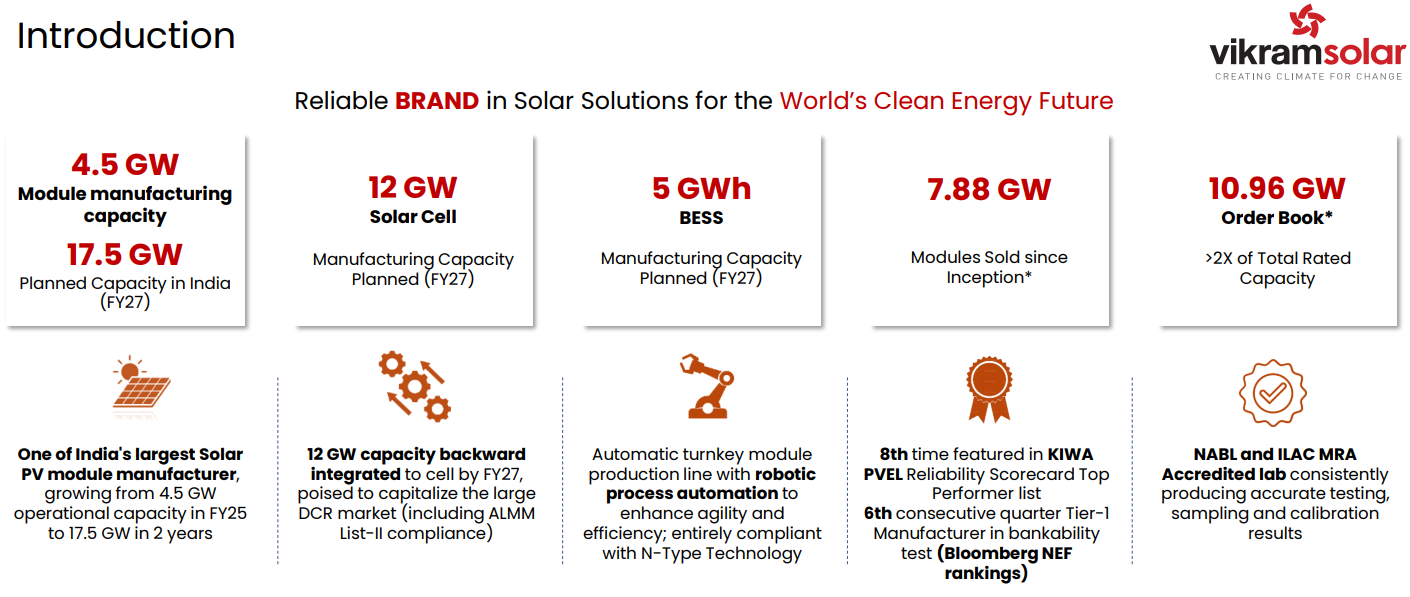

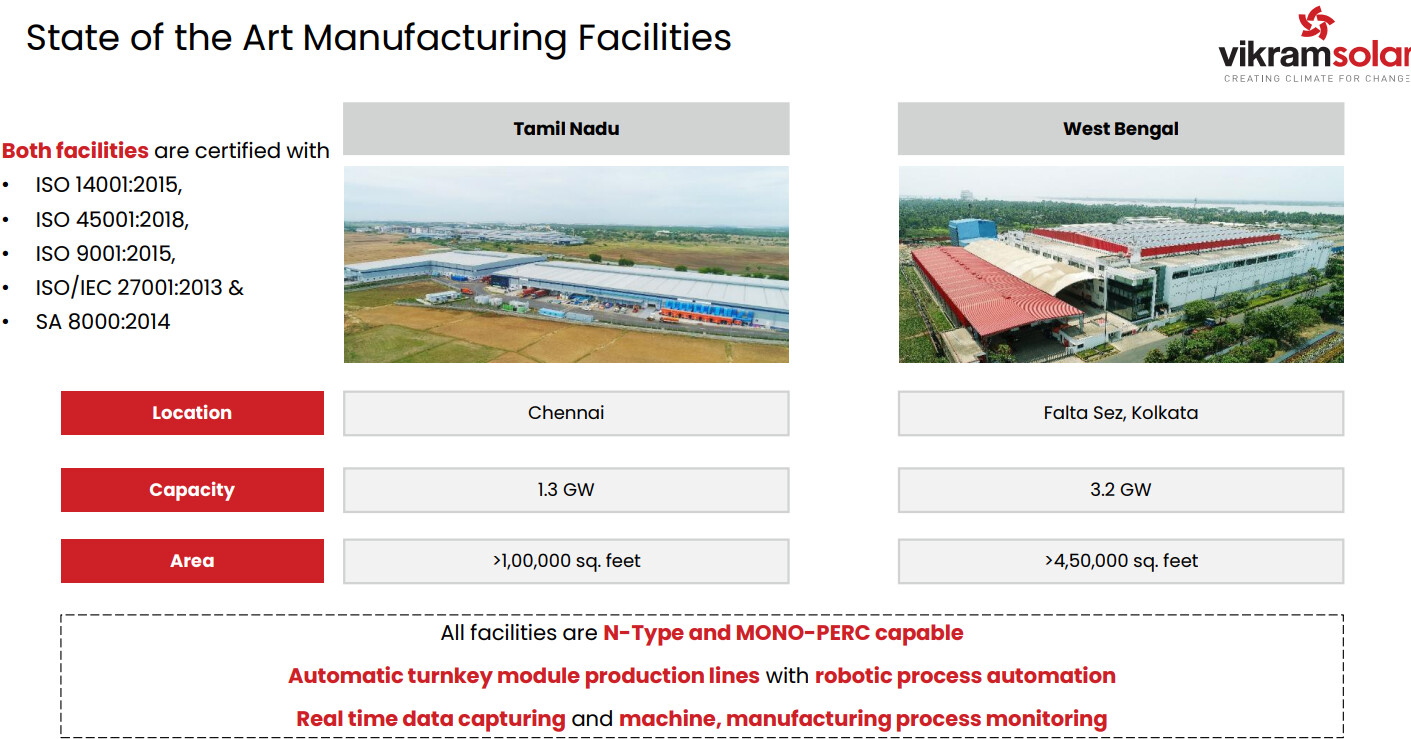

Vikram Solar is the one of the oldest PV Solar module manufacturer with an capacity of 4.5 GW PV module as on 30.06.2025, out of which 1.3 GW was added in the Q4FY25.

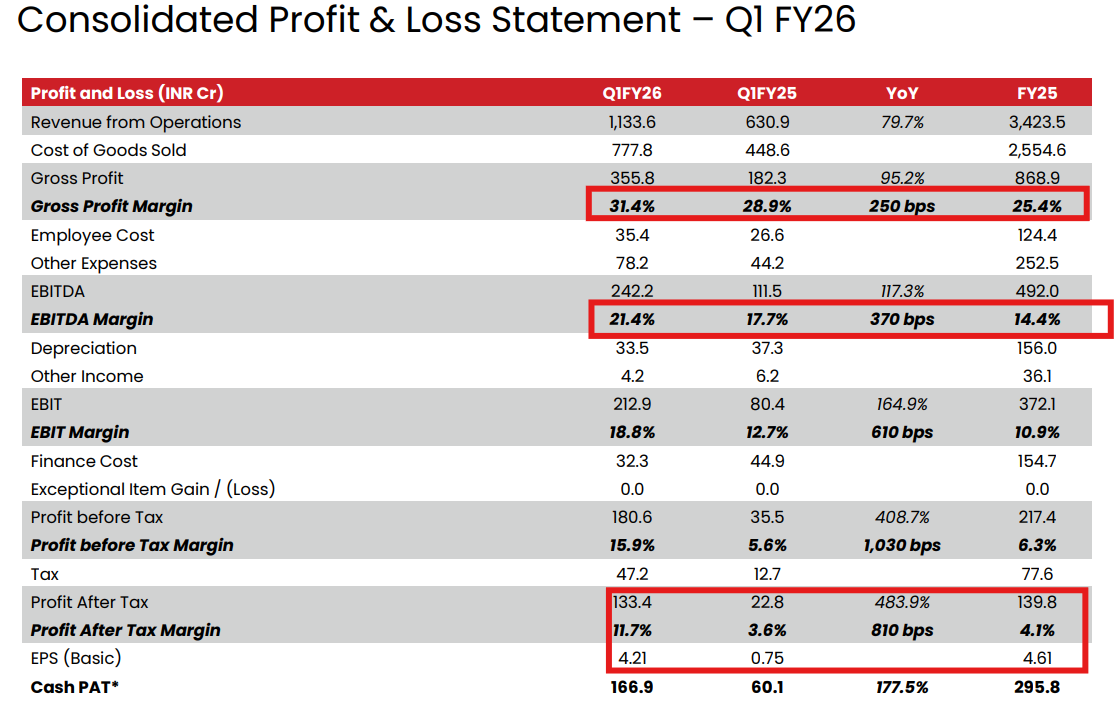

This capacity addition and increase in utilization of the previous capacity, drop in polysilicon prices helped the company to post stealer PAT in Q1FY26, Which is entire ~FY25 PAT. These Gross margins may not be sustainable as there is some trend reversal in polysilicon prices, but mix of fixed and variable price contracts may help to maintain the EBITDA margins around 20%

They have an ambitious order book of ~11 GW, which is ~2.5x of existing capacity. Complete order book is of Non-DCR as they don’t have any captive cell facility.

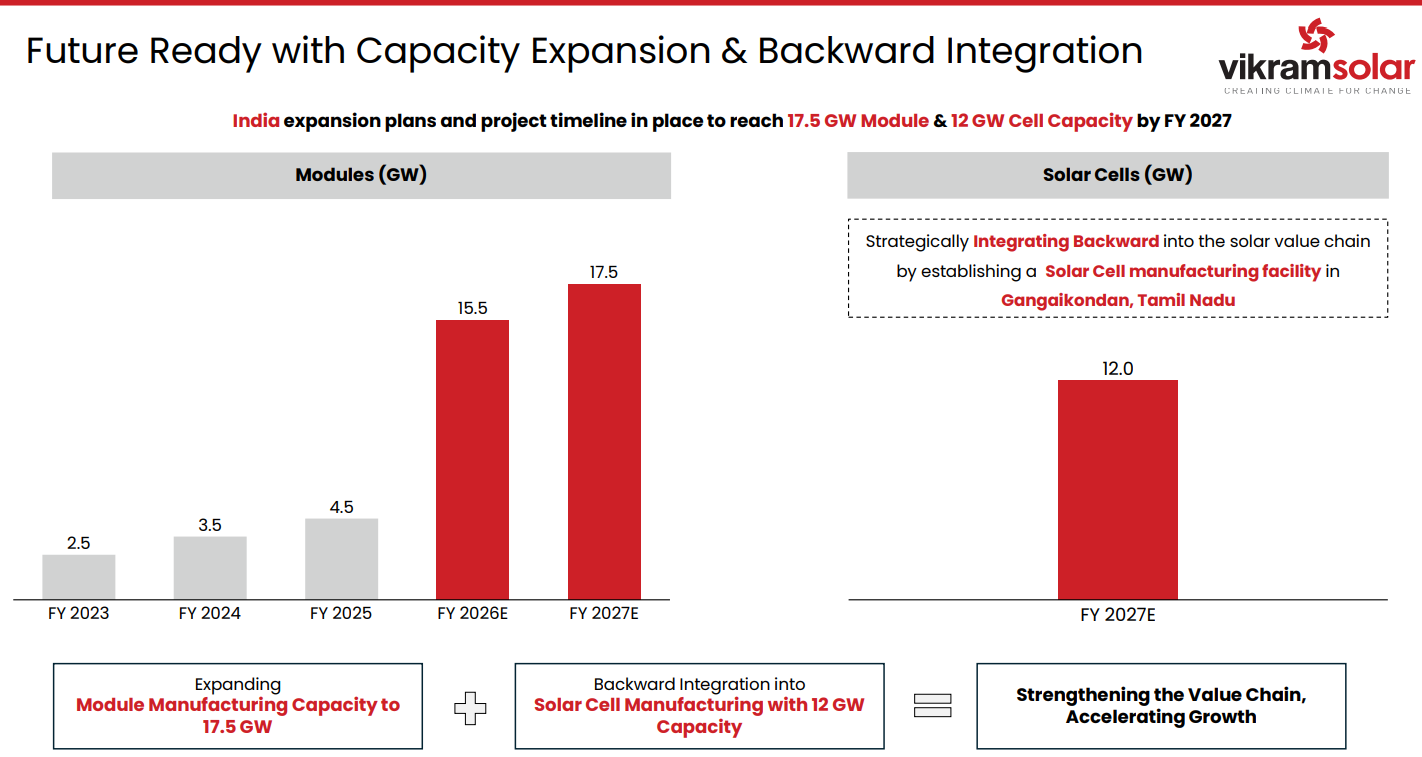

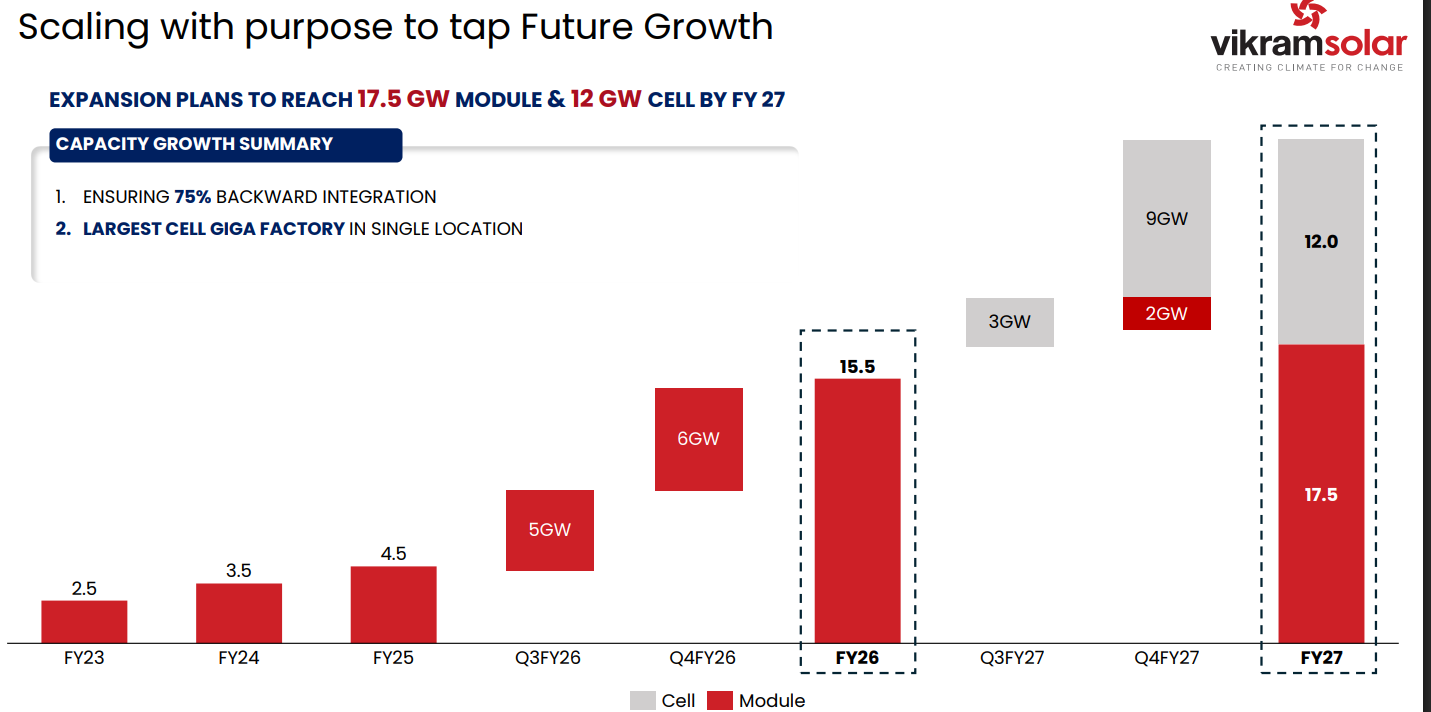

**Module:**They have very ambitious capex plans for the next 2 years, they want to scale the Module capacity from existing 4.5 GW to 15.5 GW by FY26 end and further to 17 GW by FY27 end in india.

They are going to add 5GW capacity in Q3FY26 & 6GW module capacity by Q4FY26.

Cell:

Proposed 12 GW cell capacity is going to come on stream in FY27, which can open gates for DCR market, which is high margin lucrative segment as compared to existing order book of Non-DCR.

BESS They have plan to add 5 GWh by FY27 end.

Existing manufacturing facilities.

Strengths:

They have very well experienced in the solar module manufacturing being an early entry in the industry.

Heavy capex plans in the coming 1.5 years could shape the Numbers 4-5 folds.

After cell facility coming on stream they can tap the DCR module segment also, which can boost the margins ~30% like premier energies.

There is lot of growth potential in the coming 2-3 years for this company Negatives:

Being a commodity oriented company, price fluctuation in the prices of modules and cells can flip the business.

Manufactures need to upgrade/adopt the new technologies in the module manufacturing for every 3-4 years, which involved shutting down existing line and upgrading them for better efficient module manufacturing.

Lot of competitive intensity from the China is a big threat the industry.

Govt is protecting the local manufactures with some DCR, ALMM lists, any changes in the policy of such protective measures can hit the industry very badly.

Now there are lot of capacities are under construction in module and cell segment All these capacities are going to capitalize by FY27-FY28 and expectation of over supplies can not be ruled out, which can drop the prices from the current levels. In that case current margin profiles will vanish till demand pickup.

Disclosure: Invested recently and opinion might be biased.

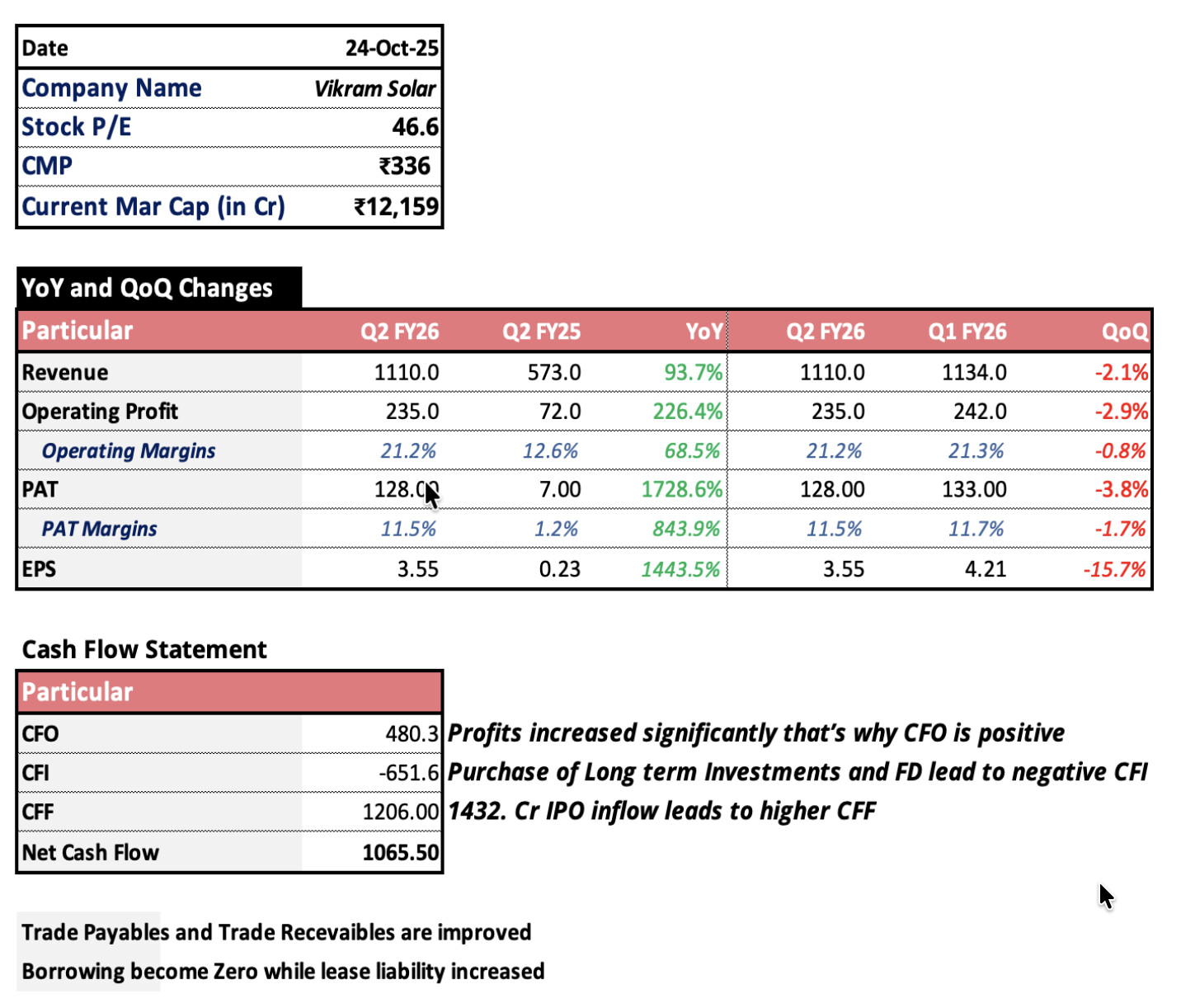

Good set of numbers from Vikram Solar, margins are still intact.

Need to check whether these margins can be sustainable for coming quarters or not due to jump in RM prices?

if things go well, they may end up at 500 Cr PAT (Excluding the numbers from new capacity additions in Q3 & Q4) for FY26~ 20 PE of FY26 numbers.

Capex timelines are clearly mentioned in the presentation

Result was above the expectation and even new modules capacity soon to begin.

From 4.5 gw to 14.5gw they will touch in 4-5 months)

Huge opportunity for player like vikram.

Trading near to 20 TTM P/E

Its same with even all other major players like premier and waaree all are having capex boom and huge capacities is going to go live in 1-2 years.

All are Trading at Lower PE multiples even there is some capex visibility in coming 1- 2 years.

RM prices and Technology upgradations are very powerful factors of module manufacturer’s, these 2 things can hit the margins badly. Period of 2023 & 2024 are the best examples for this, Players who are posting >1000 Cr PAT posted losses in those years due to sharp fall in prices and technology upgradations.

I feel these are stopping the market to give higher PE multiples even there is some visibility of capex & order book execution in coming 1-2 years.

Vikram: In todays call management confirmed that they can maintain the current margins in coming quarters with a mix of Variable & Constant pricing orders in the order book.

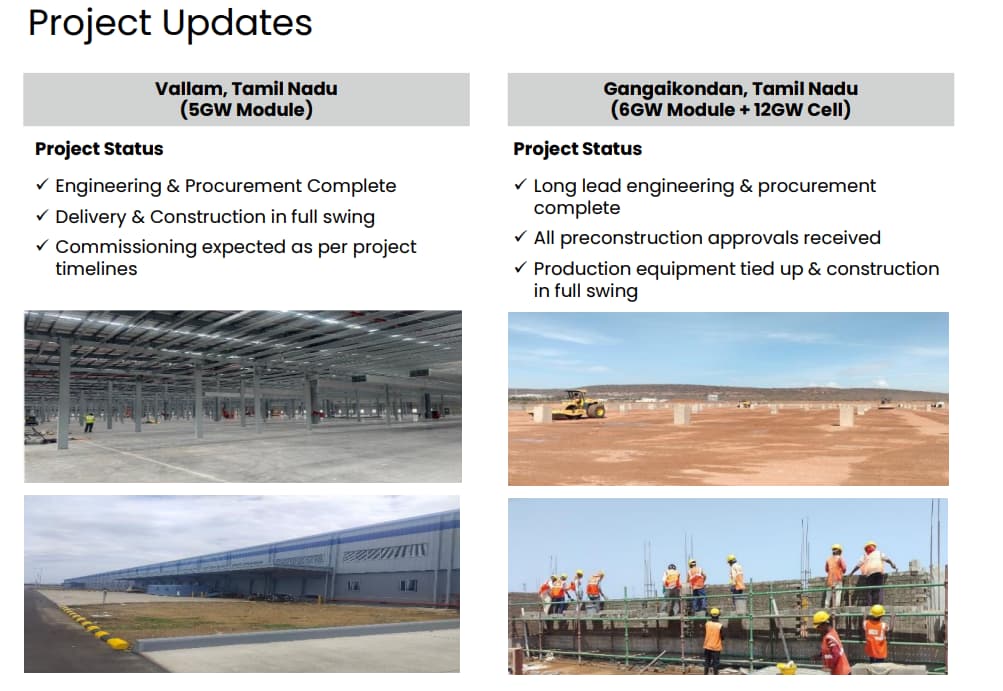

Out of 5GW coming on stream in Q3, 2.5 GW will be commissioned in Nov & remaining 2.5 GW would be commissioned in Dec.

We may see good numbers most probably double’s in Q4 after this 5GW capacity will be on stream completely.

Company has sold 784 MW of modules this quarter, 189% year-on-year increase from 271 MW. The effective capacity utilisation for the quarter was 84%.

Name plate capacity utilisation stood at 65% plus which is inline with the industry.

By end of FY26 company will have 15.5 GW of capacity of modules.

And by the end of FY27 company will have 17.5 GW of modules and 12 GW of Cells manufacturing Capacity.

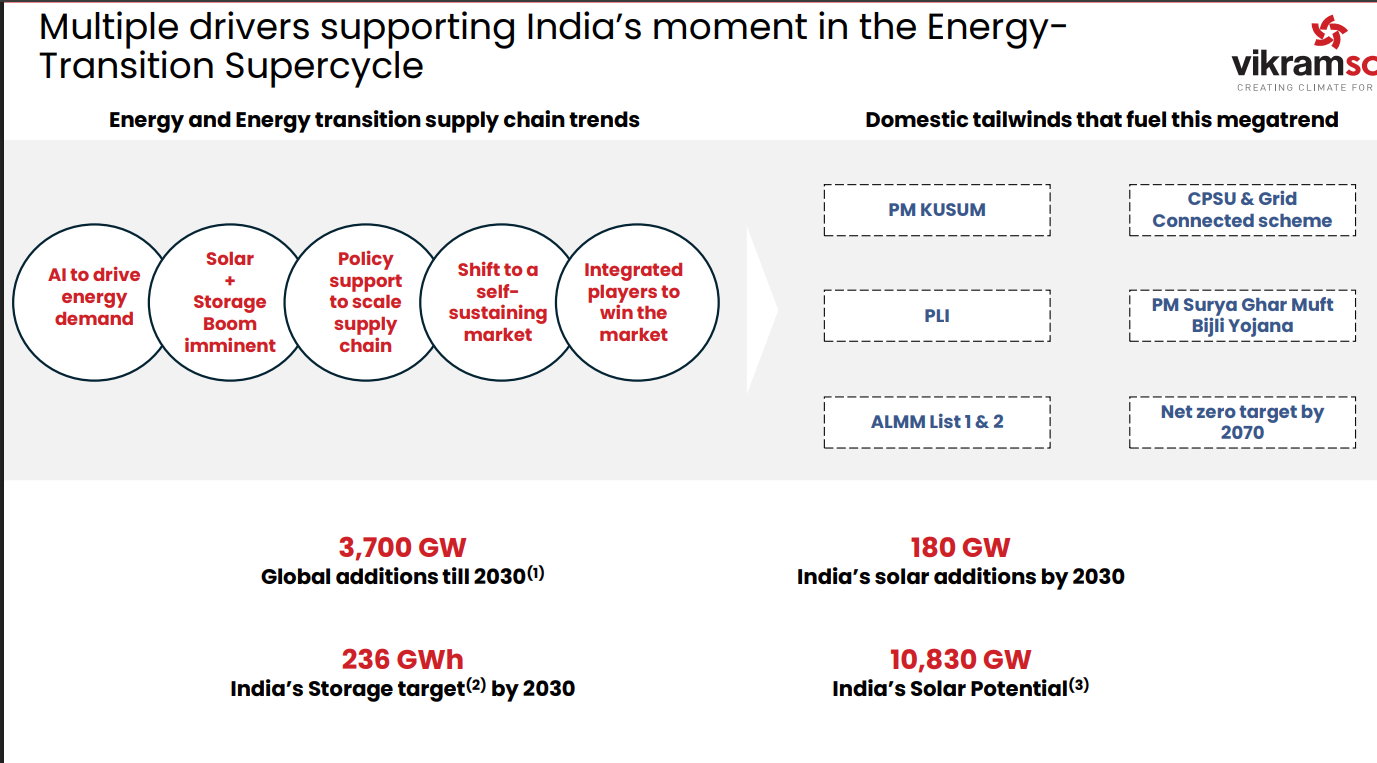

GST rate cut improves affordability and helps in accelerate adoption.

Company is net debt free now.

Order Book: The order book stood at 11.15 GW as of September 30, 2025, 36% growth from 8.21 GW in the same period last year. The composition of the order book is 85% domestic and 15% export orders. The robust order pipeline of approximately 38 GW.

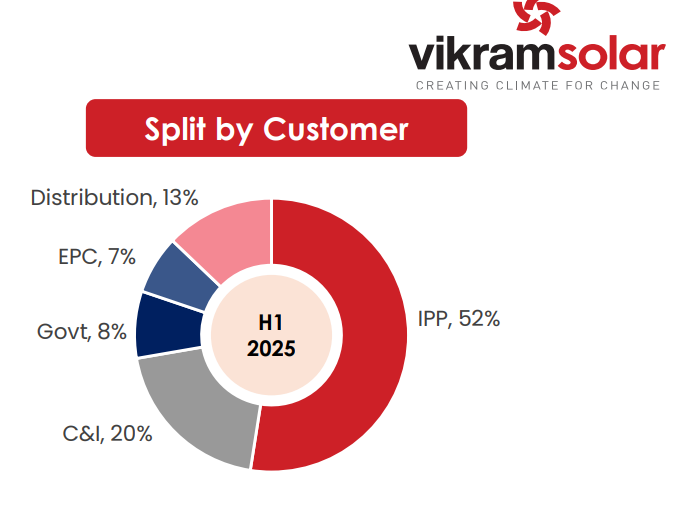

The company has shifted its customer mix to reduce concentration and tap into high-growth areas.

The current split is IPP (Independent Power Producers) at 52% (down from 72% last year), C&l; (Commercial & Industrial) at 20% (a significant surge from 4% last year).

Capex and Expansion Plans: The company has a total Capex plan of approximately 6,200 crores for its expansion projects.

For FY26, the company plans to spend a total of 800 crores, having already spent 200 crores in the first half.

The funding for the total Capex will be a mix of debt (approx. 3,500 crores), equity (approx. 1,500 crores from IPO proceeds), and internal accruals (approx. 900-1,200 crores).

The debt-to-equity ratio is expected to remain below 1 even after the completion of all projects by March 2027.

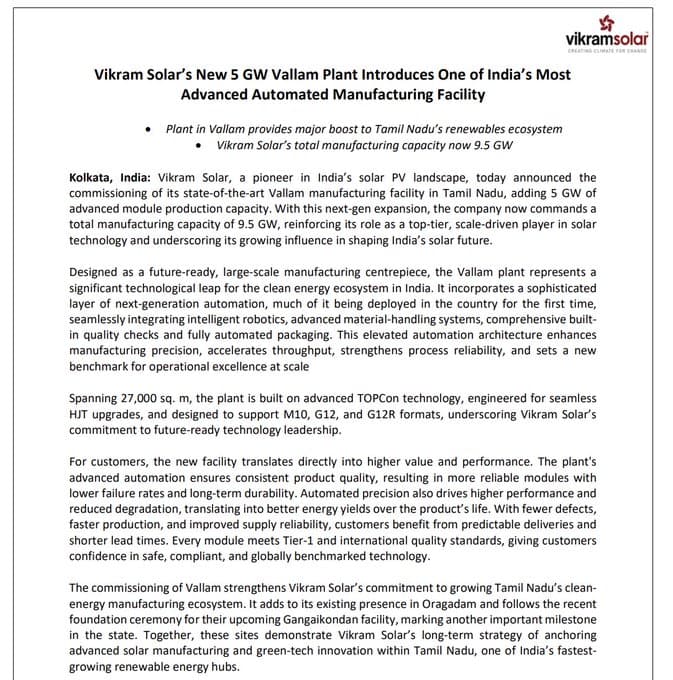

Vallam Project: 5GW project will be completed by Next Quarter which will increase total module capacity to 9.5 GW.

Gangaikondan Project (Greenfield): 6 GW project will be completed by Q4 FY26 which increases total capacity of module to 15.5 GW by year end.

The DTR has recommended an anti-dumping duty of 23-30% on solar cells imported from China. Management clarified that this is currently a recommendation and not yet levied.

Despite reciprocal tariffs making exports from India cost-prohibitive, 15% of the order book is from the US. The company is actively exploring alternative supply chains for cells from countries with lower tariff levies than India.

Management is confident in maintaining the current EBITDA margin level of around 21%.

By the end of FY27, with a total module capacity of 15.5 GW, the company anticipates being able to deliver approximately 10.5 GW of modules annually, assuming a 65% utilization rate on the nameplate capacity.

the margins for waree energies and permier look way better than vikram. if the capex is happening industry wide why roe and roce is lower compared to peers?

am i missing something?

[quote=“Arji[quote=“Arjita_Rajput, post:9, topic:209224, full:true”]

the margins for waree energies and permier look way better than vikram. if the capex is happening industry wide why roe and roce is lower compared to peers?

am i missing something?

[/quote]

ta_Rajput, post:9, topic:209224, full:true”]

the margins for waree energies and permier look way better than vikram. if the capex is happening industry wide why roe and roce is lower compared to peers?

am i missing something?

[/quote]

Blockquote

Premier is into DCR modules, obviously margins will be higher. Waree has some backward integration.

This is the catch here, Vikrams margins are low due to multi locations facilities and pure module play. margins will also catch up with waree after completion of 11GW installation in Q4.

Q4 onwards numbers will jump due to 5GW capacity addition in Q3, Q1FY27 numbers would be much better due to addition of 6GW more capacity.

Margins may catch up from Q2 onwards.

got it, also there current order book stand at 11.5 gw so that means approx 16,000 cr of projected revenue basis order book ( i have calaclated this basis h1fy26 total revenue and volume sold in the h1)

Premier is not listed in ALMM-II. Only n-type ToCpon listed in ALMM-II so far is EmmVee and Adani.

Waaree and Premier margins are higher primarily due to backward integration. Vikram will see a significant jump in its overall margin in next 6-7 months

ALMM 2 mandated use of solar cells for any projects bid after 1st Sep 25

Vikram has 11.2GW orders as of 30th Sep 25 (all exempt from ALMM-2 as i understand)

These should be enough to get them through till Mar’27 (given they will have 15 GW capacity at 80% usage)

Post Mar’27 they should have 12 GW of cell manufacturing which should be able to get them in as an ALMM2 certified player right ?

My Question is :

Will they be able to bid for new ALMM 2 projects now since they expect to have cell manufacturing by Mar’27 or they cant bid until they have an ALMM certification ?

Will there be any delay for ALMM 2 certification post making the plant ? If so there will be a gap,…

Yes, their orderbook is exclusive of any ALMM cell requirements.

Their Phase 1 of cell capacity 3GW will be on stream in Q3FY27, where as ALMM-2 will start from Q2FY27. There is a gap of 6 months and in Q4 they will add balance 9 GW. I think they will take orders from now onwards for ALMM-2 modules. I think other players also has enough ALMM-2 Order book ahead of capacity commissioning.

All these new capacities require huge capex, they should generate good cash to minimize the dependency on debt & equity.

In the current scenario of rising silver prices will Vikram be able to defend its margins by passing on increased prices? Or the margins will take a hit?

Almost 50% of order book is linked to cell price, so they can pass on 50%. As Module prices have corrected they may gain something from the fixed price orders aswell.

DCR is Zero for Vikram Solar.

In the current senario, due to slow down in tendering visibility for DCR is very low. Margins may stabilize ~18% as hinted by management. There may be some slight dip in margins in the next 2-3 quarters due to module price correction, but ,margins would be back to normal level when cell capacity will be online.

In my opinion vikram is well poised in the listed players as they don’t have any DCR orders in the order book and It is also well diversified. Risk of margins erosion would be better to some extent as compared to Premier/Waaree.

Gone through a report, concerns are only pertaining to heavy debt going forward. Even though EBITDA will jump 100% in the next 2Y, PAT will be muted due to high interest cost & depreciation.

Here the assumption is Gross debt would be 7700 Cr by FY27 end, but management told that Total capex is 6200 CR ( IPO-1500 Cr+ 1200 Cr internal accruals and 3500 Cr would be debt). if they the debt levels are maintained as per management commitment then we can see growth in PAT in contradiction to the what stated in the report.

I feel this is the one reason dragging the price.

Similar poor PAT growth of Waaree also from FY26-FY28 is being reported in the same report, whereas this growth is better for Premier energies for the same period.

I got bit confused on recent promoter pledge of 1.5cr shares immediately another announcement of revoke pledge. There is small confusion, the promoter pledge of 4.17 percent. Earlier, this pledge was allocated to Vistra ITCL in September 2025, and later the same percentage was revoked and transferred to Aditya Birla Group. This isn’t a new pledge, it’s just a transfer of already pledged shares.

Current Promoter Pledge:

The current promoters still hold around 63 percent of the company, with roughly 48 percent of those shares already pledged and the cash already disbursed. So the 4.17 percent is not new cash coming in for working capital, it’s just a shift in who holds the pledge.

Concal highlights:

Due to silver price sky rackets and it effected the solar companies a lot. All the prices passed through customer and there is no slowdown in projects, seems encouraging. Very positive news on commodity side instead of silver shifting to copper, which technology already exist and adopt by top players gives some relief.

Main reason for margin drop due to project execution as mostly government projects. Management confident to keep EBITA margins at 20%

As per management, they have enough projects for upto fy28-29 and confident that there is no slowdown in demand upto next decade. As I heard something similar from waree to but, street thinking overcapacity may trouble the industry as there is no much demand visible after fy29. However, Vikram faces outstanding order book slowdown in q-to-q

Current booking stood at 10.58GW followed by IPP 55%, C&I 21% remain goverment EPC. Management is working to reduce percentage on government EPC and focusing more on private orders.

Capax side:

Total capax 6400cr out of it 3400cr debt, IPO proceeds 1500cr remain internal arrangements. I am bit confused on BESS part as they announced 4300cr capex requirement part if 6400cr or exclude.

Management gave a clarification on that. BESS is exclude so total capax stood at 10,000+ cr out of it, debt going to be 2800cr for BESS so total debt funding would be around 6000cr plus all these realised next two years.

Total 300cr already capax done in q3, expecting to spend 900cr in q4.

Future Outlook:

Next year, Vikram’s cell factory will be operational, reducing dependency on outsourced cells. This should protect margins. As per management, they can compit with global level for exporting cells. Recent EU deal would be plus point for Vikram in coming years.

EBITA margins in the range of 20%

Future orders demand on DCR side 30-35 GW, non DCR 104GW. Addressable growth trajectory available for next 5-6 quaters

Due to huge capacity announcement by competitors as well as Vikram. I believe, there going to price swings on offering products. As per management it’s not there but street expecting this will happen near future.

On debt part, massive 6000cr plus debt where current market cap 7500cr. That’s massive.

Despite all of it, Vikram Solar looks well-positioned with a strong order book, healthy margins, and ambitious growth plans, though its heavy debt and large ongoing capex are key risks to keep an eye on.

Note: I’m holding a small tracking position, down about 28%, and not planning to buy or sell for now.