3 Likes

Company Has acquired 50% stake of Everest Industrial Lanka (Private) Limited.(company in Sri Lanka )

At cost of INR 320.88 Million.

This company engaged in the business of production, manufacturing, distribution and selling of commercial

visi-coolers and related accessories.

4320eb05-d1c0-4fa1-9de3-c1dc4a0dc93b.pdf (2.3 MB)

3 Likes

For most of the last year, the discourse around Varun Beverages has been dominated by just one topic – what effect Campa would have on its business. This summer would have decided that question once and for all, but that is not going to happen. The peak season has been a complete washout for the cola companies.

Without waiting for the quarter results, and at the risk of being called premature, let us therefore look at what – if any – effect Campa has had on VBL’s business so far. And whether the numbers justify the extreme pessimism we have seen in the analyst commentary for more than year now.

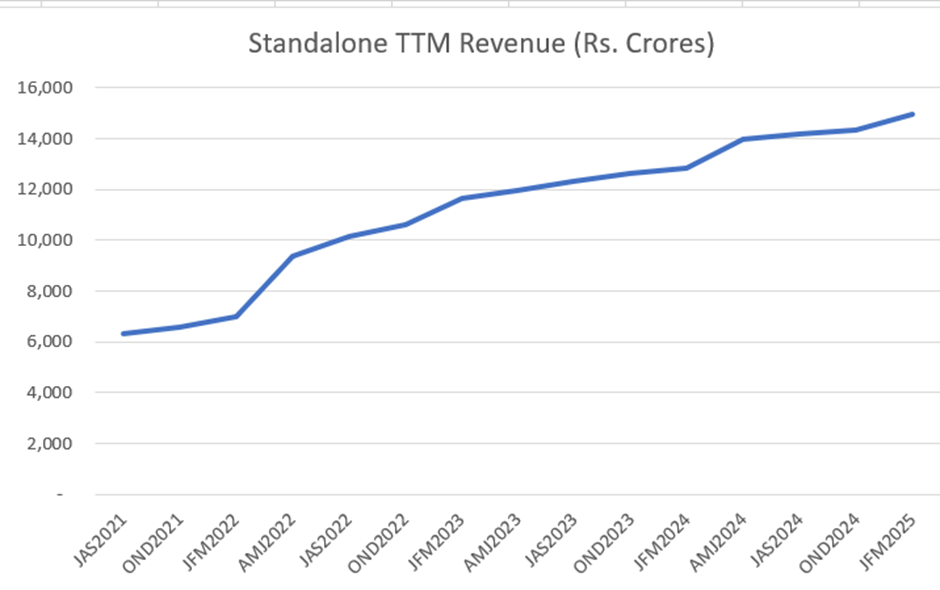

We should look at the standalone financials of VBL.

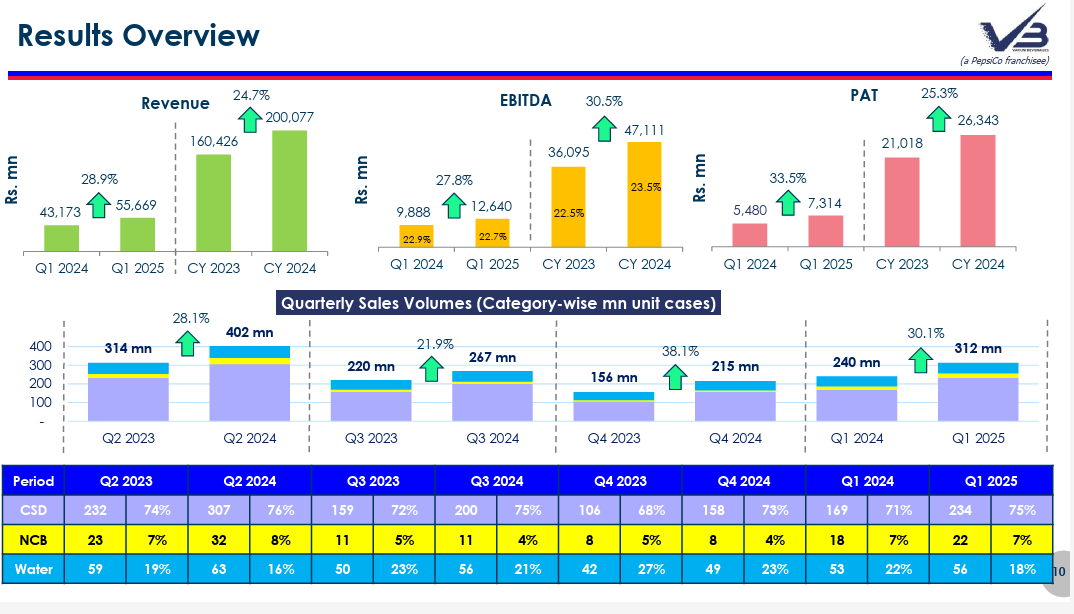

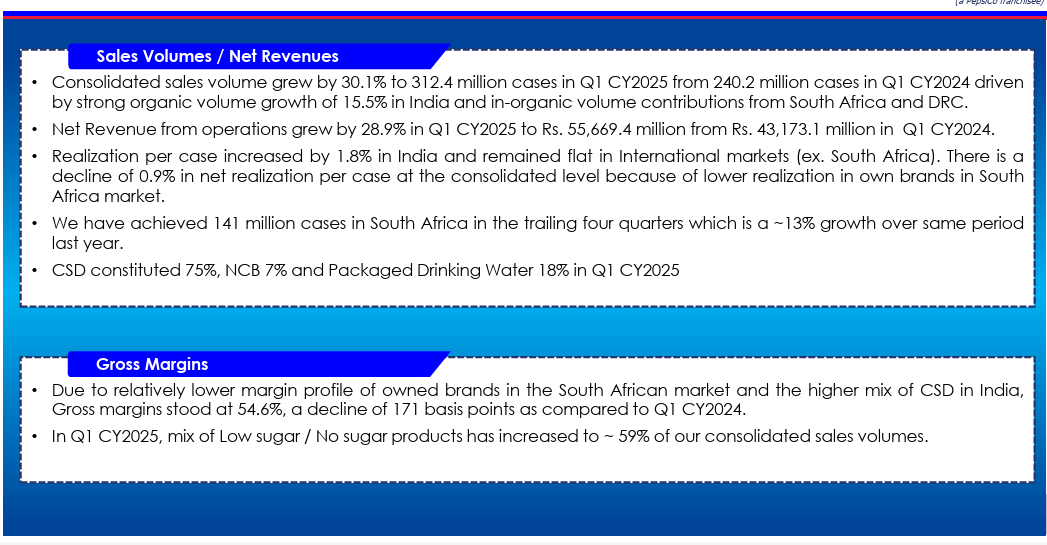

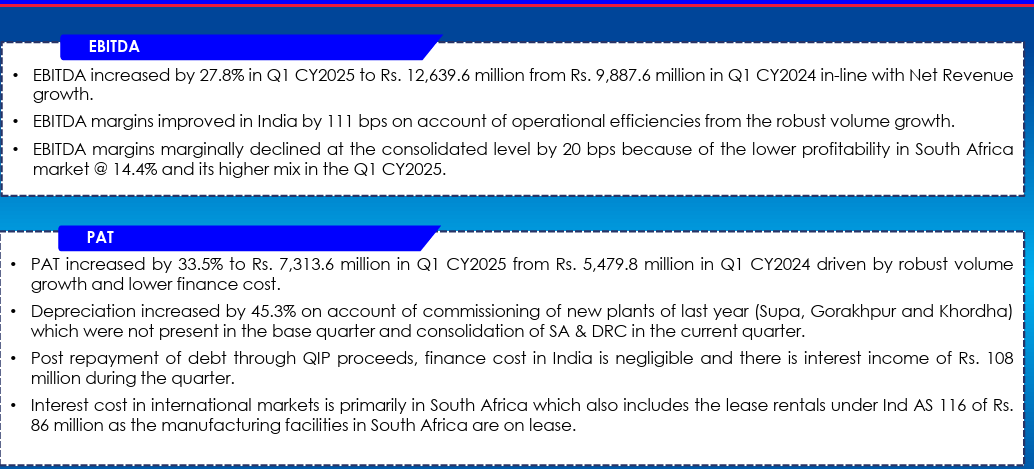

As per the Q1 CY25 results, the company reported organic volume growth of 15.5 % in India while revenue growth was 17.60 %. Realisation per case improved 1.8 %. EBITDA margins improved by 111 bps, while PBT has grown by 42.41 % YoY. This sounds fine, but this was for the last quarter alone. We should see the trend.

Effect of competition and price war if any should show up in lower realisations or lower volume / revenue growth and depressed margins.

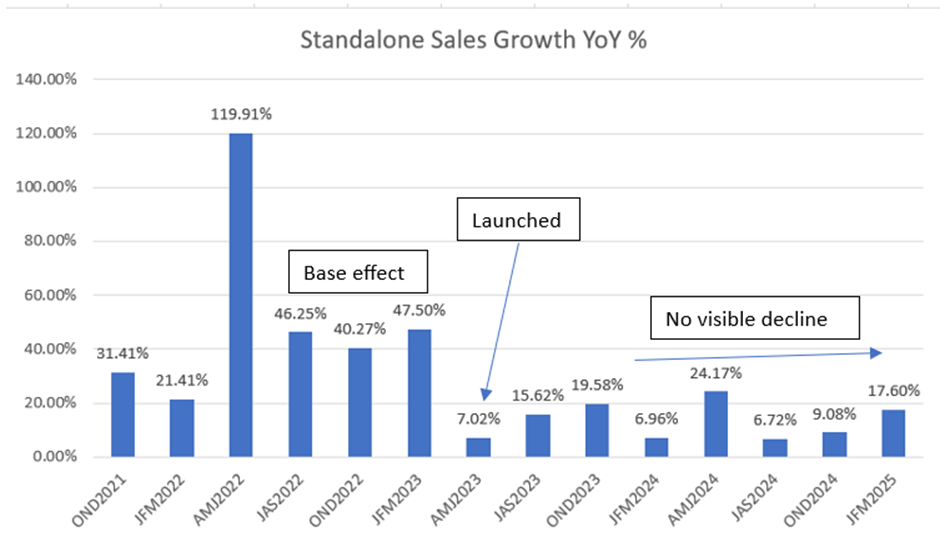

Campa was formally launched on 9th March 2023. From thereon, it would take a few quarters for Reliance to improve distribution and increase penetration. The Campa effect if any should gradually begin to be seen somewhere from late 2023 onwards.

Let us look at VBL’s revenues first.

Revenues have continued to rise, and stood at Rs.4053 crore in Q1 CY25 against Rs.3446 crore last year. TTM revenues rose further to Rs.14,955 crore.

Then, margins.

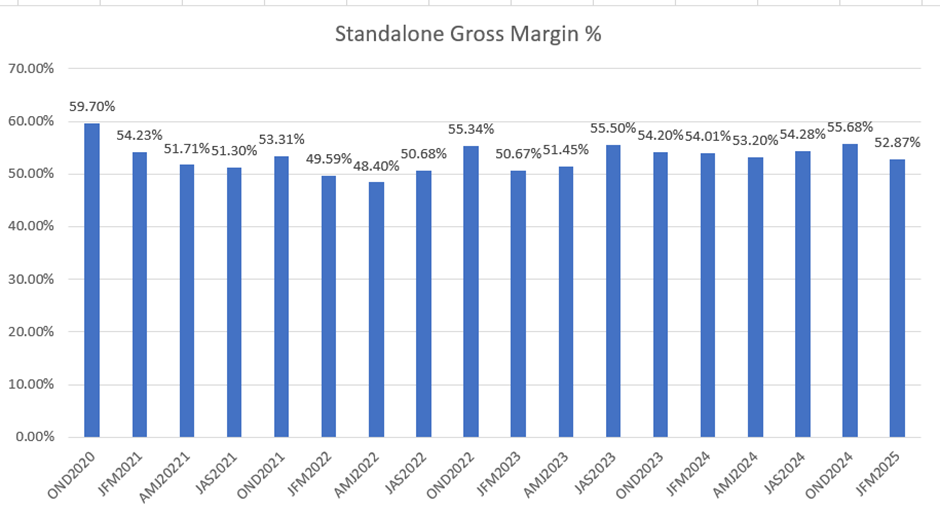

Gross margins have remained steady over the years and stood at 52.87 % in for Q1 CY2025. This is down from 54.01 % last year but still higher than 2022 & 2023. They have always hovered around the 52-53 % range. No decline here.

Finally, the Growth Rate.

Growth rate YoY has been fluctuating but there is no visible declining trend. Note that the exceptionally high growth seen in CY2022 was due to a low base of Covid in 2021 plus the benefit of new territory acquisitions in the South & West coming on stream. We are only interested in seeing whether growth is slowing as Campa gradually expands. But there is no such trend.

If competition was pinching, it should have shown up somewhere in the numbers. But data shows Varun Beverages has not seen much damage so far at least.

Both Pepsi & Coke have responded to the Campa challenge partly with price cuts and partly by flooding the market with smaller unit packs. Smaller packs make price differential between competing products less important in customer’s purchase decision, letting other factors like habit, brand familiarity and taste prevail.

I see merit in the management’s argument that as prices fall, market expands. We can see this in most of the discretionary consumption and indulgence products. For example, when fuel prices fall or milage improves, people drive more and buy bigger cars. Cheaper mobile phones have led people to buy better models, and cheaper data has meant more surfing. Same thing should happen in beverages as well, if one accepts that for most of the Indian consumers, cola is still an ‘indulgence’ product.

One good thing I notice is that Reliance has bigger ambitions. It has launched Campa in the UAE & Bahrain, plans to setup a plant in Saudi Arabia and expand into Africa and Southeast Asia. This shows Reliance is interested in growing its own business rather than play a zero-sum game and just try to defeat the incumbents in India. This is good for the industry. So long as the market is growing, this strategy poses much less of a threat to the incumbents in India.

The summer had started well with above average temperatures in end-March / early April. But later the weather – like Trump – took a complete U-turn and what we ended up with was the rainiest May we have ever seen. We never got that One Big Beautiful Summer we wanted to see. The cola giants have been forced to call a ceasefire. Investors now have no choice but to wait for one more year to see who trumps whom. Until then,

Thank you for your attention to this matter!

(Disc.: Invested)

42 Likes

Some important pointers on industry development

-

Pepsi and Coca-Cola were competing on price even before Campa’s entry. They reduced the price of 12-Rs packs to 10 (Glass botle). Then, Campa entered aggressively at 10Rs with PET, significantly increasing pricing pressure.

-

35% of the CSD market is in the 10-20Rs price point. Campa has not affected larger pack sizes (750ml+) yet.

-

Coke and Pepsi increased volume from 250 ml to 400 ml in the 20-rupee.

-

Initially, Campa struggled but leveraged nationalist sentiments, positioning as an Indian alternative, which helped penetration. Campa then matched the taste profile of established brands like Thums Up in cola and tapped into the orange segment, which Pepsi & Coke less prioritized.

- In India, Lemon is the biggest category with a much larger SKU mix, followed by Cola.

-

-

Market share

-

Campa’s market share is sub ~2-3% in select markets like TN, Telangana, penetrating markets dominated by local B-brands (45% market in TN is from B-brand).

-

Coke has lost significant market share in WB to Campa due to 10Rs pricing; Pepsi’s losses are very low. In UP, Pepsi’s market loss is very low vs Coke, because Dew has little direct competition. Thumbs Up is most affected.

-

Campa attempted to replicate Dew’s taste in North but failed. Coke & Pepsi haven’t matched Campa’s trade margins yet.

-

-

Cooler replacements are <1% across markets, esp in South India. Instead, Campa is installing coolers in smaller, less-prominent outlets not penetrated by major brands.

- Coke & Pepsi dominate visi-cooler installations (about 2:1 ratio, coke/pepsi). There is room for growth beyond Tier-2/3 cities, but low rural consumption and high distribution costs impact rapid expansion.

-

Horeca mix is ~30% to industry sales overall. Different by region: ~25-30% in TS/AP, ~45% in Mumbai.

Distributor and retailer margins

-

Campa offers higher trade margins than Pepsi and Coke. Campa gives 130 margin per case (30 bottles x 10 Rs), while Coke/Pepsi gives ~90-100.

- Of 130, wholesalers typically retain 25-35 per case and pass on 95-100 to retailers, much higher than what Pepsi/Coke offers.

Distribution & Geographic penetration

-

Campa faces distributor issues. Distributor churn is high (~65-70%), due to operational challenges. Sustainable growth and repeat sales remain low due to these inefficiencies.

-

Opex in the soft drink industry avg 14-15 per case, making distribution economically challenging, esp for low-priced 10Rs products. Campa lacks a direct distribution system and is heavily reliant on wholesalers (~80% dependency).

-

The South is not a big Coca-Cola market except for Andhra and TS. Coke has invested significantly in Visi-coolers, and Pepsi is catching up.

11 Likes

Good numbers. International business and margins have done really well

2 Likes

Few facts of the industry.

Glass is a dying segment while PET is growing.

Cans are in Fab and should be monitored as in volumes. The youth , which is the primary customer segment is the significant user of can.

Orange has never been a major category in the beverages. Mango is a larger category still not explored by campa.

Smaller packs in beverages doesn’t builds the community for you and serves as a sampling packs only. Any player with minimal/no presence in 1 litre and above packs will be a non preferred brand only.

4 Likes

Dear Vankat, How is this quarter looking like? any insight! Profits are consistently up but the price is done 30% in last 1 year. When do you see the momentum coming back. Thanks

1 Like

Saw a Pepsi Ad on the newspaper, 250ml for Rs.20 is now 400ml for Rs.20

1 Like

They introduced way back in March

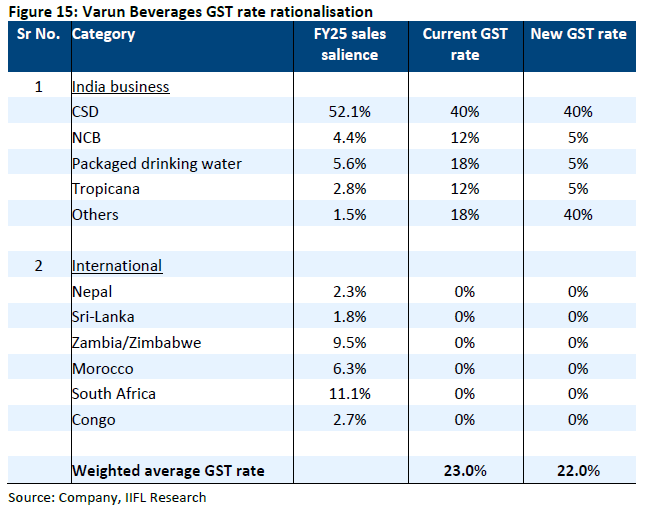

It’s anybody’s guess…weather has not been supportive, GST impact in terms of pricing is neutral although 2nd order boost in consumption might benefit the company. The only concern is competition from Campa and also from coke given the restructuring and increased focus.

Campa’s new offering Campa Sure is an added pressure on pricing for the incumbents…

I don’t see much scope for re rating in the multiple in the short term…if their execution in international markets proves good, should do good over the medium to long term

8 Likes

Varun Beverages plans to expand into RTD and AlcoBev in India and Abroad both.

Is this a strategic move to counter increase competition in softdrinks space?

11 Likes

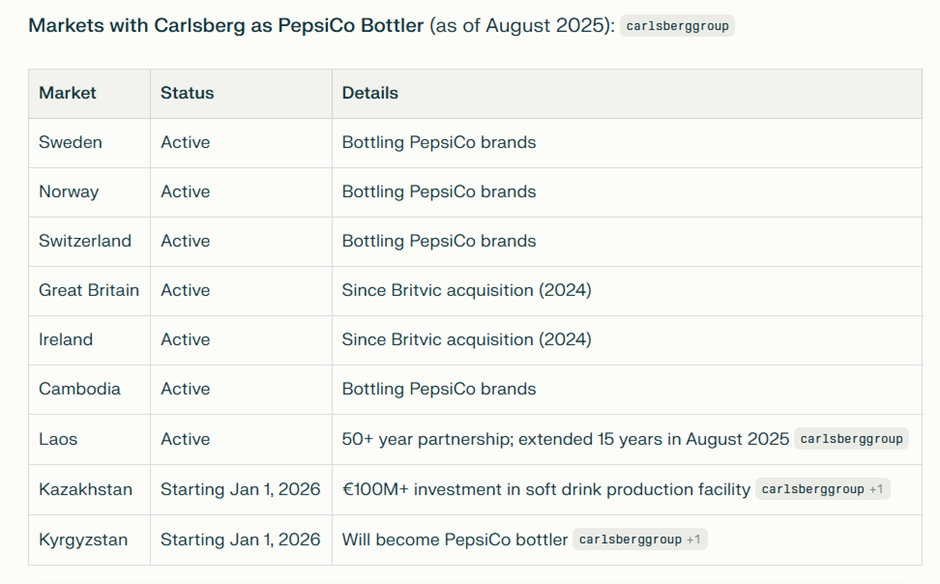

This is interesting and was new to me at least. PepsiCo and Carlsberg have an existing partnership, with Carlsberg operating as PepsiCo’s bottling partner in several countries!

It is not clear if PepsiCo played any role in facilitating the tie-up announced by Varun Beverages yesterday. But even if not, the fact that VBL is a trusted PepsiCo partner must have surely made the decision to go along with it a bit easier for Carlsberg management.

Another good thing is that Carlsberg currently has very minimal presence in Africa, with companies like Heineken and AB InBev having a much larger presence. Any revenue that VBL generates will be an incremental gain to Carlsberg. This makes the tie-up a win-win for both VBL and Carlsberg.

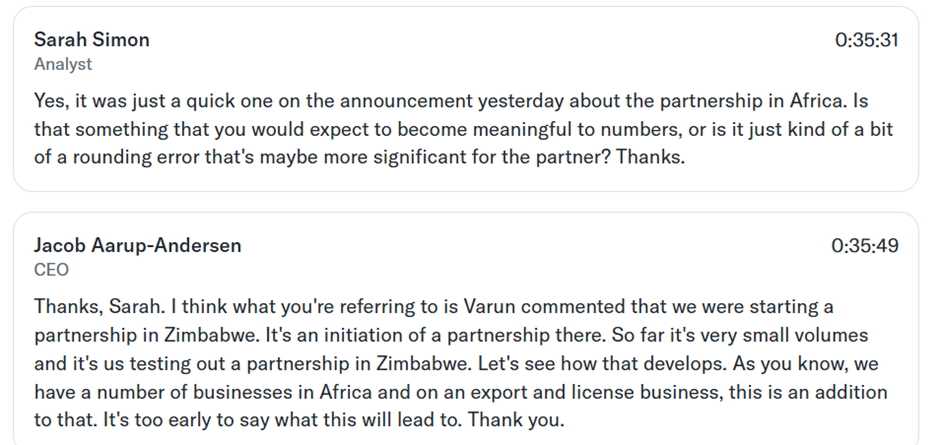

A point to note is that while VBL announced the tie-up yesterday, Carlsberg made no parallel announcement from their side. But Carlsberg had their Q3 results today and there was a question on this in their analyst call. The management clarified that the partnership would start with Zimbabwe.

Overall, nothing much should be expected from this in the near term, but in the long run this certainly opens up a whole new world of possibilities for Varun Beverages. A big positive for sure.

(Disc.: Invested)

12 Likes

VBL’s African subsidiaries will “test-market beer” under Carlsberg’s brand in those territories.

The agreement cited is distribution/exclusive distribution or test-marketing rather than a full bottler/manufacturer integration in all cases.

The business model for beer/alcohol is somewhat different vs soft drinks: regulatory risks, margins, competition, taxation differ. Still i feel they will be Sucessful and Expand More in this.

(DISC: NO RECO, INVESTED)

4 Likes

Varun Beverages in talks with partner PepsiCo for its foray into hard drinks. This is being mooted for Indian markets and help to add more revenue streams.

6 Likes

Q4CY25 results may give some more clarity on numbers by the management, related to the African beer market they will cater to, and related stuff, basically a more deep dive into this decision by the management.

This video gives a decent breakdown,

4 Likes

2 Likes

“sending shares up 4.9% in afternoon trade.” Eh..Is it ? It actually went down and media reports it went up. I wonder, wjat spoofed the market as shares went down 3.5% when everything else went up. Is it lower profit and EPS on Q on Q ? Yet to look at the results closely.

1 Like

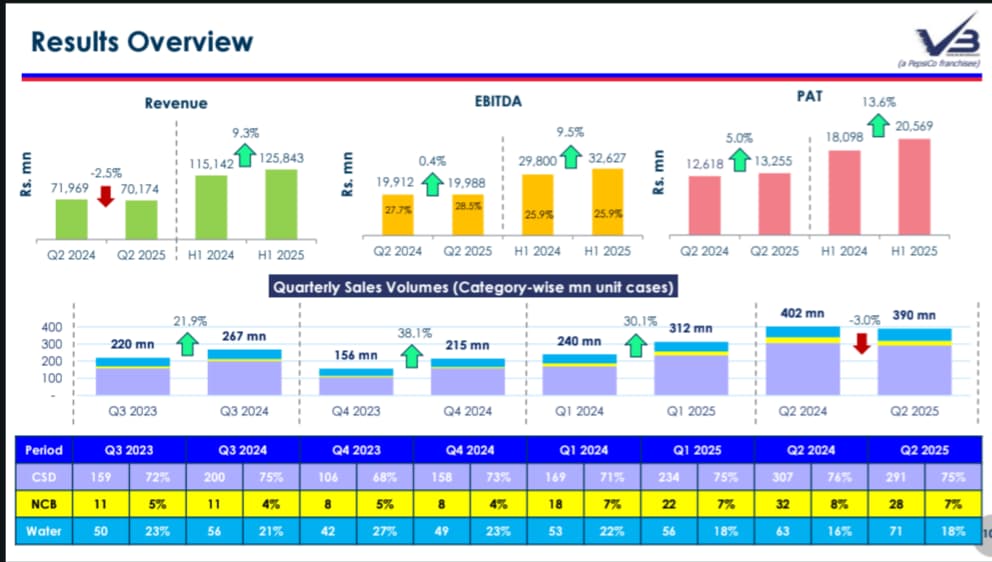

Because of the Margins and Inline Volume Growth in international business, which was believed to do well, the domestic volume growth outperformed the estimates