Below is my portfolio and would expect your comments or advice on it. I believe both in value investing and growth investing so you many find some stocks that are very expensive.

Good portfolio. Can you write a few lines on each stock and your rationale for buying / holding? I am not sure what kind of response you are a looking for? Just looking at a list of stocks tells me nothing. It has to be tied with your experience in the markets, risk appetite, ability to withstand 30-40% drawdowns etc.

I have been investing in market , But my strategy earlier had been to buy when i see value in a stock and sell it when i used to make profit of 30- 35% . However due to this my holding periods was short and was not able to have compounding effect of my portfolio and if i made a mistake that would wipe substantial part of the profit. Hence after lot of research and studying my thought process if to have a concentrated portfolio of 12- 15 stocks and hold it for a long time and see the compounding effect kick in. I am 65% invested in 35% in cash. I believe some of the stocks in portfolio is slightly overvalued and would invest 35% remaining cash if those shares correct. Below is the rational or thought process for each of these stocks.

Agro Tech- FMCG- MCAP 1500 Cr - This company is focused on created brands or products that other FMCG dont specialize it and have a sizeable market of 500 crores and 20% Profit margin, In span of 6-8 years if they are able to have 6-7 brand it could have a sales of 4000- 5000 and profit of 500- 600cr and could have a market cap of 8000 to 10000 cr . So a 5- 6 bagger

Balmer Lawrie- PSU Mini Ratna- This is more on value investing . I feel it is highly undervalued and its logistics business has potential for growth and they are expanding this business. So i feel eventually it will be re rated

E- Clerx - KPO or BPO. - It is the leading listed KPO player. It has profit margin of close to 30% which is significant.It has been continuously growing both organically and inorganically . Its also debt free and had good management.

Escorts- This i feel is undervalued . However for it to get better valuation it needs to improve its profit margin and i feel management is putting effort in right direction and it will take some time to show results

Gruh,: I guess everybody aware of HFCs growth potential. Even though it is overvalued i am looking to hold it for long time.

IPCA Lab- This more of contrarian buy. I find it hard to analyze or differentiate which pharma company has great competitive advantage . So i have bought a contrarian buy in this sector due to its FDA issues.

Persistent System:I feel one the Mid Cap company will grow in the new era of SMAC. My bet is on persistent system as i feel they are well prepared for it and good management

Poly Medicure: I feel just like Pharma sector the medical devices had great scope in future and india will have a major playe. So based on the scope of the sector- More of top down approach i have selected poly medicure over opto circuit.

Supreme industry- This is more of integrity of management and compounding stock.

TV Today. Cheap media stock

Va Tech Wabag- Water - Leader in water treatment and sector has growth potential

How do you feel about the promoter/management of Escorts and Poly Medicure? Are they relatively honest?

I too bought lot of IPCA Labs at around 700 levels average price. Would buy again if it comes to 500-600 levels.

Rationale behind Agro tech food looks good.

Nikhil Nanda seems to have a vision of improving profitability margin of escorts and not of improving sales. Also the 4 CEOs of different business segment have credible back ground. Some of the steps taken are to reduce debt , VRS for employees. He is also tying to do tie ups with other companies like Porsche and other measure to increase export for better profitability. I guess if he succeeds in his vision it will be a multibagger. This company is trading less than discount to book value and has a turnover of more than 5000 cr . However its market cap is just 1400 to 1500 crores. So the only reason i can think of it trading at such valuations is profit margin. Hopefully the measure taken would help achieving it. The promoter holding has been steady and debt has been reducing this shows promoters genuine interest.

As far as poly medicure i do not have much information on credibility of management. However the forward looking statements of management has been correct over the years. I am more bullish on the sector . Just like pharma india also will have low cost medical devices company. This company as per recent news will raise additional capital or debt for manufacturing in India . It is currently highly over valued so i plan to add more if there is a correction.

Yes i plan to add more of IPCA if it comes down. However i believe all the bad news are factored in and may not come below 600. But market is full of surprises.

Though it was a cash bargain but it looks like the cash is being deployed progressively in buying businesses and company

is positioing itself as integrated solar play. What is your reasoning for buying the stocks as there is no positive traction w.r.t. business / profits and stock remain subdued.

I was looking at solar sector specially . I agree this will not have immediate upside potential. It will take sometime for it to grow its solar business as you rightly .They are making their investments in this currently like investment in US, The second reason was the promoter execution capability. The ability to grow UPS business from the promoter and sell it off at the right price shows capital allocation and execution capability. However you would need lots of patience to see upside in this stock,

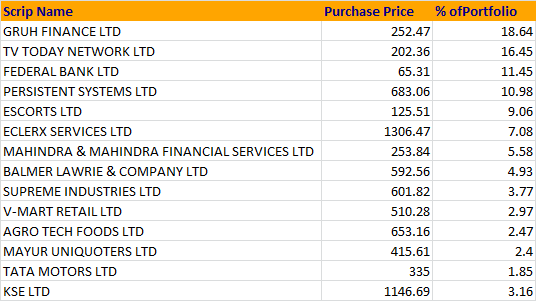

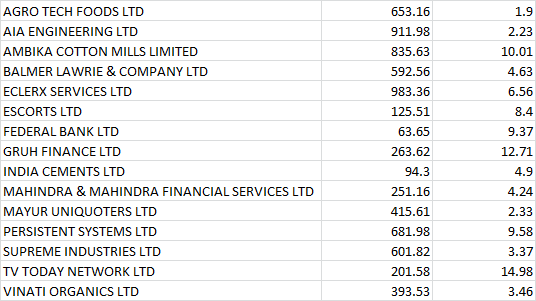

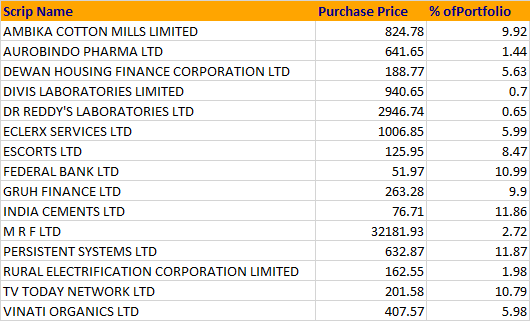

Can anyone advise me on my stock picks. I am planning to hold the below for the next 5 years unless any of them goes below 8% of purchase price. Given below are the stocks with their avg. purchase price:

Apart from swelect, Ujaas also is a good player in solar sector. Opportunity size in solar is very large but most large order are being captured by large players viz. Tata power, india bull, Renew power etc. Ujaas is focusing on solar park (150 mw) , SOLAR power generation (15 mw) and EPC orders and getting good traction in business as well as markets. Once it crosses 1000 crore MCAP, it may come on the radar of institution. Management is also proactively sharing their perspective in concalls. This year they r likely to install 80 MW so a top line of 500 cr and bottotme line of 50 looks likely.

I think equally bullish about swelect but they are still setting up their manufacturing capacity and still to get significant orders. But once they get going , growth would come conformably. Though I am not sure why orders r not coming to swelect way? Has the DCR ( Domestic content requirement) withdrawn by MNRE/ SECI due to adverse WTO judgement and loss of appeal. Not sure if still DCR projects being floated by gov? Share if you have any idea?

I did look at Ujaas but somehow gave it pass as it did not meet one of my criteria in my checklist.I have not looked at DCR issue i remember reading it when i was doing the research on solar industry. I felt its hard to pick a winner in this sector as there are other large players and difficult to predict who will survive.