Have they done Q4FY22 con call.

I am unable to find it.

- Company will be expanding ATBS capacity from 40000 MT to 60000 MT given the high demand.

- For this 300 crs capex which will be funded by internal accruals and is expected to get commissioned by December 2023.

3.The capital expenditure in Veeral Organics Private Limited is under progress. (280cr Capex)

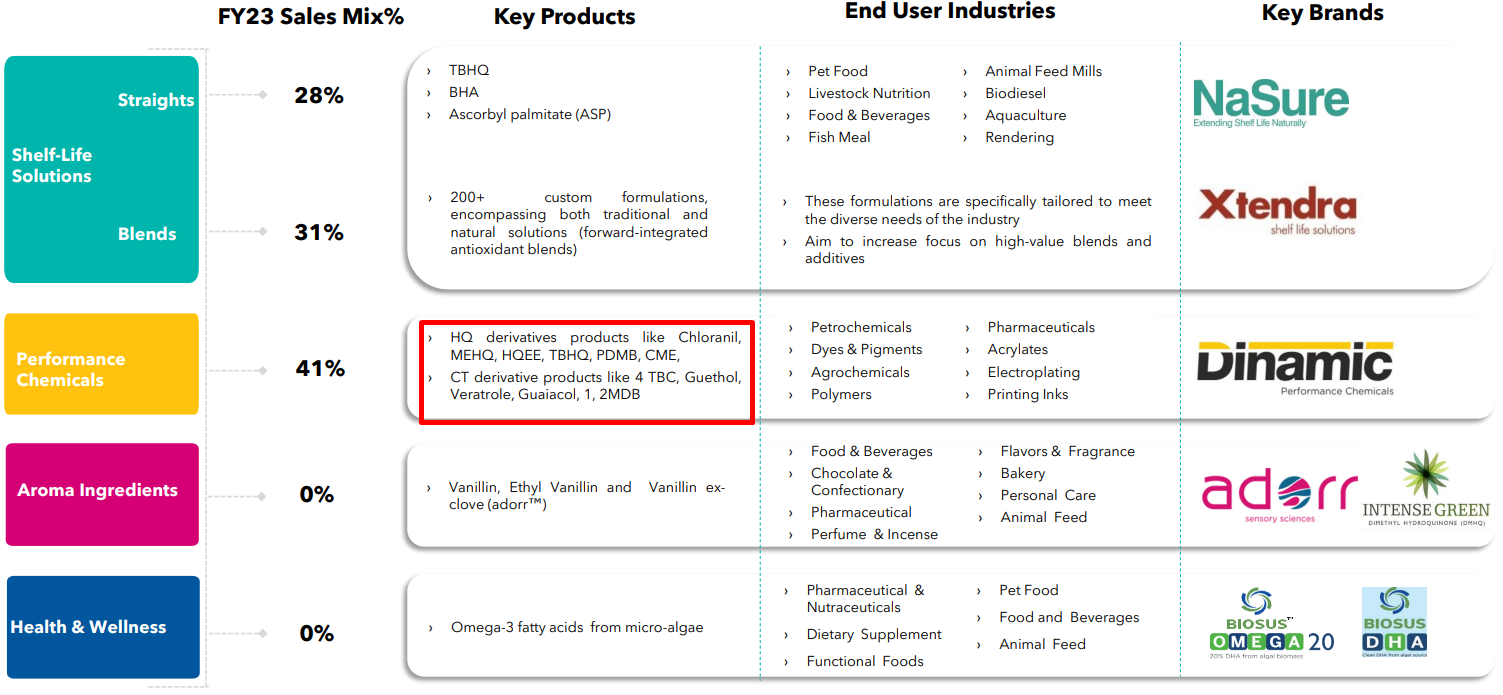

4.Products include 2000 MT of MEHQ & Guaiacol and 30000 MT of Iso Amylene.

Two of the above mentioned products i.e. MEHQ & Guaiacol also manufactured by Clean Science

2 Likes

2 Likes

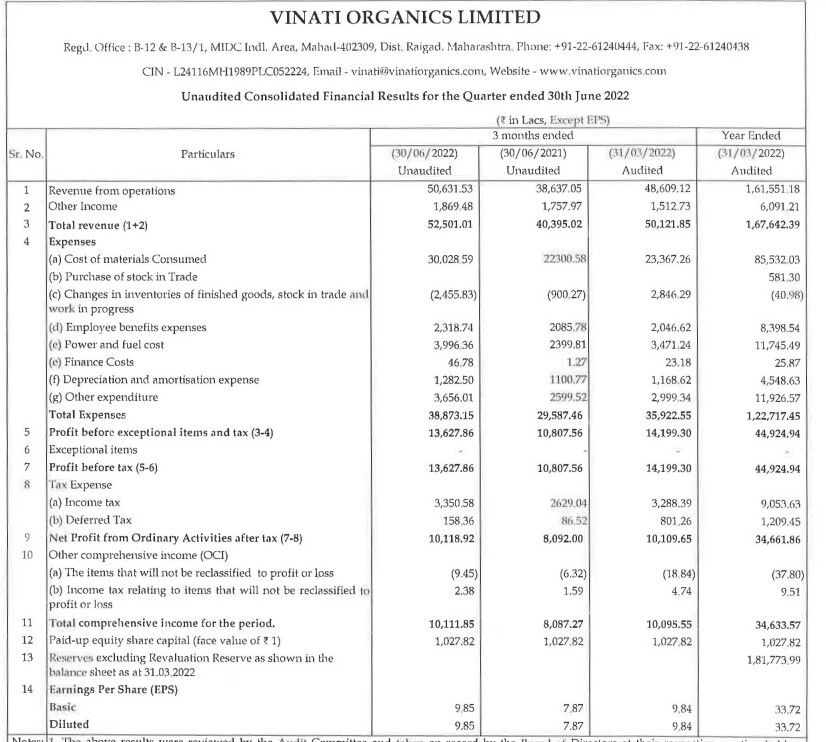

Q1FY23

- 31 % yoy growth in revenue.

- Blip in gross margin .

- EBITA margin declined qoq stable yoy.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/4037bcde-00f7-41b3-a4cf-071cca5b75e5.pdf

Still no update on Veeral Additive plant commissioning. Hope someone will point out in next interview.

Latest CNBC interview (link)

- Expect to maintain quarterly revenue of 500 cr. in FY23 with EBITDA margins of 28-29%

- ATBS expansion was triggered due to customer demand

- Veeral Additives: Will run at 25% utilization in FY23 and ramp up to 50-60% in FY24 (bring in 300-400 cr. of revenues)

Disclosure: Not invested (no transactions in last-30 days)

5 Likes

Did any one attended Vinati AGM? pls do share notes from AGM, if possible

Interesting. Promoters pledge 250,000 shares (a small quantity, admittedly) “to provide guarantee on loan facility availed by Alphagrep Securities Pvt Ltd". Alphagrep is a controversial Algo trading firm owned by Ms. Vinati Saraf Mutreja’s husband Mohit. Mohit’s business activities had never spilled over to impact Vinati Organics till now, so this is a first probably.

8C8211E0_E56F_49A2_AECA_CED986B6EA93_140653.pdf (bseindia.com)

17 Likes

Probably to cover leverage on non vinati holdings if it’s invested in USA, if so, we shld expect more

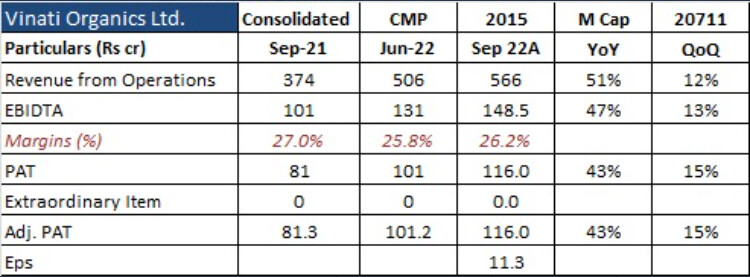

Interesting numbers by Vinati Organics this quarter. Raw Material cost reduced 46% qoq. Last quarter it jumped 35% qoq. Cash flow improved a lot.

2 Likes

FY24Q1 concall notes

-

ATBS (40% of sales; 170 cr.)

o Destocking from oil & gas customers as they had overstocked earlier (accounts for 30% of ATBS sales). Expect demand to normalize starting October 2023 as end demand has not been impacted

o 90% decline was due to volume and 10% due to price realizations

o Expansion from 40k to 60k tons will commercialize in March 2024. Expansion is based on confirmed orders from repeat customers

o Have not seen competition from any Indian manufacturer (Atvantic Finechem) -

Anti-oxidants and butyl phenols (Veeral additives; 17% of sales):

o Commercial ramp-up was slower, will do 150 cr. in FY24 and double in FY25

o Currently operating at 25% utilization

o Doubly backward integrated with butyl phenol and isobutylene

o Doing R&D into more niche AOs (higher realization, lower volume)

o Total revenue potential from butyl phenols and antioxidants will be 900-1000 cr. with 15-20% EBITDA margin (butyl phenol ~300 cr. + AOs ~600 cr.) - IBB (20% of sales; 86 cr.): Expected to remain steady in FY24. One Indian producer exited market this quarter

-

Veeral Organics:

o 260 cr. capex for MEHQ, Guaiacol, Iso Amylene derivatives and Anisoles. These products were used in polymerization inhibitors, flavors, fragrances, pharmaceuticals, and pesticides

o Total capacity for Anisole will be 5000 MTPA; for MEHQ and Guaiacol combined capacity will be 3000 MTPA

o Potential revenues of 350 cr.

o Plant will be commissioned by March 2024

o Production by phenol route: from methanol and phenol you make Anisole and from Anisole you make MEHQ and Guaiacol. This is the most cost-effective route currently

o Other routes to manufacture MEHQ are based on hydroquinone which is a more expensive raw material than Anisole -

Power costs

o Commissioned 15 MW solar power plant, which is currently catering to 55% of electrical consumption.

o Adding 11 MW solar plant, to be commissioned by September 2023 - Custom manufacturing revenues: 150-175 cr. in FY24

Disclosure: Not invested (no transactions in last-30 days)

10 Likes

4 Likes

In my experience, Management has consistently presented appealing long-term and short-term figures to investors, but they have rarely been able to attain these targets

Stock price has hardly moved in 2 years , either their MOAT is not working or their new products are not at same level as the existing ones.

I feel there is either lack of transparency or lack of operational excellence.

Many many disagree but I have come to this after holding the stock for few years and seeing it not moving in either direction

1 Like

Expected triggers over short to medium term

• Normalisation of ABTS demand

• Completion of capacity expansion for ABTS

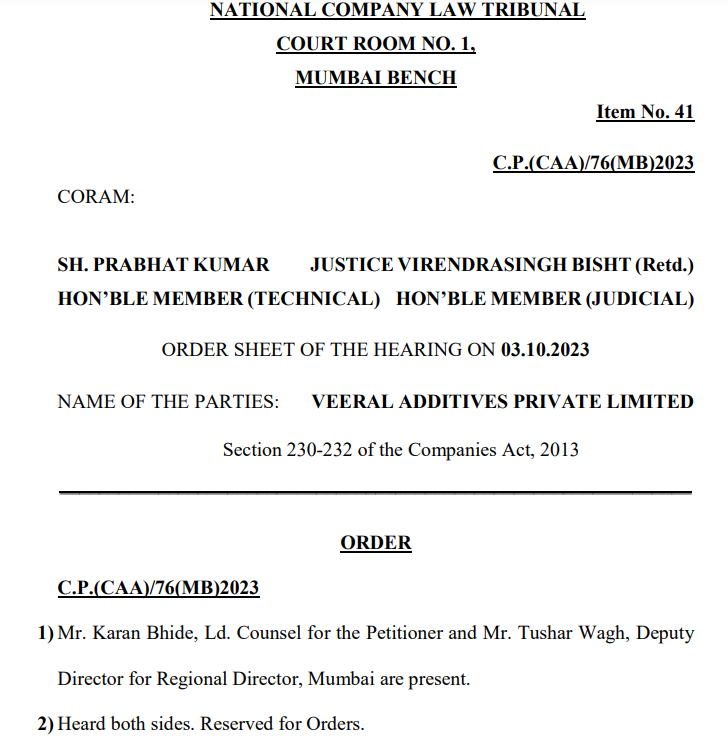

• NCLT approval for VAPL merger (currently owned by promoters)

• Ramp up in Anti-oxidants business under VAPL

• Operationalization of capacity under the subsidiary company VOPL (having MEHQ, guaiacol, isoamylene products)

• Revenue diversification due to above mentioned products

Key Risks

• While capex is already delayed, any further delay in capex could be negative

• Also, delay in normalisation of ABTS demand could be another over hang

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

1 Like

Vinati has commenced commercial production of new Ortho Secondary Butyl Phenol (OSBP) and Di-Secondary

Butyl Phenol (DSBP) at their Lote facility. Only manufacturer of OSBP and DSBP in India with an installed

capacity of 5000 MT and 1000 MT respectively.

15187dcd-61a2-4160-8c40-e104682a14e1.pdf (378.8 KB)

3 Likes

Few positive developments in this month

-

The company has commenced commercial production of Ortho Secondary Butyl Phenol (OSBP) and Di-Secondary Butyl Phenol (DSBP) w. e. f. 8th December, 2023. Vinati is the only manufacturer of OSBP and DSBP in India with an installed capacity of 5000 MT and 1000 MT respectively.

-

NCLT approval has been received for Amalgamation of Veeral Additives Private Limited with Vinati Organics Limited.

-

DGFT has imposed Anti dumping duty on import of Para tertiary butyl phenol (PTBP) from South Korea, Singapore, USA for a period of 5 years. Vinati is the only producer in the country with a capacity at 39000MT and it contributes ~17% of Vinati’s revenue.

While Vinati has a superb track record; stock has underperformed during last 2 years due to destocking of its key product ATBS by the customers and delay in completion of capex, which have impacted the earnings. Some positive developments have already happened during this month and more triggers (normalization of ATBS demand and commencement of new capacities/products) could be around the corner. If this happens, Vinati’s position can strengthen with a more diversified portfolio of specialty chemicals products apart from resumption of earnings growth.

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

12 Likes