VEDAVAAG Systems India Limited is setup in the year 1998 and over the years evolved as a niche player of e-governance solutions and citizen services infrastructure management.

VEDAVAAG went public in the year 2000 and got listed in Bangalore and Hyderabad stock exchanges. The company during the initial days executed many intranet and client specific applications for customers such as Andhra Bank, Oriental Bank of Commerce, Nokia, Web Sprocket Inc, Information Logistics, Singapore and others. VEDAVAAG built strategic relationship with Electronics Corporation of India (ECIL), a public sector undertaking to reach out into e-governance sector.

VEDAVAAG bagged its first project in e-Governance solutions along with ECIL in year 2001 to execute a five year contract for computerized bus pass services for Delhi Transport Corporations and went on to bag similar contracts from many other state road transport undertakings in Tamilnadu, Karnataka and Maharashtra.

VEDAVAAG has built well acclaimed solutions for local body management - for municipal e-governance – covering Panchayats, Nagar Palikas and Municipal Corporations. VEDAVAAG bagged its first project to deliver local body e-governance solutions to Municipal Corporation of Delhi in the year 2003 and that paved way for VEDAVAAGs growth in to e-Governance sector in a big way.

VEDAVAAG has setup over 2000 citizen services centers in Delhi, Haryana and Bihar to reach out to people. These centers have been setup under the Government of India Mandate to provide various G2C, B2C and B2B services. VEDAVAAG has launched various citizen services under the brand ABHEE and proposal is on to setup these centers are free standing units on franchise basis.

VEDAVAAG is certified for ISO 9001:2008 for its e-Governance applications delivery and services management since 2006.

VEDAVAAG got listed in Mumbai Stock Exchange in April, 2009. The company did a turnover of Rs 10.6 Cr in the year 2008-09. VEDAVAAG expects to make quantum jump into performance in the years to come as it completed Common Service Centers roll out in the current year.

From the latest AR vedavaag is the buisness correspondent for SBI.

My theme for investment:

Strengths:

-

All government related documentation and data , and various services is being digitised eg aadhar, birth and death certificate, jobs,entrance exams , banks, e commerce, loans, pensions etc these offer ease for both government and the citizens and also the service providers to reduce cost and provide their services to a wider audience without significant expenses.

-

CSC will be relevant as it will act as interface between digital and human as biometric scans, holographs check, cash payments , cash deposits, package delivery centres for amazon. assisted Purchase centers for amazon etc. etc needs physical interface,

-

Limited CSC’s in a area. Competitors wont enter in a area where another company is a CSC as it wont be profitable for both. So the areas covered by a CSC will have a first mover advantage. Also not sure if government will allow multiple CSC’s in a area as already allotments are complete.

-

No debt

-

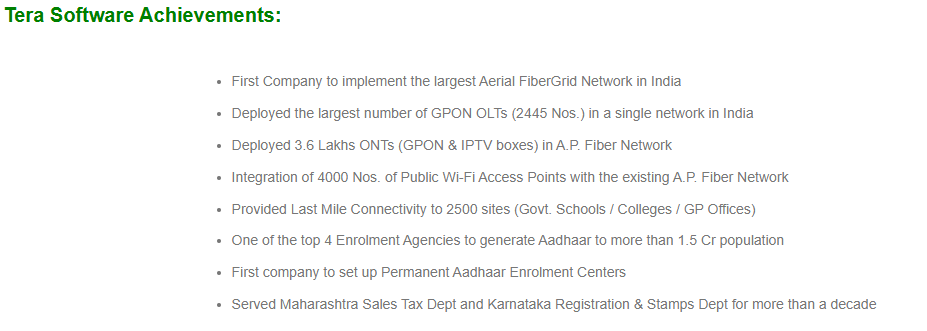

Conservative Management, No future guidelines due to the uncertainity. Dont give guidelines of 2000cr revenues by 2020 like Tera Software . These are the management who are more likely to fake it when they dont make it.

-

In future CSC’s will play a pivotal role in bringing rural areas to the mainstream. The CSC’s are the metaphorfical pipelines/railroads that once laid will provide a steady revenue stream in the future. As of now only 5 companies that are listed have presence in the CSC market. What I found are the below.

a. Vakrangee - P/E 26 they are the most innnovative and focused in utilising this network.

b. Aksh optifibre - Significant presence in Rajasthan - P/E of 10.

c. Vedavaag - Significant presence in Bihar, Delhi, Haryana, Small cap company at 12 P/E.

d. SREI sahaj- Big company so CSC wont offer much difference to the overall revenues.

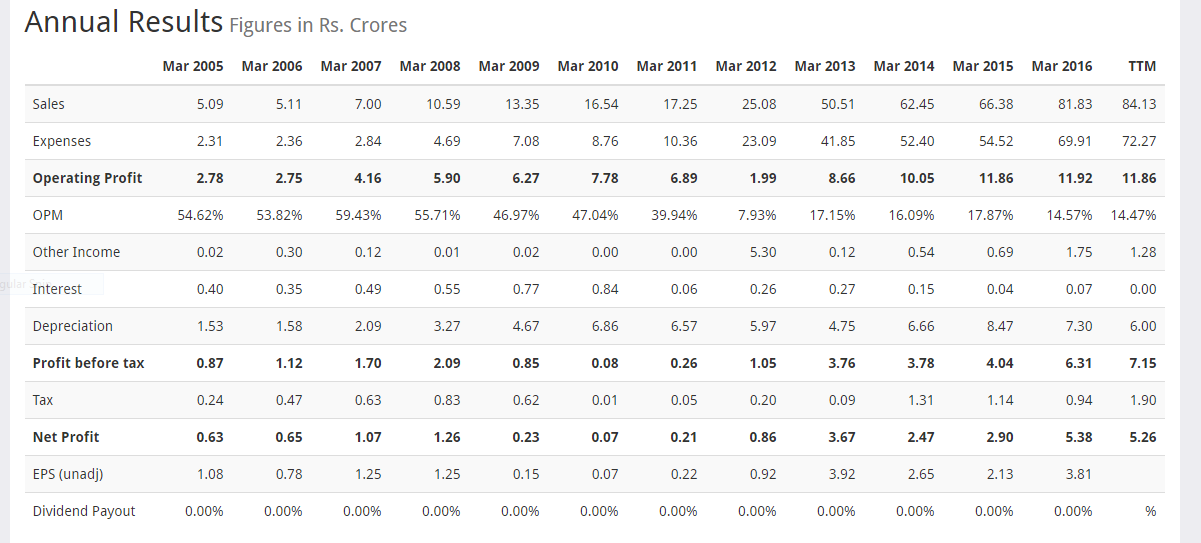

e. Tera Software - Only few CSC , also Management seems untrustworthy.

So that leaves us with Vedavaag and Aksh Optifibre.

There are multiple ways this value can be unlocked.

- Sale of the E governance division e.g SREI sahaj model

- Company realises the gold mine they are sitting on and utilises it to the fullest like Vakrangee.

- Various Private players like retailers and service providers realise this goldmine and offer services through these CSC. E.g Amazon partnering with Vakrangee and Banks setting them up as Buisness Correspondent.

Valuation

Considering a monthly profit of Rs 2500 ( after 70% to the Franchise and all operating costs ) for 1 CSC of Vedavaag.

=2500x12

=30000/ year

Considering that we expect a 10% return on investment amount while valuing a single CSC. The Valuation will be (30000/10) x 100 = 3L / CSC

Now Vedavaag has 2000 CSC. So 3L x 2000 = 60 Cr. Company is now valued at 60cr. So we are getting the projects division for free.

Similarly Aksh optifibre will be valued at 3L x 10000 = 300 Cr only for the CSC’s not considering the OFC division.

Opportunities:

-

Note that we havent considered e governance projects revenues that it provides for other government services.

-

Also 2500/ month profit is a very conservative estimate and may increase exponentially in future.

Weakness:

-

Buisness depends on the Village level enterprenuer and so not relaible.

-

Difficult to ensure control over a large network as these companies dont have relevant expeirence and manpower.

-

Buisness model may be flawed.

-

Companies may not be able to utilise the opputunity as their core buisness is different.

Threats:

-

Other competitors coming in. Aggresive play by Vakrangee.

-

Prices for e gov services regulated by Government , Hence may be just break even and not as profitable as calculated.

-

Failure to attract Private service providers who may provide value addition.

-

Disruption by Technology.

-

Small cap company so shares traded are very few and liquidity is a problem. Always locked in UC now.

Mods may please suggest any changes and I shall make the same. Wrote this a bit in hurry so all detailed data might not be attached.

Disc: Invested in Both Vedavaag and Aksh