products. These will help increase bottomline. Decent sales growth of 15% can have magnifying impact in bottomline. With increase in EBITDA margins and decrease in interest and dep. expenses, bottomline is bound to grow much higher. Management subscribed to warrants at Rs.90 so their incentives are rightly aligned.

It’s huge bargain if they walk their talk.

CCL Products - Good business and good management but okay valuations.

New capacity addition, increasing margins, focus on building domestic brand and above all this is STICKY business and very hard for customers to switch.

This one still forms 3% of portfolio as I am not convinced fully on valuations.