Like you said,there are no free cash flows.Difficult to put money in such stocks .

The company holds Birla corp, universal cable and mutual fund investments which is worth 2300 cr. At 70% discount, its value is 690 cr.

If we value EPC business at 12 P/E at an EPS of 83 (FY2018), it worth another 1000 cr.

Hence 690+1000 = 1690 cr. But market cap of VTL is 1180 cr.

Today it rallied 20%. Is it a pre-result rally? Q1 results will be reported tomorrow.

It may be due to its subsidiary, Birla Corp reporting yesterday a 94% increase in PAT.

Anyway VTL is undervalued as it holds investment worth 2300 Cr in Birla corp.

1 Like

Vindhya Telelink has come up with very good results. Whether growth sustainable?

1 Like

Their annual report is extremely upbeat and they are playing big on surge in OFC demand in this country.

And forgetting everything, it’s still trading at P/BV < 1.

Vindhya Telelinks has appreciated by almost 30% in last 3 months. Is it then a possible multi bagger?

I doubt, reasons:

a. It’s part of MP Birla group. They used to do well some 100 years back. The group companies growth seem jaded and tired now.

b. Cash FLow is negative as per AR 2017.

Even though it might have appreciated by 30% in last 3 months but it doesn’t qualify to be a probable multibagger.

So Vindhya Telelinks may spurt by 30% in 3 months, but it can’t continue to keep creating wealth for it’s shareholders. Views invited.

I thought this is the Annual Report (AR): http://www.vtlrewa.com/pdf/Annual-Report-2017-18-VTL.pdf

AR for 2018 will be released next year, right?

@pbd Thanks for correcting me- there was a mistake from my side.

I am going to update the post.

No one has mentioned it yet. Crisil released their rating report. Highlights from their rating rationale write-up:

Strengths:

- Company has a strong market position in the optic fibre cables (OFC) industry, and is among the top three players in India.

- The group has strong order book, diversified revenue, and a healthy financial risk profile.

- Their EPC segment undertakes turnkey projects for them and has set up distribution lines for state power distribution companies.

- The EPC division grew by 14% fiscal-on-fiscal in 2018

- The cables division grew by 78%.

Risks:

- Large working capital requirement.

- Vulnerability of its profitability to volatility in raw material prices and foreign exchange rates.

- Exposure to risks related to the tender-based nature of the business.

Comments on financials:

+---------------------------------+----------+--------+--------+

| Particulars | Unit | 2018 | 2017 |

+---------------------------------+----------+--------+--------+

| Revenue | Rs crore | 1351.3 | 1026.5 |

| Profit After Tax (PAT) | Rs crore | 153.4 | 170.0 |

| PAT Margin | % | 11.3 | 16.5 |

| Adjusted debt/adjusted networth | Ratio | 0.87 | 0.69 |

| Interest coverage | Ratio | 3.75 | 3.76 |

+---------------------------------+----------+--------+--------+

Revenue is expected to improve over the medium term on account of healthy demand prospects in the OFC and EPC segments. The group had orders of Rs 4,131.44 crore as on June 30, 2018.

Thanks.

courtesy: screener.in

Good numbers… are we ready for another spike or million dollar question is that how long it will survive

VTL is an MP Birla group company (now Lodha’s) which started manufacturing Jelly Filled Telecom Cables at Rewa MP in 1986

You can take a person away from Data but you cant take Data away from a person ! VTL is a proxy consumption story for data consumption via mobile phones, gadgets, TV etc etc in India.

OFC serves the need to transport this data from cellular companies to the final user. The India user is always looking for faster speeds as most data is being replaced by videos from pictures earlier

Only 20% of the cell towers are linked with optic fibre cables in india. The bal 80% work on mercury waves(old tech). If India needs to move to 5G then mercury waves will not be able to support this 5G. OFC’s will HAVE TO be deployed

in order to take the full benefit og 5G. This will mean huge capex spend by Telecom companies on back haul and last mile connectivity. 5G will boost OFC consumption by 6x from the current capacity available.

Even if Voda, Bharti and JIO INCREASE DATA rates and leave calling free the Indian Consumer who is now ADDICTED to data will pay up even if his bills increase by 20-30% from the current tarrif’s

DATA CONSUMPTION IS SOLVING THE LONLINESS PROBLEM IN INDIA

Today VTL is a leading manufacturer of

Optic fibre cables with a capacity of 1,89,000 cable km’s

Solar E Beam cables

Railway signalling and Quad cables used in Railways

Copper magnesium based Catenary wires used for railway elctrification. The govt has mandated that IR becomes fully electrified by 2022

EPC Business

VTL is a unique EPC player and not a conventional one. This is because VTL not only lays OFC’s and Power Cables for companies but also has 27,000 Kms of its own fibre spread across 12 states that Telecom companies use at 99.90% efficiency

VTL has the destinction of rolling out 7500 Kms of OFC for defense much ahead of its peers.

The company has built 40,000 route kms in difficult terrain like China, Bhutana and Nepal.

The company has arso emerged successful bidder in 9 pro.lects of Government of India,s ambitious BharatNet Project for supp ry / rayingof oFC Network over 35000 Route KMs.

lhe lgmnanr is equally strong in executing energy distribution/sub-transmission and rural electrification, etc. projects rnainry invorving streJgthening of existing distribution network, augmentation & installation.of power transformJrs, conlstruction oi new linbs, etc. The revenue from energy verlical in_Epc business segment formed a signifi"a;t pun-oi,o,ut revenue from operations of the Epc business segient’during tlie Firiancial vJ* zors-ry. Going.forward, energy vefiical is expected to Jontribute substantially in the re,renue from operations of the company given strong order book of around Rs.15b0.00 crores besides emerging successful bidder in tenders woith about Rs.5g0.00 Crores.

Increased requirement of OFC’s in Defence

Another initiative by GoI is the Network for Spectrum (NFS) project. The increased demand for connectivity has led to the massive growth of the telecom sector. In terms of leveraging these requirements GoI decided to release 150 Mhz of spectrum for defense sector. The ‘Network for Spectrum’(NFS) project, by Bharat Sanchar Nigam Ltd (BSNL), was envisaged to build a new communication network for exclusive use by the armed forces in lieu of the spectrum. This project will consume huge volumes of specialty optical fibre cables. This project will also involve some offtake of optical fibre cables for its continuous operation and maintenance purposes in the coming years. Seeing, the determination of the GoI towards projects such as Digital India, NOFS and NFS, we can be sure that there is going to be a great demand for optic fibres and other cables in the future leading to greater revenue for the Co.

After the boost of 4G now comes 5G

Due to sudden outburst in telecom services, all private sector telecom service providers have upgraded their networks to offer high speed 4G telecom services. This change in the telecom industry allowed the high usage of OFC. Also growth in telecom infrastructure will be driven by a mix of operator-led-demand and public sector investments. Thus The roll out of 4G technology has boomed the requirement of optical fibres thereby paving the way for construction of futuristic network which is capable of handling new generations data centric applications. The planning for 5G technology is already underway and will be introduced in telecom ecosystem in 2020 thus multiplying the usage of optical fibre cables by 6 times.

FTTA IS ALSO EXPECTED TO INCREASE THE DEMAND FOR OFC

The requirement for specialty optical fibre cables which are to be used in ultimately connecting the antenna position in the cell sites with the base stations has been gradually increasing. This clearly shows the inherent quality of optical fibre in providing unlimited bandwidth capacities thereby necessitating its use even in final access network. This entire ecosystem is under the name of Fibre-to-the-Antenna(FTTA). The use of Copper telecom Cable is diminishing very quickly and is getting replaced with Optical Cable Fibre

FTTH IMPLEMENTATION TO AID TO EXISTING DEMAND - JIO announced another 20,000 Cr capex on this on 18/6/19

Another thing is the Fibre-To-The-Home (FTTH) roll out by leading 4G service providers and fabrication of telecom towers. FTTH is the installation and use of optical fiber from a central point directly to individual buildings such as residences, apartment buildings and businesses to provide unprecedented high-speed Internet access. FTTH services, has gained momentum due to its huge advantages in terms of offerings in all three services of voice, video and data.

Jio has begun offering fibre to the home (FTTH) broadband connections with 1.1 terabytes (TB) of free data at speeds of 100 megabits per second (mbps) in select markets in the country as the 4G entrant is expected to roll out commercial services in the second half of this year.

CLEAR Earnings Visibility

The company is one of the premium EPC contractor and OFC provider for the Digital India customers. As discussed earlier, there is huge demand for OFC in the country and this is expected to continue for atleast three to five years going ahead. With the current demand status, we are sure that the company is fully booked with orders and each subsequent new order are booked at higher margins. Thus, helping the company improve its profitability. This strong and clear visibility will offer a scope re-rating and there by improve the value of the stock and benefit its share holders.

Management Discussion & Analysis AR 2018

Phase 1 of Bharat Net over in Dec 2017 - Connected 100,000 gram panchayats with broadband

Phase 2 - Going on to connect 250,000 GP with broadband

For 5G OFC will expand 6x than current

VTL entered manufacturing of Solar PV cables catering to solar energy market supported by govt’s solar mission

Copper cable telecom network shrinking rapidly and getting replaced by OFC

EPC division undertakes complete solution for telecom cables networks, power cable networks, electric sub station installations etc

Business Review & Outlook

OFC network in india at 1.4M FKM from 0.7M FKM 2-3 yrs ago

Less than 25% of towers are fiberized and backbone network presents the biggest opportunity for OFC’s

5G requires 70-80% fiberisation from 20% due to low latency and other speed benefits

EPC biz - Telecon Vertical very well placed to execute substantial portion of Bharat Net Phase 2 orders which is to be executed on turnkey basis

Company has become the biggest IP-1 service provider. ( License issued by DOT )

| Vindhya Telelinks | |||||||

|---|---|---|---|---|---|---|---|

| 20th June 2019 | |||||||

| Mcap : 1576 cr | |||||||

| Promoter Holding : 43% | |||||||

| Investments of Vindhya Telelinks in Group Co’s | |||||||

| Mcap (Cr) | CMP | Share O/S | Shares held by Vindhya (Cr) | Stake (%) | Value of Stake (Cr) | ||

| Universal Cables (Power Cables) | 700 | 200 | 3.5 | 1.05 | 30.1% | 211 | |

| Birla Corporation (Cement) | 4,511 | 585 | 7.7 | 2.44 | 31.7% | 1,427 | |

| Birla Cable (Optic Fibre Cables) | 271 | 90 | 3.0 | 0.58 | 19.3% | 52 | |

| Total Value of Quoted Investments | 1,690 | ||||||

| Valuation Computation | Base | Bull | Blue Sky | ||||

| FY19 PE | 9.0x | 11.0x | 15.0x | ||||

| FY19 PAT | 168 | ||||||

| Value of core business | 1512 | 1848 | 2520 | ||||

| Hold Co Discount | 40% | ||||||

| Value of Stakes | 1,014 | (1690-40%) | |||||

| Case1 | Case2 | Case3 | |||||

| Overall Value | 2,526 | 2,862 | 3,534 | ||||

| Current Mcap | 1,576 | ||||||

| Upside | 60% | 82% | 124% | ||||

| Standalone | |||||||

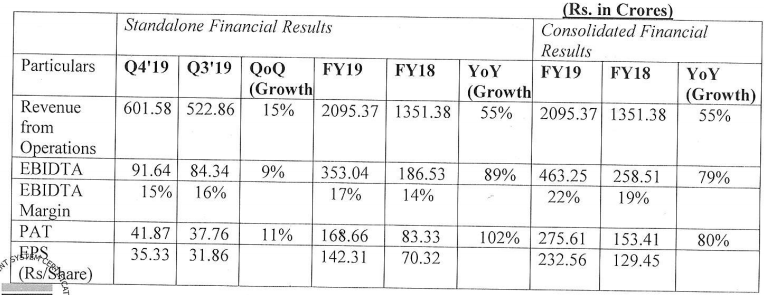

| Particulars | FY17 | FY18 | FY19 | CAGR Growth | |||

| Sales | 1044 | 1362 | 2108 | 26.39% | |||

| EBITDA | 147 | 188 | 353 | 33.91% | |||

| PAT | 65 | 83 | 168 | 37.24% | |||

| Consol (Incudes share of profit of Associates like Universal Cables + Birla Corporation) | |||||||

| Sales | 1061 | 1383 | 2132 | 25.71% | |||

| EBITDA | 163 | 208 | 376 | 19.19% | |||

| PAT | 117 | 266 | 311 | 38.52% |

3 Likes

Thanks and appreciated. If you could help to compare VTS with Sterlite Tech would be really useful.

1 Like

any view with recent 5G announcement

digital india Push

technical volume is rising

any expert opinion for fundamental and future prospect

1 Like

Any one following this stock???Why no dividend increase at all?

Just wanted to ask if anyone is tracking this stock and if there are any new developments with regards to this stock in the recent term. The stock seems to have corrected slightly just in the past month or two and I wanted to know how the other forum members think of this stock considering the push towards internet and fiber optics in India and abroad.

Quoted investments of vindhya telelinks in its Associates as on March 2022:

A) 19.33% stake in Birla cable => 19.33% of 374 crore(market cap of birla cables as on may 7th 2022) = 72.2 crore

B) 8.29% stake in Birla corporation => 8.29% of 7719 crore = 639.9 crore (after the recent 40% correction in this stock)

C) 23.85% stake in universal cables => 23.85% of 508 = 121 crore

- total quoted investments (A+B+C) = 833.2 crore

D) Aggregate Amount of Unquoted Investments = 402 crore ( as per annual report march 2021)

E) Investments in debt/ mutual funds = 45 crores

Total investments = (1+ D +E) => 1280 crores

market cap of vindhya telelinks as on may 7th 2022 = 1190 crores

In simple words vindhya telelinks business is available for free

4 Likes

3 of their 100% subsidiaries August Agents, Insilco Agents, Laneseda Agents owns 7.8% each, totaling 31.7% (8.3%+23.4%) stake in Birla corporation.

Investments in mutual fund is also much higher through these 3 subsidiaries.

Vindhya is such a deep value stock.

2 Likes

Been holding this business in our portfolio for the past year or so. (Around 4%, so not a lot). The thing is, that the market and its participants usually do not care what the assets owned by the business are but rather what kind of money the company is able to make on the ownership of those assets. Yes, Vindhya is really deep value by any measure. But also, the average ROE of the company for the past 5 years has been around 10% or so which just isn’t that great. Alongwith that, the infighting among the management/promoters ensures that market will just be unwilling to put a lot of money into the business. Having said all of the above, I am obviously optimistic about the company’s prospects in the medium term, so will continue to hold it as well as keep buying as and when I can find it for cheap (and have spare cash) as long as my thesis for investment holds true.

2 Likes

Operationally they are the best company in this space