HZL interim dividend, Board meeting on coming Tuesday

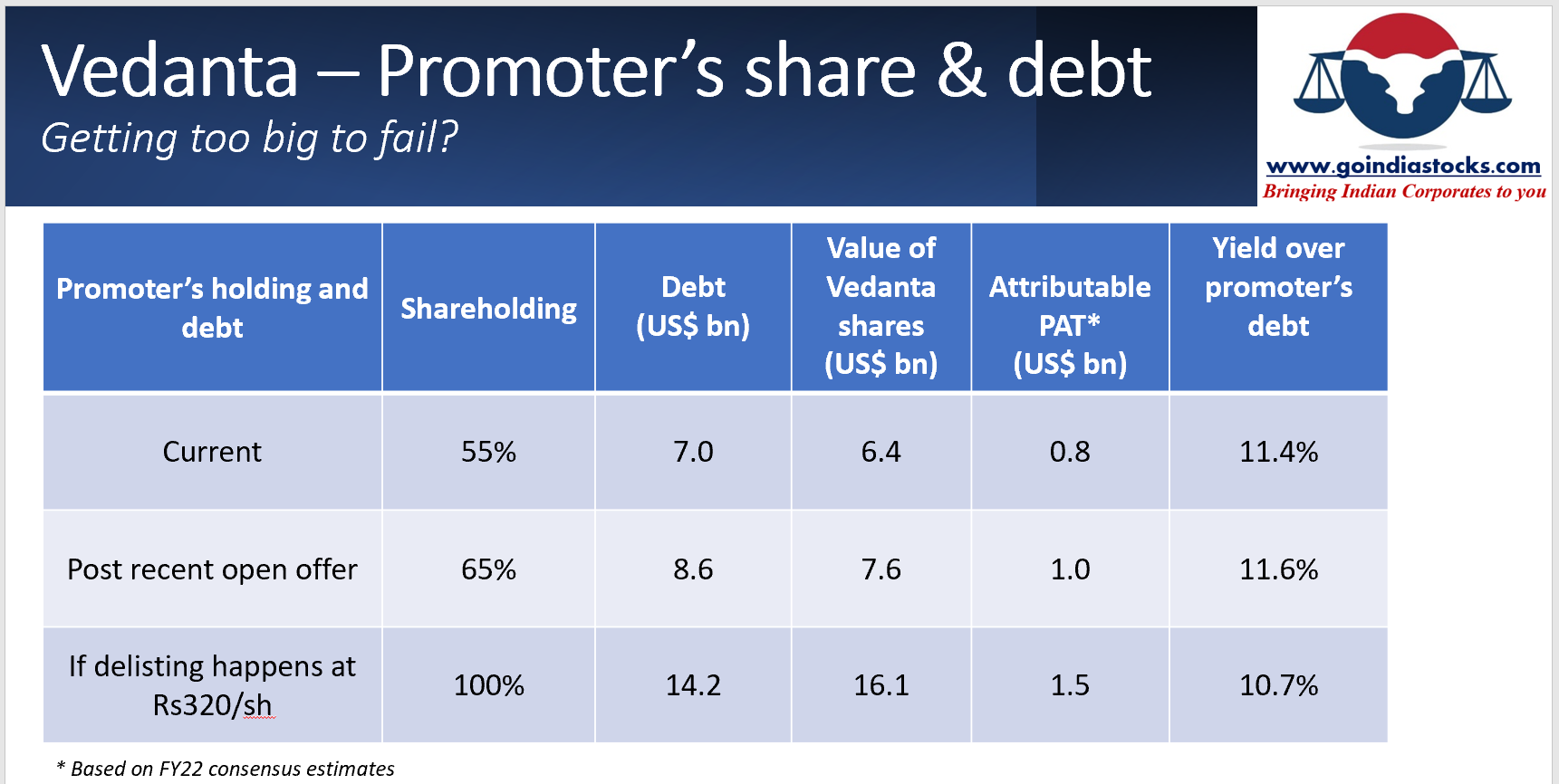

Sources tell ET NOW that Vedanta Ltd promoters, Vedanta Resources are mulling an upping stake in Vedanta Ltd by another 10% in the months to come. This comes after the promoter last week picked up a 5% stake from the open market, increasing their shareholding to about 55%. SEBI Regulations allow for the promoter to increase their stake via a creeping acquisition by up to 5% in one fiscal year without having to launch an open offer. In June this year, SEBI enhanced this limit to 10%. Thus Vedanta’s promoters have the headroom to up their stake by another 5% by March 2021. At the beginning of the next fiscal year in April 2021, the promoters can pick up yet another 5%. This can potentially increase the promoter holding in Vedanta Ltd to 65%. If SEBI extends this higher limit of 10% for creeping acquisition to FY22, then the promoter can even increase their stake to 70%. In Oct, Vedanta Resources made a failed attempt to delist Vedanta Limited, for the purpose of which it had accumulated a debt of about $3 bn. This financial ammunition may now be used to increase the stake in Vedanta Ltd. As per SEBI regulations, the promoter can make another delisting offer after one year.

Vedanta PLC has borrowed US$400mn from Oaktree for the 5% purchase of Vedanta Ltd. The return requirement for funds like Oaktree is usually around 13-16% dollar returns. Not sure what the game plan is here for Vedanta promoters.

Btw it is interesting to note that of all the block deals seen on exchanges only buyer is shown while there is no large seller? Where did all this stock come from? Lots of questions!

Vedanta has announced a voluntary open offer for acquisition of another 10% from the public share holders. This is in addition to the recently acquired 5% through creeping acquisition. If successful, this would take the promoter holding to 65%.

The indicated price is Rs. 160/- per share. This price is however only indicative & is likely to be raised before the open offer to make it attractive for shareholders to tender their shares. One thing appears quite certain & that is that the promoters are determined to take their stake higher & so will ensure that unlike the failed de-listing a few months ago, the open offer will succeed whatever the cost. Post April 2021, the promoters will again be eligible for creeping acquisition. I expect the promoters to make another de-listing attempt next year & this time they will make sure it goes through.

The commodity cycle has turned & no one understands this better than the promoters. As their stake goes higher, the outstanding shares keep coming down. This enables the promoters to acquire them at a higher price & still only marginally increasing their overall cost. It makes sense for retail investors not to be in a hurry to let go their shares. In fact, to me it appears to be an attractive buy at current levels of 180/- with a years horizon.

Now what  ??

??

The Vedanta story is unfolding along expected lines. It is up 25% in the last couple of months with the open offer price revised to 235, again along expected lines. The open offer has been increased to about 17% of the balance equity held by the non promoters. If the open offer succeeds, it will take the promoter stake to about 72%.

I would be pleasantly surprised if the promoters are able to garner the entire 17%, but if they do succeed, it would take them very close to the maximum permissible limit of 75%. I expect the promoters to have another shot at de-listing within the next 6-8 months post the current open offer. Needless to say, this time they will not fail to reach the magical figure of 90%, regardless of the cost involved as the increased cost will be limited to that many fewer shares since they would already have close to 70% stake post the current open offer. The promoters are raising capital at exorbitantly high costs for the current buy back, which only makes sense if they are going to go the whole hog

& manage to get the Co. de-listed.

I expect to see appreciably higher levels within the next 8-10 months. Perhaps it makes sense not to offer ones entire holdings in the current open offer.

Very much agree to this thesis. Was doing some numbers on the cost to promoter as they increase the offer for remaining stake. Doesn’t change much and probably now they have no going back either

Source:How desperate is promoter?

MMDR bill got amended again in 2021. The amendment looks like it will be beneficial to the mining companies. (removal of captive and non-captive mines distinction)

Does anyone have analysis / ideas on how this could impact Vedanta?

Summary of the amendment

https://prsindia.org/billtrack/the-mines-and-minerals-development-and-regulation-amendment-bill-2021

Disclosure: I am invested in Vedanta

No impact, Vedanta is short of mining capacity on captive requirement so they don’t have surplus to sell. In fact, now when they bid for mines for captive use, they will face more competition from merchant miners

@RajeevJ Thanks for your valuable insight. What happens after promoters reach 75%. Do they need to buy from us via open market/offline trade. May be a nube question.

What will happen to shares which we did not render in open offer?

Disclosure: Invested.

I bought Vedanta last year in March-Apr time before the delisting was announced. (60ish) then added more once the delisting was announced.

Reasoning - commodity bull run coming. Plus Vedanta produces silver and I believe gold and silver will go up due to inflation and money printing.

The delisting bid and the desperation shown by the prompter confirmed my thesis. The prompter company even sold a dollar denominated debt for 1 billion plus in order to increase it’s share in Vedanta for 13 percent interest rate. Imagine that. The interest rates world wide are zero, 17 trillion of negative yielding debt etc. At the same time this prompter is issuing debt at 13 percent simply to aquire the stock of Vedanta and take it private?

This commodity cycle is going to be huge one for multiple years. So I hope Vedanta doesn’t go private. But if the promoter manages to buy stock and finally delist I will hold it till the end.

If a company is delisted and you didn’t tender the stock, you still get 1 year of time to tender the stock to the promoter at the same price that it was delisted at.

So the strategy is going to work out.

If the promoter tries to delist and it fails the second time, it is good too. But mostly it won’t fail this time

Came across this article.

If this goes through, India may again become a Copper exporter.

Can be a real big trigger for Vedanta Stock!!!

In the recent earnings call of Vedanta (Q1 FY- 2022) the board made it clear that priority is to deleverage Vedanta ltd. and the parent (VRL) as well. And the most likely available option is dividend from Vedanta (both, from free cash flow and may be borrowings passed on as dividend to parent). Additionally, it was also made clear that the time line to pass on last dividend from Hindustan Zinc is 31st Oct (11 months from declaration I suppose).

Going by the above comments (made in earnings call by management), can we expect good dividend in near future. Would love to hear from others.

Disc: Invested

Vednata declared dividend of Rs.18.5 yesterday. This was what they got from Hindustan Zinc last October and technically, they were suppose to pass it on to Vedanta shareholders as per there policy.

As the parent (VRL) is highly leveraged and there is decent cash on books of Vedanta and Hindustan Zinc, I believe, the company may go for few more rounds of dividend or they may try for delisting as well. To sum up, parent need access to cash. This is what I think, would welcome any other opinion.

One more instance

It’s anyone holding Vedanta stock following the SAST disclosures being made by the company?

I am sitting on some nice profits in Vedanta. Bought around 90 in 2020. I was planning to hold onto them till the commodity bull market plays out.

However, it seems every day there is some SAST disclosure by the company. Some promoter related entity is doing some transaction or the other. Keeping up with these disclosures it’s exhausting and I can’t understand what they are doing really. Seems the promoters are just doing these transactions instead of actually running the company.

I am holding since 90 … did partial exit at 310… Still holding big chunk…promoter is increasing stake at every opportunity so they can get more div to reduce debt at vadanta resources the parent… I am still bullish as non ferrous metals are still in bullish run…one more year of these high prices and vedanta resources the parent will get hugely deleveraged and we will see the governence improve …as they say governance is also cyclical… They is also a proposal for demerger…not sure of the merits at this point…vedanta main issue is debt level at parent…