Results announced

At first glance, encouraging. Need to study more closely.

Results announced

At first glance, encouraging. Need to study more closely.

Yes, the results are good. The EPC division has done particularly well. But its still a long road to complete recovery and there is always a chance of relapse if things are not managed well.

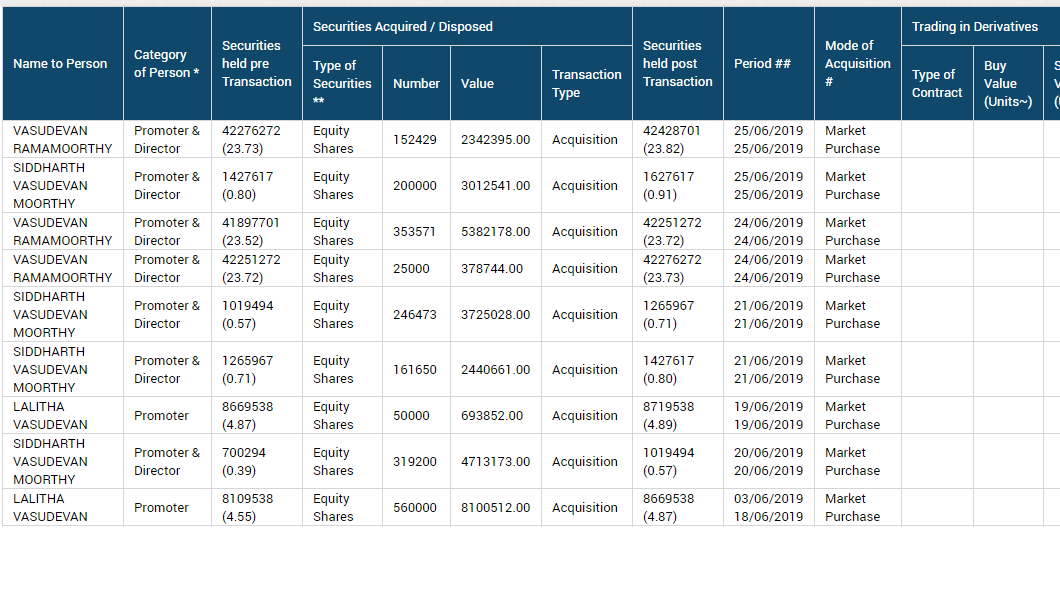

Land sold for 170cr in which vascon holds 50% share.

Anyone still tracking this company? @bheeshma ? I regret I was unable to keep up with the developments owing to personal reasons. While I will try to dig out some information, any help would be appreciated.

Thanks

Sandeep

Investor Presentation for November 2020 is here: https://www.bseindia.com/xml-data/corpfiling/AttachHis/a6789d53-9a3b-44e8-b07e-2d0955ac502c.pdf

Some highlights:

-Total order book Rs 1972 Crs

-High amount of govt projects - 75%

Now does the high percentage of govt projects signify a positive or otherwise? My concern is regarding the potential for delay in payments for such projects.

Note to self - Examination of following is required:

The company has been experiencing continuous losses for the past four quarters and profitable quarters are relatively few. Is there any hope for the future?

Continuously pledged shares of promoters - reasons?

I will try to find info on the above (and other issues). I will appreciate any help particularly as I am a novice. Please also point out any errors, or even the direction I should take to dig deeper into the subject.

Thanks

Sandeep

Hi @Sandokan

The cos real estate division hasn’t really taken off as was planned. They have a good EPC order book but their ability to bid on tenders is constrained by their bank guarantee levels as was the case in the past as well. The debt levels are also About 250 crs at a gross level. The cash flow generated from the sales of Windermere units are going to be used to get the debt levels down going forward and mgt has mentioned that they saw some 35-40cr of sales happen in that project. All in all, I think it will take a while for the co to climb out of the previous downcycle.

Investor presentation for Feb 2021 is here: https://www.bseindia.com/xml-data/corpfiling/AttachLive/0e982f1c-a709-4aaa-88e9-2c6fa84d78ce.pdf

Results Dec 20 are here: https://www.bseindia.com/xml-data/corpfiling/AttachLive/421d5aa1-449d-4fa3-b0e6-185f9c684299.pdf

Not very encouraging. Time to exit?

I had posted a frivolous comment in reply to this post. My apologies.

VASCON ENGINEERS.docx (24.1 KB)

Looks like a real Turnaround opportunity. Comments, contrary viewpoints invited.

Disclosure: Invested

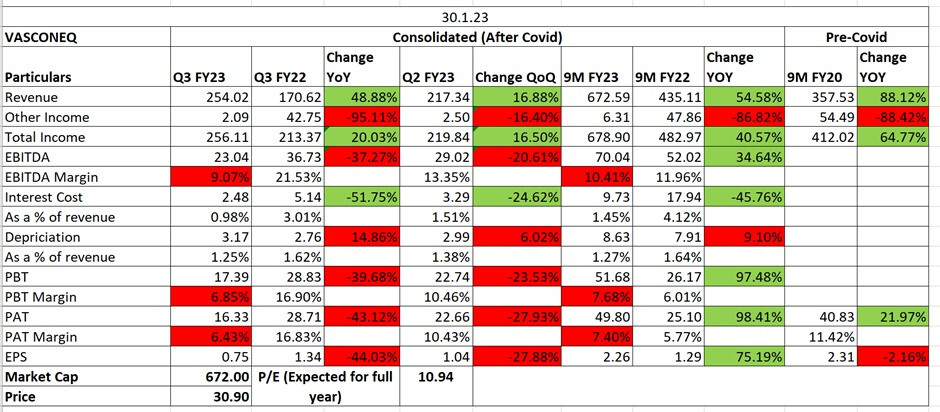

Q1FY24 CONCALL NOTES:

• Our improved funding position: As we have been informing you, our credit rating has been improving and with CRISIL rating has been upgraded to BBB+ from BBB for long-term facilities and has been upgraded to A2 from A3+ for short-term facilities. We have commenced applying for enhanced BG limits also. We are happy to report that we are in the final stages of getting those limits enhanced, and this will allow us to significantly increase our order book position and continue the EPC execution run rate.

• Currently, the company has a working capital limit of INR 300 Crores as of Q1 FY24 and expect to increase this limit to INR 400 Crores by end of this year. The ratings have also helped us negotiate better interest rates, which we are currently doing with the banks.

• We are hopeful to bag a couple of orders in the next two months, three months, which will increase the order book by more than INR 1,500 Crores. We are very much on the verge of bagging more than INR 1,500 Crores of orders. We are at the last stages of negotiation in quite a few projects at this point of time, and we can hopefully look forward to some announcements in the next few weeks. And yes, we will be targeting to have an order book closer to INR 3,000 Crores rather than INR 2,000 Crores because next year, we want to grow our EPC revenue to at least INR 1,000 Crores. And for that, we need to start the year with INR 3,000 Crores order book. So that is definitely a target, and we will achieve that.

• Execution of new orders will have a positive impact on revenue from second half of the year. So we are expecting our quarter 3 and quarter 4 because few projects that we bagged early this year in January and February, those needed environmental clearances, tree cutting, etc. These are in process, they’re almost done. So we expect to start work on the Pune Police Housing in September and also on the PMRDA project that we bagged in September. So both of these will give us added revenues in Q3, Q4 compared to last year. And so, that is why we hope to catch up. You’re right, we’ve just grown about 7% in Q1 and Q2 might be pretty much similar. But Q3, Q4, we expect our run rate to be more than last year.

• Last year, we had certain BG constraints, and we couldn’t exceed our order booking target. We have increased our BG limit this year by about INR 40 Crores - INR 50 Crores. And we are in the process of now getting further increased new assessment based on our last year’s balance sheet, which has significantly improved compared to the year before that. So these improvements with the banking facilities are going on currently, our rating has improved. So we are very now positive that in the next three- four months, we’ll have much higher BG limits and lesser constraints to book orders.

• I keep saying this that our real estate division is like a glorified EPC. We do not want to be putting our own equity or borrowing much on these projects. So we will be looking at methods where we have an equity partner. And then we will execute the project.

• EPC Growth guidance : We’ve been talking about 10% to 15%. So we expect this year, the growth to remain in that range. But next year, we intend to jump straight to INR 1,000 Crores for the EPC.

• GMP: So we are just at the last phase of starting operation of another plant also. So it will start operations from August onward or so. So the run rate will be continued, and we are expecting, on a Y-o-Y basis, if you compare to last year, our performance in GMP we are expecting almost 10% to 15% growth in the top line and almost 20% growth in the bottom line. So our order book and everything is very well placed to take this thing up. But first quarter due to this slightly droppage of the backward integration with the client, slight bit of drop happened in terms of the GMP is concerned.

• I wanted to know if all your real estate projects, the EPC orders come to you or they also executed outside? Santosh Sundararajan: So wherever we have partners, a process of initiating an arm’s length quotation and discussion will always happen. So far, we have managed to bag wherever we are in the driving seat, of course, we get the first site of refusal. Yes, so far, actually, all these orders have been coming to us.

• INR 500 Crores internal order is very much in hand over the next 8 - 12 months, any projects get launched, which will add up to our EPC order book internally as well, you’re right.

• Thane Land: Owns 45% of 150acres of land in Thane. Government road is expected to pass through 40 acres of land. Expecting 5-6cr per acre from Government. And 3cr from other land. 550cr sales potential from the land.

• Still we expect completions for a couple of projects, we should do upwards of INR 150 Crores – INR 200 Crores in FY25 from real estate. And from FY '26 onwards, that run rate should be steady and continuing to grow.

• The first question on commercial, as far as Vascon is concerned, we launched a commercial project in Kharadi. We intend to launch one in Baner, but we are not in business of holding commercial assets and leasing them. Even if we at all have a leasing model, we would lease and then discount the lease and sell out the asset. So we do not intend to hold on the commercial assets. We will develop them, sell and exit.

• In general, when this project gets launched, what is your percentage of booking that happens? I mean, for every real estate company, they have got this right, 25%, 30% that comes in launch itself. What is your rate, I mean, historically? Santosh Sundararajan: Yes, about 25% to 30%, in fact, more than 30% sometimes, 35% we do end up booking when we launch.

• Powai and Baner, we expected to commence in this current financial year. Vignesh Iyer: Thane? Santosh Sundararajan: Yes, Powai, Baner, Santacruz, yes, we will be launching it in this financial year. Somnath Biswas: The Ajanta will be over by next year.

• GMP Monetization and Growth potential: There is a lot of potential in this company because with the amount of Make in India that is now finally starting to take shape with the Foxconns of the world coming to set up semiconductor industries here. And a lot of these industries will be needing clean room. GMP, the 90% exports to clean room will be health care centre, but it doesn’t take much of treating to be able to supply clean rooms to the industrial sector, to the semiconductor sector. So they are working on it. And based on that kind of growth horizon available in that industry, which is humongous, the number of factories that people intend to be putting up. So we feel that GMP will definitely have a strategic investor at some point, who will look at the bigger potential and offer us a fair price, which we will then take up and exit.

We think we can easily get anything upwards of INR 200 - INR 250 Crores equity value for the company. And then our share would be 80-85% of that.

Analyst / Investor Meet

TechnoFudna Analysis on Vascon

Fndamental Upticks

1**-Debt Reduction**-The Debt has been constantly cut down from the balance sheet and is around 142 crores.

2-Industry Tailwinds-The Real estate specially the government infrastructure which is around 75% of the order book of Vascon is growing at a very fast pace.

3-High Demand-The demand scope of real estate is at new peak with high rental yields and land rates.

Technical Upticks

1-Multi year Breakout above 61

2-Strong upmove supported by volumes

3-Strong RSI and Above 40 EMA on montlhy basis

Dis-Invested

MCap 1200cr

PE 19

PEG 0.31

Just disinvested 157cr

Has a huge land bank in Thane which is worth a gold mine!

1000cr top line

3000cr order book

CMP 58.

What is the market not liking?!

No brainier investment !

In the last 1 year, i have invested in vascon 2 times and got out with profits (40% and 20%) both times… I wanted to hold it for the long term but found a few red flags in the annual report

Vascon annual report red flags -

Very high promoter remunition - 18cr on net profit of 78cr

Debenture investment of 27cr in ascent hotep private ltd

High rate of interest on borrowings- 12-15%

Bad situation in ageing of trade receivables and payables -

100cr + receivables in 1 yr + category

Current loans given of 91cr

10cr provided as finance to related parties

Lots of related party transaction

Current valuations proving attractive. Waiting for q2 results to see cash flows and recievables situation