@jacksparrow13 superb analysis. for me 4 months of receivables has been a put off and hence did not go deep into it but you chose to do that. Great efforts!

1 Like

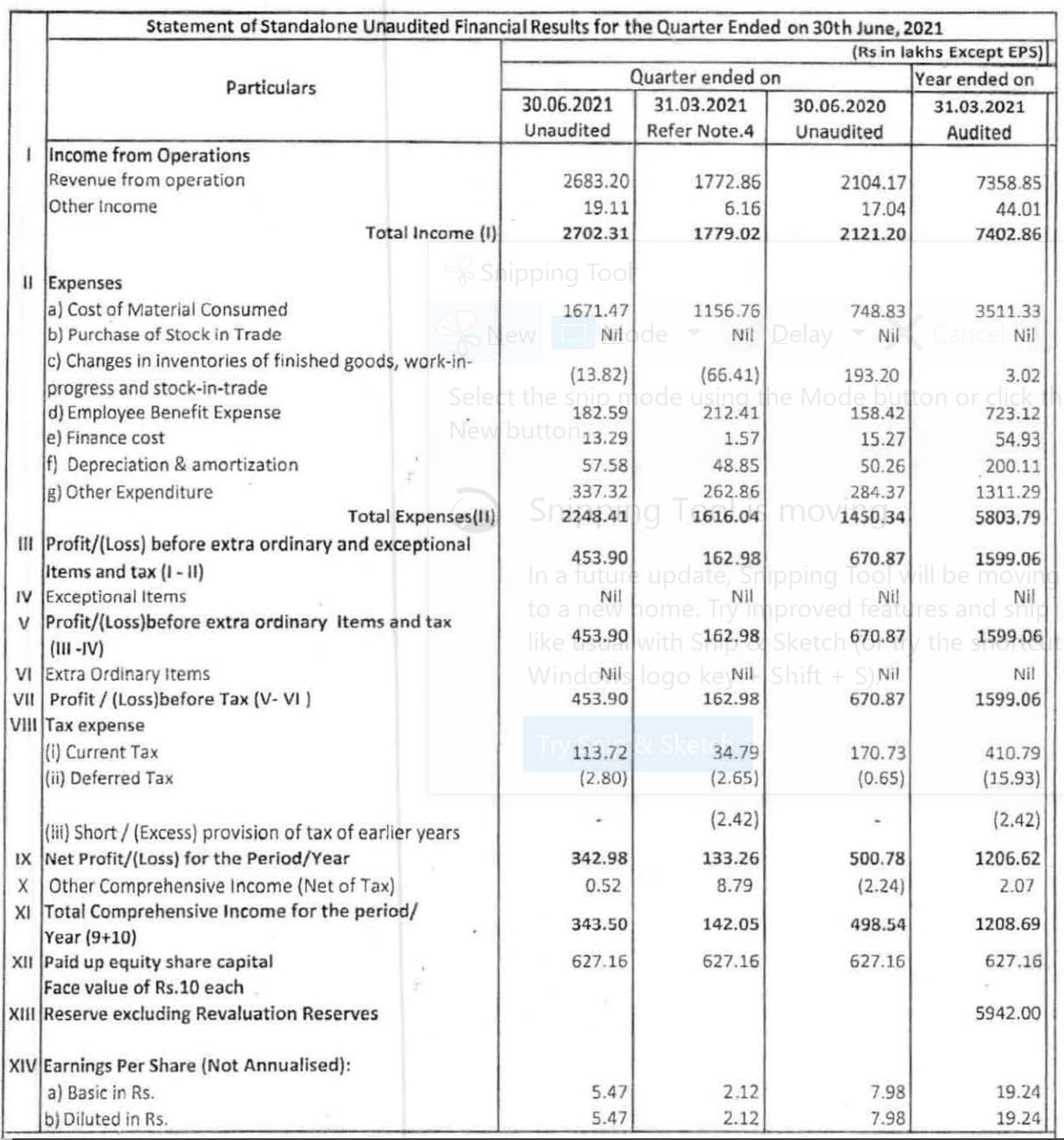

Q1FY22 showed good revenue growth but gross margins are lower. RM is more than double of last year.

Revenue came at 27cr vs 21.2cr yoy, and 17.8cr qoq. Looks very good. This is the highest revenue posted in one Q. Encouraging to see the scale up.

PBT at 4.5cr vs 6.7cr yoy and 1.63cr qoq.

3 Likes

Announced 4:1 bonus today.

2 Likes

Any views on demerger anounced recently

do you any competitors in India for them? And what is the market size of these excipients? I tried to get the clientele of the company but unable to fetch anything.

There market share, Excipients market size of India and Global, What is there clientele and is this business having any Moat? What is your view?

Do they supply to API players like Divis, lauras? What is the market share of Vikram?

Below is a comparison of revenues & margins of Vikram Thermo (VT) with another India based company in this space – Ideal Cures (IC).

Though Ideal Cures is not a listed company (majority stake acquired by a privately held company named Colorcon in 2021), this comparison might pose some interesting questions.

(Note: Ideal Cures financial data is taken from MCA filings)

Revenue comparison

| (in Cr.) | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

|---|---|---|---|---|---|---|---|---|

| Ideal Cures | 180 | 171 | 137 | 113 | 105 | 108 | 88 | 89 |

| Vikram Thermo | 93 | 74 | 56 | 58 | 50 | 50 | 39 | 38 |

In FY22 Ideal Cures was 2X of Vikram Thermo. In preceding 2 years though, VT has grown at a much higher rate (29% vs 15%).

OPM comparison

| Operating Margin % | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

|---|---|---|---|---|---|---|---|---|

| Ideal Cures | 24%* | 46% | 38% | 37% | 34% | 38% | 34% | 34% |

| Vikram Thermo | 17% | 25% | 22% | 16% | 11% | 17% | 21% | 16% |

*FY2022 OPM dropped due to a one-time bonus of 37 CR to employees.

Over the years, Ideal Cures’ margins have been significantly superior to that of Vikram Thermo. Among other, this is probably one of the reasons Colorcon paid more than 12x sales to acquire a ~70% in the company.

Almost all of this delta in margins can be attributed IC’s much lower COGS than VT.

7 Likes

So the question is - what could be the possible reasons for Ideal Cures’ so much higher Gross Margins?

Given the general lack of information on both these companies, it is hard to say for sure. But few of the possible hypotheses could be:

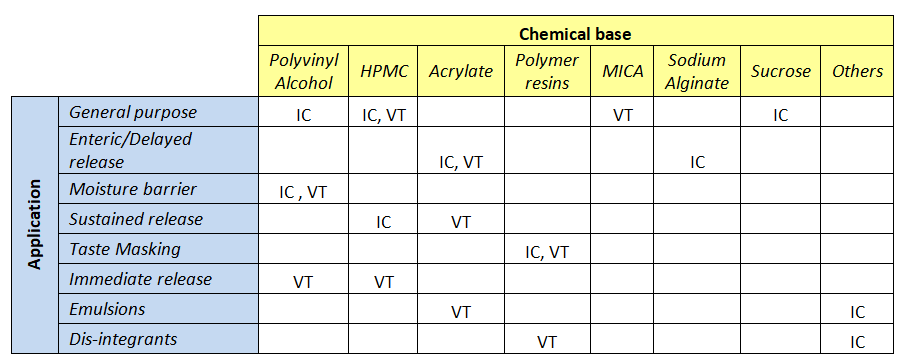

(i) Chemical base used in key products

Basis my understanding from the respective product brochures, have put together a table on chemical base and applications these two companies work on.

As can be seen from above, both have products across applications. However one difference is VT’s concentration on Acrylate polymer based products.

Basis product listings an estimate is that around 50% of VT’s listed products are based on Acrylate (as a % of all listed products). While the corresponding number for IC is around 20%.

This high dependence on Acrylate could be the reason why VT’s margins fluctuate widely based on crude oil (raw material source) prices while that of IC are relatively stable.

(ii) Ideal Cures is more R&D focused than Vikram Thermo (complex products, possible backward integration etc.)

Data on R&D spends is a bit patchy (inconsistently reported for IC). However for the years it is available, it does show that IC’s spend on R&D has been higher than that of VT.

While not conclusive, it could possibly indicate that IC’s products are better (in complexity and/or quality) and a somewhat higher degree of backward integration than VT.

| R&D spends as % of revenue | 2022 | 2021 | 2020 | 2019 | 2018 |

|---|---|---|---|---|---|

| Ideal Cures | NA | 2% | 2% | 3% | NA |

| Vikram Thermo | 0.1% | 0.1% | 0.2% | 0.9% | 0.1% |

(iii) VT’s sales mix (Pharma & Non-pharma split)

Till 2016, VT had about 30% of sales coming from DPO (perfumery stabilizer, HTF) which is relatively low margin vs their pharma products. They have stopped sharing the break-up of drug coatings vs DPO post 2016. However there are indications that DPO’s share in total revenues has been declining. Hence this in itself should not be a big reason for VT’s lower margins as compared to IC.

Above are just some of the hypotheses on why IC’s margins have been relatively better. If VP seniors can kindly share their views on possible reasons for above, it will really help newer equity market investors like myself ![]()

13 Likes

Hi,

I had worked on ideal cures several years back. From what i can recall - it seems ideal cure makes custom mixtures vs the standard power/liquid supplied by VT to everyone. No doubt ideal cure nos are fantastic. But given that VT also has DPO, i get a sense that the nos of VT are also very good. Most probably they are doing 25-30% OPM in good times and probably 15-22% OPM during other times. Personally by looking at ideal cures, I get a sense/excitement that maybe VT can also get on to this journey as they get bigger. 2-3 years back VT did start making these custom mixtures but i think they haven’t taken off in a big way.

Cheers,

Ayush

Disc: Invested in family and client acs

15 Likes

Thanks for sharing. Just curious to know where did you get such in-depth data?

Please do share the source.

Regards,

dr.vikas

@ayushmit: Hi Ayush ji, thanks a lot for sharing info and insights from your research on Ideal Cures. In case VT is able to emulate some of what IC has apparently been able to do in terms of margin expansion and consistency, it will be indeed quite an exciting prospect.

@vikasbargale - Hi Vikas ji, financial data above is taken from: (a) ARs of Vikram Thermo; (b) Public filings of Ideal Cures with MCA ( couldn’t find it at no cost, hence paid an online vendor to obtain those). If required, can share the files with you on your email ID etc.

Product data for these is based on info shared by them on their websites, their product brochures uploaded on CPHI sites etc.

7 Likes

and what are the clientele of VT? Could you share it if possible?

Hi Manish,

Publicly available info on this patchy. I am trying to get more info on VT through on-ground ways. Will post where once (and if) I get that.

4 Likes

@ayushmit sir - Looks like this will get in ESM list soon :(. What is the opinion of the other members on ESM?

1 Like

Exited. Stock will enter ESM Stage 1 anytime.

Had sent a few questions to the management on the business, and they were kind and cooperative enough to reply to some of those. The summary is as follows:

-

Recent quarterly reports of intl. players like Croda, Evonik, Archer Daniels etc. had mentioned sales slowdown due to de-stocking by their customers.

However, VT has not faced any such issues (till now). Demand from pharma (for polymers) and cosmetics (for DPO) is strong. Revenue mix as of last FY is 75% polymers, 25% DPO. -

Wrt margins vs Ideal Cures, as Ayush ji mentioned, IC is more into customised formulations (higher margin), while VT is more into polymers (can be thought of as a intermediary). Also IC has higher exports proportion due to its current ownership. Hence VT vs IC is not an apple to apple comparison wrt margin profile.

-

As per them, their know how and capabilities on a wide range of polymers (mostly acrylic based) is their advantage over other Indian players. The 3 primary applications of their polymer excipients are in: sustained release, enteric coating (targeted as per ph level of surroundings etc.) and taste making.

In my view, the India side of their polymer sales will likely follow - Indian pharma industry growth rate (expected to be around 9-10% CAGR till 2030 as per some industry reports) plus the addnl. market share they gain.

If they can keep on increasing exports and also add a few more product lines, they are likely to do really well.

The cyclicality of GMs is likely to be there based on crude oil prices (as long as their product mix is dominated by acrylic polymers).

PS - Still figuring out reliable sources to get key customer names.

9 Likes

Hi Ashish,

I have been trying to connect to the management, haven’t been able to yet.

Its difficult to analyse the company thoroughly with the amount of information available in the public domain.

It would be really helpful if you could share some insights or help me connect with the management.

Wanted to know about the following things

- The ability of the company to pass on the cost of materials (methacrylic acid, acrylic polymers); which will help us understand the fluctuation in margins.

- Major customers and their concentration

3.Revenue distribution (Product wise and Geography wise)

Thankyou so much.

2 Likes

Hi Shreya ji,

Yes, you’re right, it is quite difficult to analyse the company basis publicly available info as there is hardly any.

I was able to contact the mgmt. through the company secretary. I sent them some of the research I had done on few intl. and one major domestic player (Ideal cures) and asked them questions basis that. They replied to some of the questions on the mail, some they deemed as revealing confidential info and did not reply.

On points you raised -

On #2 and #3 were my part of my questions (apart from geography wise bit) - they were not ok to answer those. Only gave a general polymer & DPO revenue split.

On #1 - I have looked at their GMs from over last 12+ years and mapped them to crude prices. Basis that my inference was that ability to pass cogs is there, but I’d say limited. It was not one of the questions I asked since I was reasonably sure of my inference (caveat: you’d check this with them though as my inference might be wrong).

Wrt contacting the mgmt., maybe you can try contacting through the company secretary or maybe send questions for the AGM (which is in August). Also senior members on the forum might have better suggestions on this (ways to contact mgmt.) so maybe you can check with them too.

4 Likes

Thankyou so much for your response, I had a talk with the management today.

According to them, the fluctuations in the margins is primarily because of DPO (commodity business with low margins). After the demerger is done, stability in margins can be expected.

Also they usually absorb the raw material cost fluctuations in the short run.

Hope this information is helpful, pls add on if there’s anything else that you come to know of, regarding the company, in future!

7 Likes