During this quarter, NCLT sanctioned the scheme of amalgamation with Veeral Additives Private Limited. into Vinati Organics with effect from 1st April 2021

We expect Q4 numbers to slightly improve over Q3 or be in similar lines. I had mentioned the de-stocking effect in the overall sales as well as in ATBS, which I believe now is almost over. We are seeing sales of most products, including ATBS seeing pickup. Looking at this, I expect the demand to normalize in the coming months

The butyl phenol business has also scaled up well and delivered decent growth this year, and we expect the momentum to continue next year as well

We make four types of butyl phenols. The mono-butyl phenols are used in the fragrance industry as well as the resin industry. The di-butyl phenols will now be used mostly captively in Veeral Additives to make the antioxidants

The sales of IBB have also picked up starting the last quarter, and next year we are expecting to do higher numbers in IBB as compared to this financial year. Isobutylene as well as the highpurity MTBE continues to remain stable, along with our basket of customized products, the niche products, they all remain steady

We also commissioned the ortho-sec butyl phenol as well as the di-sec butyl phenol plant in this quarter. These products find application in agrochemicals, polystyrene, and perfumery. The DSBP is used in surfactants as well as in liquid dyes

We are the only manufacturer of OSBP and DSBP in India and expect about INR80 crores revenue at full capacity

The antioxidant business. In this financial year, the sales from antioxidants, we make five types of AOs. The phenolic ones are the 1010, 1076, as well as 135. The phosphite one is 168. We also make 10-98. They are used in different applications in polypropylene as well as plastics, lube additives, and the nylon industry. This year, the revenue from this business will be about INR100 crores to INR120 crores, which is at 25% capacity utilization

We are focused on optimizing our efficiency and ramping up sales in the coming months in antioxidants, and we expect this business to be a growth driver for our company as the demand normalizes. We expect to reach full capacity utilization in the next two to three years. We supply these AOs both in the domestic as well as the export market. We are also actively working on adding more antioxidants to our portfolio

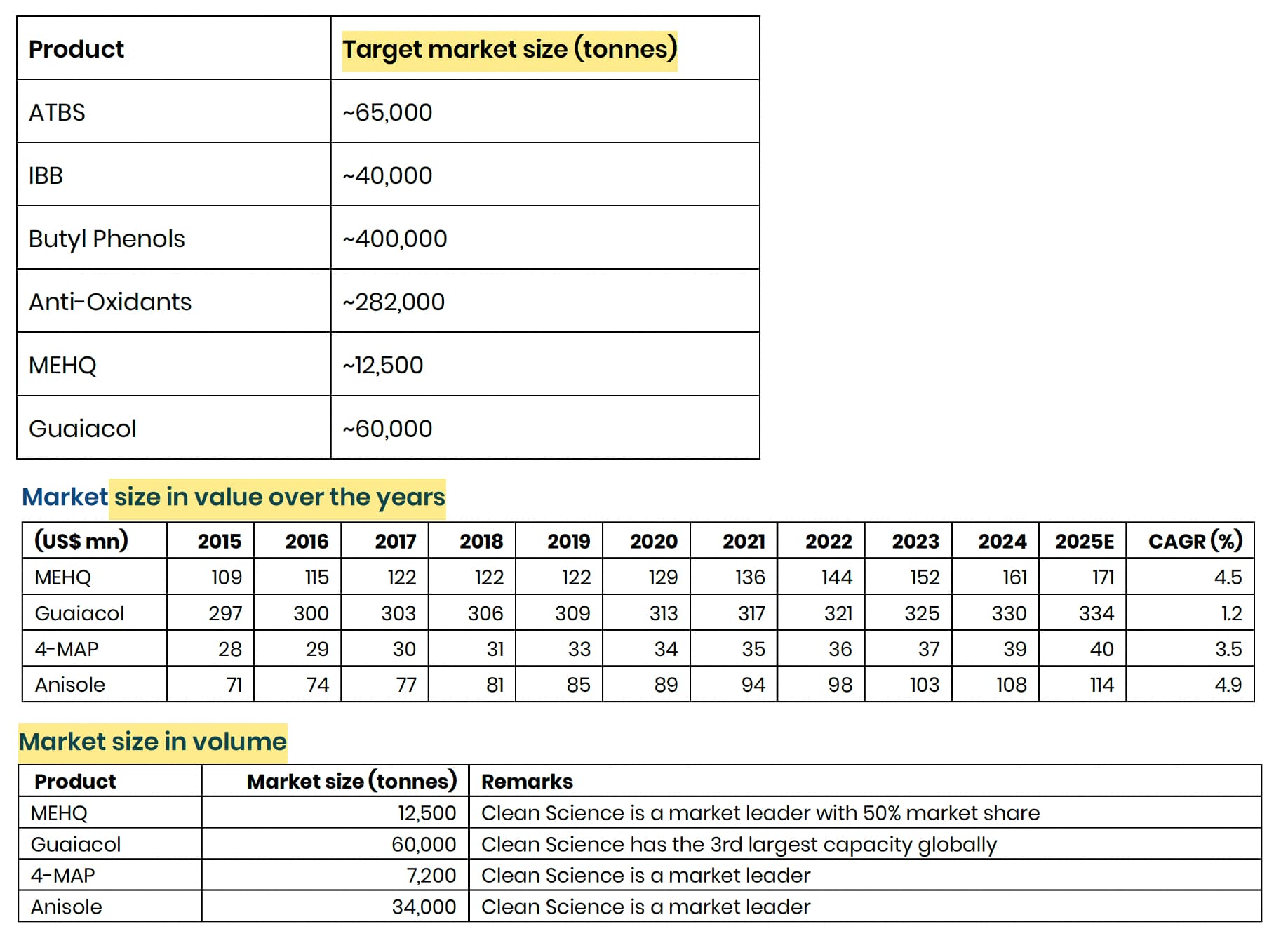

The long-term outlook remains positive. Now coming to VOPL, Veeral Organics Private Limited, which is a 100% owned subsidiary, a setup for manufacturing niche specialty chemicals. We have lined up a total capex of approximately INR 480 crores, mainly consisting of products, MEHQ, Guaiacol, 4-methoxyacetophenone, and isoamylene derivatives, as well as anisole. These products are used as polymerization inhibitors, pharmaceuticals, fragrances, and personal care. The MEHQ-Guaiacol plant is expected to be commissioned first by March 2024

Our long-term view on ATBS remains unchanged, and the ATBS expansion is expected to be completed by December 2024. With sustainability being a core part of our value proposition, we commissioned about 15 megawatts of solar power plant during fiscal year '23. Then we added another 11 megawatts this year in FY24, and we will be adding another 7 megawatts in the fourth quarter of FY25

We expect our revenue to have about 15% to 20% CAGR over the next three years, with growth coming mainly from antioxidants, the new products in DOPL, as well as growing demand in ATBS

Vinati reported better than expected results in Q4FY24 with highest ever quarterly EBITDA. While YoY performance is flattish, there has been significant improvement sequentially. The company seems to be back on track after 3 quarters of weak performance. After 3-4 quarters of subdued demand in ATBS due to destocking by the customers, ATBS has shown strong recovery. Though the company has been diversifying into new products, ATBS still remains largest profit contributor.

Even if one conservatively assumes, no further sequential improvement in the quarterly profit for next 4 quarters, FY25 PAT could increase by 29% (to Rs.104.5crx4 = Rs.418 crore). There are further triggers for revenue and profit growth for forthcoming years due to expansion of ATBS (by 50% of existing capacity) as well as for few other products getting completed during FY25 and ramp up/recovery in other molecules.

Management has guided for 20% revenue CAGR for next 3 years and indication of stable EBITDA margins. This looks achievable with possibility of positive surprises in my personal view. The stock return has been zero during last 3 years due to subdued earnings, delay in expansion projects and significant jump in stock price in earlier years. However, worst seems to be already over and there is visibility of earnings growth resumption. TTM PE is 53x, 5-year median PE is 48, 10-year median PE is 36. Stock may optically appear expensive on TTM earnings (which were depressed); BUT demonstrated track record, cost leadership and more importantly visibility of decent earnings growth, make me positive about the prospects.

Disc: Invested. I am not SEBI registered Advisor/Analyst. My view may be positively biased. I am not suggesting any investment action. The information provided above is for education purpose only.

During the quarter, the National Company Law Tribunal (NCLT) sanctioned the scheme of

amalgamation with Veeral Additives Private Limited (VAPL) into Vinati Organics with effect from 1st April 2021 and accordingly the comparative financial result and other financial information for the quarter, year till date, and year ending March 2023 has been restated taking into account the full effect of the merger.

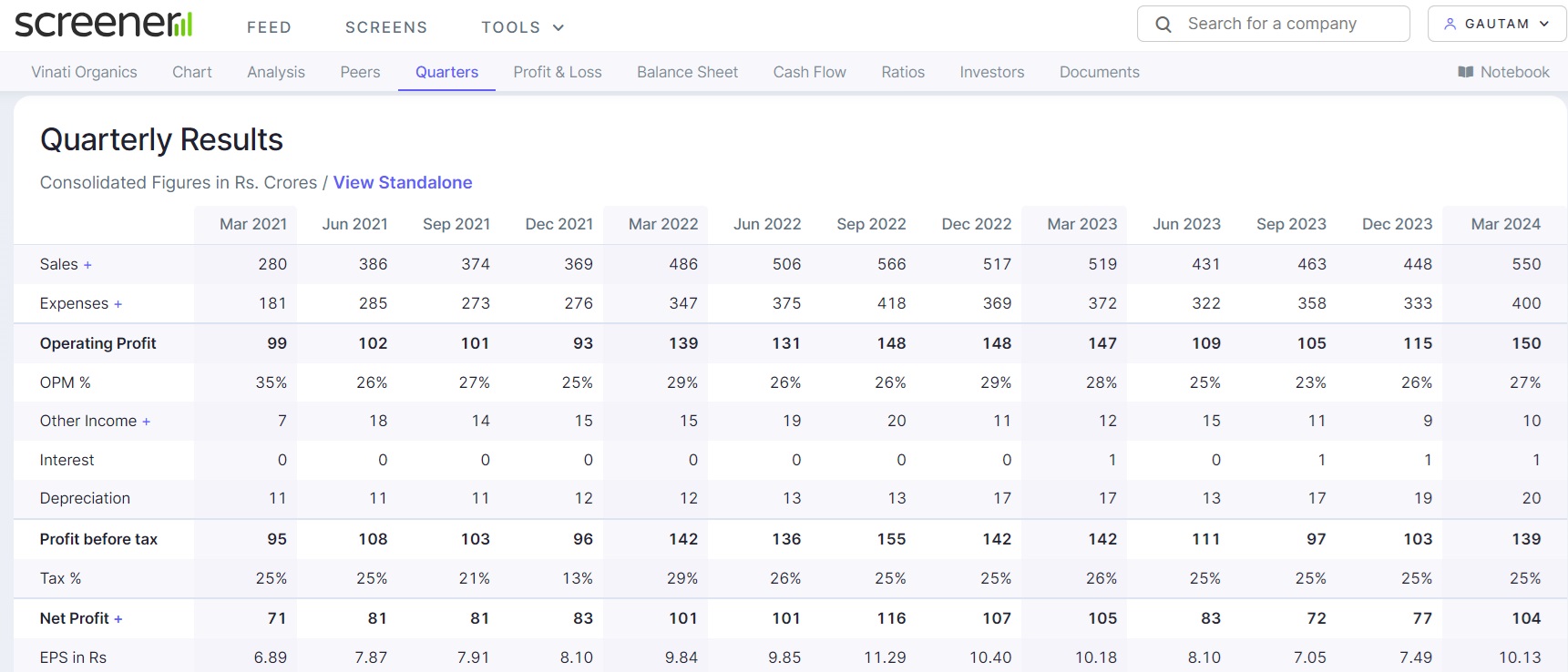

On a QoQ basis, the revenue from operations grew by 23% and net profit grew by 30% QoQ to ₹104 crore.

In FY24, the EBITDA declined by 18% YoY to ₹509 crore as compared to ₹620 crore in FY23.

BUSINESS HIGHLIGHTS

On a QoQ basis, the company witnessed volume recovery in ATBS (2-Acrylamido 2-Methylapropane Sulphonic Acid) and butyl phenols. The ATBS sales are now normalized and de-stocking is over.

In FY24, the revenue contribution from ATBS was ~32%. The sales were down compared to last

year.

The company’s global market share in ATBS remained unchanged at 60%-65%.

In FY24, the revenue from butyl phenols business was ~₹300 crore. The company witnessed good growth in this business and it was a major contributor to the revenue during the year.

During the year, the capacity utilization of butyl phenols was ~65%-70%.

The performance of Iso Butyl Benzene, Iso Butylen, and other customized products remained flattish YoY.

Over the last four years, the basket of customized products doubled in revenue to ~₹150 crore. The company expects good growth in the coming years as well.

In FY24, the revenue from the antioxidants (AO) business was ~₹130 crore. The demand for antioxidants is still going through a weak period. The company anticipates scaling up of antioxidants sales in FY25.

During the year, the capacity utilization of antioxidants was ~25%. The company expects to touch a 50% utilization level this year.

The research and development (R&D) department is also working on adding more antioxidants to its product portfolio and the long-term outlook of antioxidants remained positive.

In FY24, the company incurred capital expenditure of ~₹360 crore. Some part of the capital expenditure was incurred towards Vinati Organics for capacity expansion & addition of some new products and the balance was constituted for its subsidiary company Veeral Organics Private Limited (VOPL).

Veeral Organics Private Limited (VOPL) is a 100% owned subsidiary of Vinati Organics Limited for manufacturing niche specialty chemicals. The total capital expenditure in VOPL will be ~₹500 crores mainly consisting of anisole, MEHQ (Monomethyl ether of hydroquinone), Guaiacol, 4-Methoxyethyl phenol, and a couple of Iso Amylene derivatives. These products are used in polymerization inhibitors, flavors & fragrances, pharmaceuticals, and personal care. The asset turnover would be ~1x.

One plant of MEHQ (Monomethyl ether of hydroquinone) and Guaiacol was commissioned in March 2024. The company is still working on getting its product tested and sampled with customers. It is also working on enhancing the yield and efficiency of the plant.

The other products, i.e., anisole, 4-methoxyethyl phenol, and two more products to be commissioned in H2 FY25.

The ATBS capacity expansion from 40,000 to 60,000 metric tons per annum is proceeding well. It is expected to be completed in H2 FY25.

As of date, the company commissioned a total of ~33 megawatts of solar power plant. This will help in reducing the energy dependence on non-renewable sources.

FUTURE OUTLOOK

The company expects revenue growth of ~20% CAGR over the next 3 years mainly driven by the new products and some of its existing products.

The management anticipates an EBITDA margin of ~26% on a sustainable basis.

For FY25, the company plans to incur capital expenditure of ₹550 crore including the subsidiary.

The management anticipates the demand for ATBS to remain strong and expects double-digit sales growth in the next financial year.

In antioxidants business, the company expects sales of ~₹280-₹300 crore in FY25. Antioxidants business is expected to be a growth driver for the company. The peak revenue potential of the antioxidants business is ~₹700 crore.

In Veeral Organics Private Limited, the company expects sales of ~₹50 crore in FY25. It expects some sales from its recently commissioned MEHQ and Guaiacol plant.

The company is entering mehq and guiacol through anisole route. This has only been achieved by clean science so far who took share away from hq based producers. Does anyone have a sense on the economics vol can generate on these products? Clean science does north of 40 pc ebitda here.

Secondly with hq prices declining, have players using this route of manufacturing become competitive again? The price of hq had gone to 13-15 usd vs 10 usd price of mehq ans approx 5 for guaiacol. Hq prices are down to 7 usd now which makes such players viable again.

Stick To Guidance Of 20% Topline Growth & 26-27% EBITDA Margin In FY25

Disc: Invested. I am not SEBI registered Advisor/Analyst. My view may be positively biased. I am not suggesting any investment action. The information provided above is for education purpose only.

I am adding my notes from last few calls of theirs.

08.12.2023

Commercialized Ortho Secondary Butyl Phenol (OSBP) and Di-Secondary Butyl Phenol (DSBP) at Lote facility, only Indian manufacturer for both

OSBP capacity: 5000 MT; $4-5/kg product; used in agrochemicals, polystyrene, perfumery & liquid solvent dyes

DSBP capacity: 1000 MT; used in surfactants for agrochemicals, speciality liquid dyes

19.02.2024 CNBC

Witnessing order book recovery starting February across products, FY25 will be better than FY24 (15-20% growth in sales)

Anti-oxidant recovery is slower

Revenue from new line of ATBS will start in FY26 (expect 1.5-2x asset turns on brownfield capex)

27% is sustainable EBITDA margin

FY24Q4

Capacity utilization in ATBS (~611 cr.) and butyl phenols (~300 cr.) is near optimal levels

Antioxidants: 130 cr., 25% utilization; expects to double to 50% utilization in FY25 (280-300 cr.). Facing pricing pressure from Chinese oversupply and weak demand (peak revenue potential of 700 cr.)

FY24 Capex: 400 cr. (550 cr. in FY25); MEHQ plant (2000 MT) was commissioned in March 2024, and OSBP (5000 MT) and DSBP (1000 MT) in December 2023

Commissioned 33MW solar plant

CSM products contributed 150 cr.

12.06.2024 B&K

ATBS expansion (40k to 60k tons) will cost 300 cr. and is expected to commercialize in H2FY25

Antioxidants capacity of ~24,000 MT should generate 700 cr. sales

Started manufacturing butyl phenols in 2020 and incurred capex of 250-300 cr. for setting up a 39,000 MTPA capacity

MEHQ, Guaiacol, 4-MAP, anisole, and Iso-Amylene derivatives can generate 500 cr. sales with capex of 500 cr. capital expenditure (1x asset turns). Expected to contribute 50 cr. in FY25

ATBS competition: couple of Chinese companies have added ATBS capacities for domestic consumption (combined capacity is 15,000-20,000 MTPA). Atvantic Finechem (a Meghmani group company) has acquired trademarks and rights of Lubrizol’s ATBS technology and have started manufacturing ATBS in India. Their current utilisation is ~10-20 tons/month. Clean Science had also applied for an environmental clearance to manufacture ATBS

This quarter, I haven’t yet came to know about their concall. Any idea, whether they will conduct it or not?

Also in this post, you mentioned about 12.06.2024 B&K summary. I am not getting details of this in previous concall. Can you please help me with the reference or note of it.

There has been impressive scaleup from Atvantic Finechem in ATBS. The Infomerics rating report provides good insights into Atvantic’s operations. They purchased the patented ATBS technology from Lubrizol. Also, they has received product approvals from the leading customers, and their exports are expected to increase due to quality. In H1FY25, they already scaled to 72 cr. sales with 25.3% EBITDA margins!

FY25Q3

Witnessing Chinese competition from antioxidants and Butyl Phenol, antioxidant import prices are currently low. Working on higher value products in AOs

ATBS expansion (40k to 60k tons) to be commercialized in Q1FY26. Will reach full utilization in 3-years

Capex of 500 cr. in Veeral Organics to expand capacities for MEHQ, Guaiacol, and Iso Amylene derivatives, with meaningful contribution to start in H1FY26

Launched monomer inhibitor and a pharma intermediate from Veeral Organics

Incorporated US subsidiary to serve US customers and undertake reprocessing activity

Confident of 20% sales growth in FY26/27 with 26-27% EBITDA margin

Disclosure: Invested (no transactions in last-30 days)

Vinati Organics reported good numbers with growth coming back. Management continues guiding for 20% growth in next 2-years, sharing concall notes:

FY25Q4

ATBS: 30% growth in FY25 driven by volume (~790 cr.), maintained 60-65% global market share. Expect capex commissioning in June 2025 (capacity increase will be 25-30%) and guide double-digit volume growth in FY26, next phase will be commissioned in June 2026 (this is because they were planning to utilize 50% higher capacity in next 3-years). High molecular weights and high purity is used for oil recovery

Presently oversold in ATBS and have order backlogs, confident of utilizing new capacity coming on-line in June 2025. Major applications remain in water treatment and oil recovery

Butyl phenol: 26% growth in FY25 (~380 cr.)

AO: 70% revenue growth in FY25 (210 cr.+), expect continued growth momentum (plant running at 50% utilization which should increase to 90%+ in next 2-years). Developed product for lubricant additives which allows product expansion

AOs used in polypropylene, polyethylene and all their customers have expanded capacities in last 3-years

Butyl phenol + AO ~ 610 cr. in FY25, expect to reach 800-850 cr. in FY26 and reach 900-1000 cr. in next few years

IBB: (-27%) decline in FY25 (247 cr.) reflecting demand side challenges

Customized products: flattish

IB (Isobutylene), IB derivates & HPMTBE witnessed strong growth (337 cr.). IB is used in production of cypermethrin

VOPL: products will commercialize in Q2 / Q3 FY26 (new products: anisole, 4-MAP, TAA and PTAP; MEHQ is used in polymers, Guaiacol in pharmaceutical, TAA in agriculture and pharmaceutical, PTAP in resins industries). Expect 100 cr. revenues in FY26. MEHQ produced for captive consumption, teething trouble were resolved and MEHQ is now also being sold externally

MEHQ will be used to produce butylated hydroxyanisole (value-added product)

Consolidated – standalone will give VOPL numbers (4 cr. operational losses in FY25 excluding depreciation)

Total investment in VOPL is planned ~500 cr. in VOPL of which 250 cr. still needs to be done; full utilization asset turns will be >1; so ~500 cr. revenues)

400 cr. investment in growth capex in FY25, 360 cr. capex in FY26

Expect continued growth in ATBS, Butyl phenol and AO divisions. Expect 20% CAGR in next 3-years. In 3-5 years, EBITDA margin will be 26-27%

Solar capacity: 32.5 MW

Disclosure: Invested (no transactions in last-30 days)