Vesuvius India (known as Vesuvius Refractories Ltd before November 1992) was incorporated in September 1991. The company is promoted by the Vesuvius group, UK, which accounts for about two-thirds of the worlds continuous cast refractory market. The Vesuvius group is part of the Cookson group of companies, which is into ceramics, electronics, and precious metals.

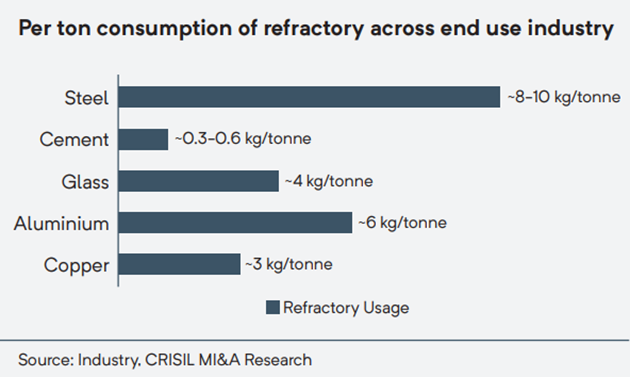

Vesuvius India manufactures specialty ceramics, refractory products, and control systems for industrial applications. It primarily caters to the steel and foundry industry in the process of continuous casting of steel and transfer of molten materials. The company also supplies refractory products for application in industries such as aluminum, cement, lime, mineral processing, hydrocarbon processing, and power generation. It has factories at Kolkata, Mehsana, and 2 plants in Visakhapatnam…

The Vesuvius Group continues to consolidate its positions in India, China and South America, their three strategic areas of development, and has been extremely supportive of their Indian operations and continues to provide constant support in terms of technology, systems, manufacturing etc.

Chairman : Mr Biswadip Gupta is a BE (Metallurgy) and MBA and has over 44 years’ experience in the steel and refractory industry. He is associated with the Vesuvius Group since 1979 and was instrumental in setting up the Indian operations.

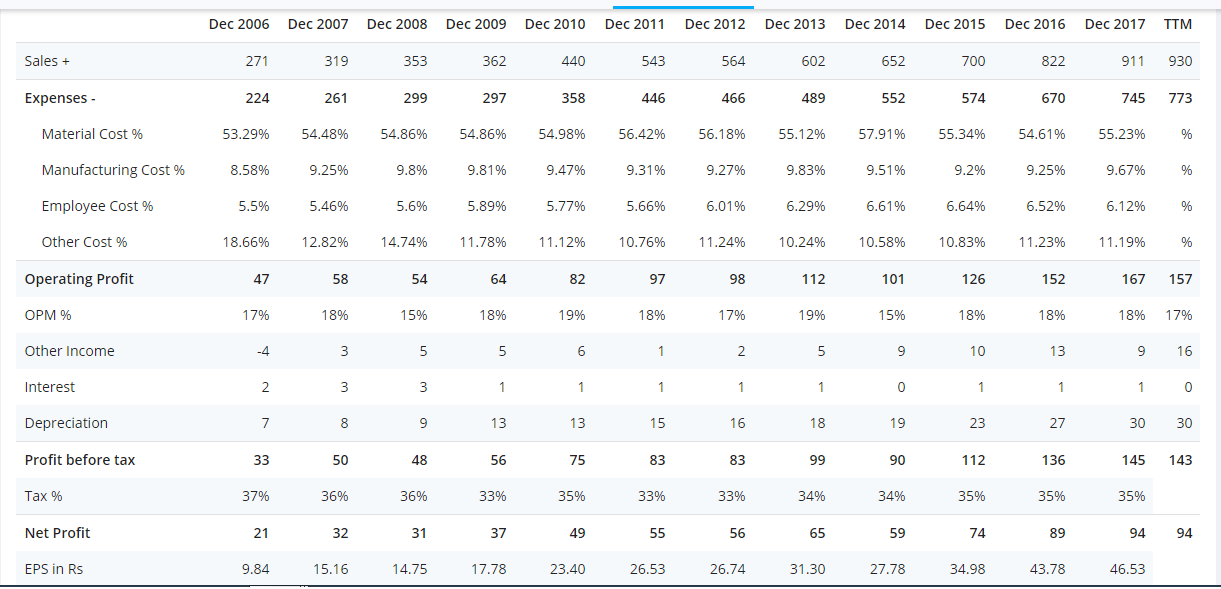

Company follows Dec to Dec Calender and thus most of the details available are as of December 2017.

The Company has shown good growth in past.

Compounded Sales Growth around 10% over 3 , 5 , 10 Year Period.

Compounded Profit Growth 10% over 3 , 5 , 10 Year period

ROEs around 15%

ROCE around 25%

Company is debt free and promoter holding around 56% without pledge.

MFs (Reliance , Sundaram and HDFC) own around 20%

No equity dilution

Dividends paid around 15-20% of profits on consistent Basis

345 Cr of Cash and Equivalents on Dec 2017

The constant OPMs and Sales are very consistent and does not give any impression of cyclical nature of the business.

Orient Refractories , Foseco also have similar quite of growth with strong Foreign Parentage.

Negatives :

CSR spend is 0.27% of Profits

Receivable of Rs 20 Cr from certain customers currently under insolvency proceedings under the Insolvency and Bankruptcy Code, 2016 which the Company considers good and recoverable.

Related Party Sales : 101 Cr (Around 11% of total Sales)

Related Party Purchase : 112 Cr

Vesuvius products have a short service life due to wear caused by the high temperature, high thermal cycling and the erosive and corrosive attacks they suffer. Due to the specialised nature of our products and the high volume in which these products are consumed, Vesuvius has developed close, collaborative relationships with customers together with an extended global manufacturing network aligned with customer locations. Vesuvius focuses on gaining a fundamental understanding of customers’ processes and delivering systems and products that are mission-critical for the demanding applications in which they are used. ~ AR2017

@hitesh2710 @ayushmit Looking to know your views that how do you see these companies like Foseco , Orient Refractories and Vesuvius. How one should approach towards these companies. The ARs hardly provide any greater details about the business.