I guess - exiting HOEC is to do with softer crude prices and headwinds due to potential higher US production in Trump’s leadership?

Do you see in longer term the exploration expansion not going to over smart the decline in crude prices?

I guess - exiting HOEC is to do with softer crude prices and headwinds due to potential higher US production in Trump’s leadership?

Do you see in longer term the exploration expansion not going to over smart the decline in crude prices?

Hi Vikas, the only moat is the network already built up as I understand it at the moment. Infollion has a strong set up already and is in an industry that is growing fast. This will be an execution heavy business and thebunit economics are beautiful.

I have not exited HOEC, it is around 5% of the PF - you’ll see it at the bottom end of the list. I do see softwr crude prices structurally but this is offset with India’s push to want higher local crude production. The north east gas pipeline will be thebmajor trigger for HOEC.

T&D is in a massive upswing as a sector, coming out of a long lull period which put players like Jyoti Structures in a very rough past few years. They have high competence in the sector having done a lot of major projects in the past. Fresh fund raise will allow them to capture the industry tailwinds and hopefully imprve their balance sheet. Playing for an improvement in fundamentals and associated rerating.

Hi Vineet,

Thank you for sharing, we’d connected earlier on Twitter as well.

What are your views on Geekay? I’d gotten lucky and ridden a solid wave long back till 100/110 and sold the stock early this year. I’m seeing its been consolidating ever since.

The reason behind my selling was that when I’d attended the AGM last year (and I believe the broad tone was similar this year as well) that management is a) not communicative b) even in AGMs doesn’t give full responses c) have likely found a small niche and are not too keen on growing. Another reason was this ASP loan on top of the inherent risk of owning such a small company was becoming a bigger red flag.

So just wanted to hear your thoughts on why you’ve had a stable position in Geekay.

I’ve started looking again after I noticed the price consolidation has still continued for almost a year and the stock looks like reasonable value at current levels and could start moving again if some growth triggers kick in.

So the number of shares I have of Geekay is just 20% of what I had when I first build my position pre-split. I sold out of 80% shares on the way up till 120 and continue to hold the rest, such that the % allocation in the portfolio remains at a 5-7% range.

Sold for exactly the reasons you mentioned, held some for exactly the reasons you mentioned as well. It is quite cheap compared to other companies in the galvanized wires, nuts and bolts, and the capital efficiency has been very good historically so I am ok to hold at these valuations, assuming that the unit economics will not deteriorate. There has been some growth capex and volumes have grown too. With metal prices stabalizing and maybe unching up with the China economic push, there can be better realizatiins which will boost both top ajd bottommline.

Hi all, apologies again for missing to post the December updates. Here they are, and I’ll post the January updates separately as well.

Here are the updates for Jan. PF is around 5% from ATH. Some changes last month as opportunities presented themselves. Have a lot of undeployed cash from salaries over the past few months which ai will deploy over the next couple of months.

What about the staggering debt?

I agree with your analysis, and the stock does look promising for the long term.

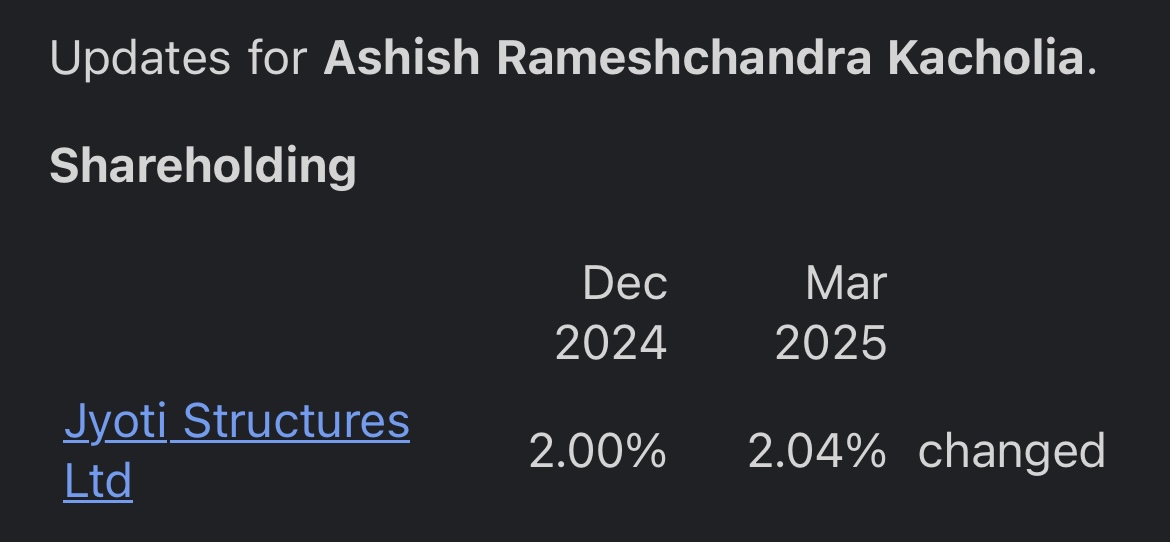

Even ace investor Ashish Kacholia has increased his stake from 2% to 2.04%.

What are your thoughts on this massive debt? I don’t even see them paying interest.

Apologies if this topic has already been discussed.

Vineet has already exited from this scrip.

I am aware still asking, need his view point on this.

They have said that they are in discussion with lenders for a one time settlement. Also, they received a couple of big orders recently. But their receivables are so high and operating cash flow is negative. That gives much less confidence to invest in this scrip. I’m still invested and at a notional loss.

Well summed up. Their silver bullet will be if one of the large receivables is received, which apparently they are working on. But with the capitulation in the markets over the past couple of months, a lot of much better quality companies became very cheap and so I sold out of the ones that had more risk and high debt, like Jyoti and Gensol to concentrate into higher quality.

I update a lot more regularly on X, almost after every major transaction.

This is driving my appproach in the markets now. I have sold off long levered positions (HDFC Bank and Bajaj Finance), sitting on some cash and waiting for some clarity to emerge. Holding on to the rest of the portfolio.