Company Introduction

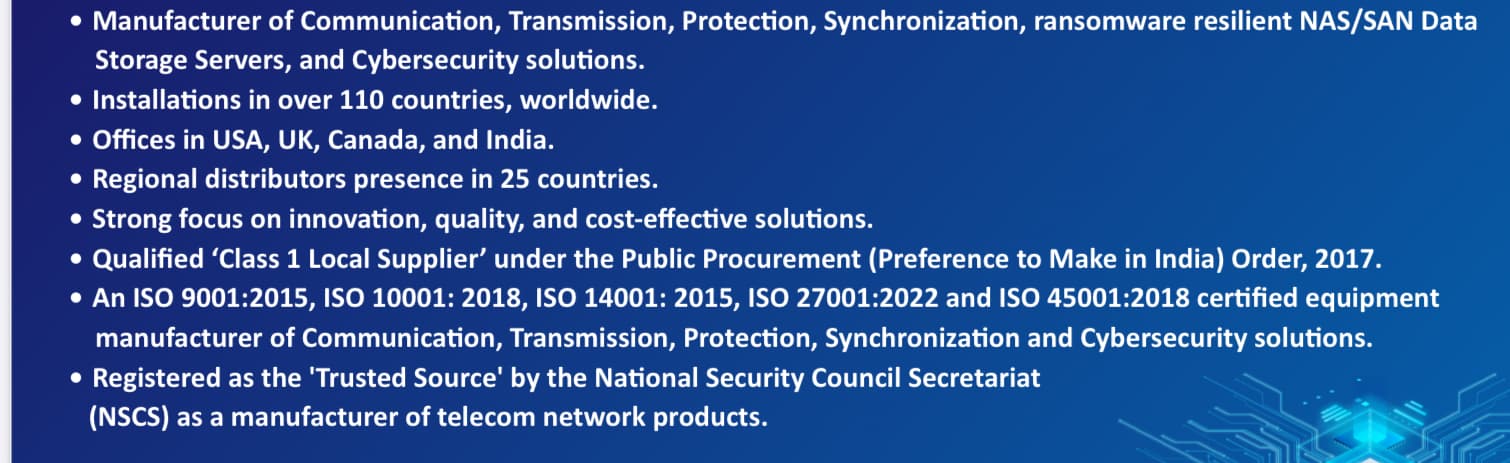

Valiant Communications Limited, founded in 1994 and headquartered in New Delhi, India, is a publicly listed enterprise specializing in advanced communication technologies. The company is certified under ISO 9001:2015, ISO 14001:2015, and ISO 27001:2022, The company has earned global recognition with its devices being installed in more than 100 countries. Its early product portfolio included Digital Pair Gain Systems, PCM Multiplexers, and Optical Line Terminating Equipment, laying the foundation for its evolution into a global provider of telecom transmission, synchronization, and cybersecurity solutions. Despite operating with a lean workforce of approximately 75 employees, Valiant has established a strong reputation for delivering mission-critical communication systems to diverse industries including power utilities, oil and gas, railways, airports, defense, BFSI, and government institutions.

Business Overview

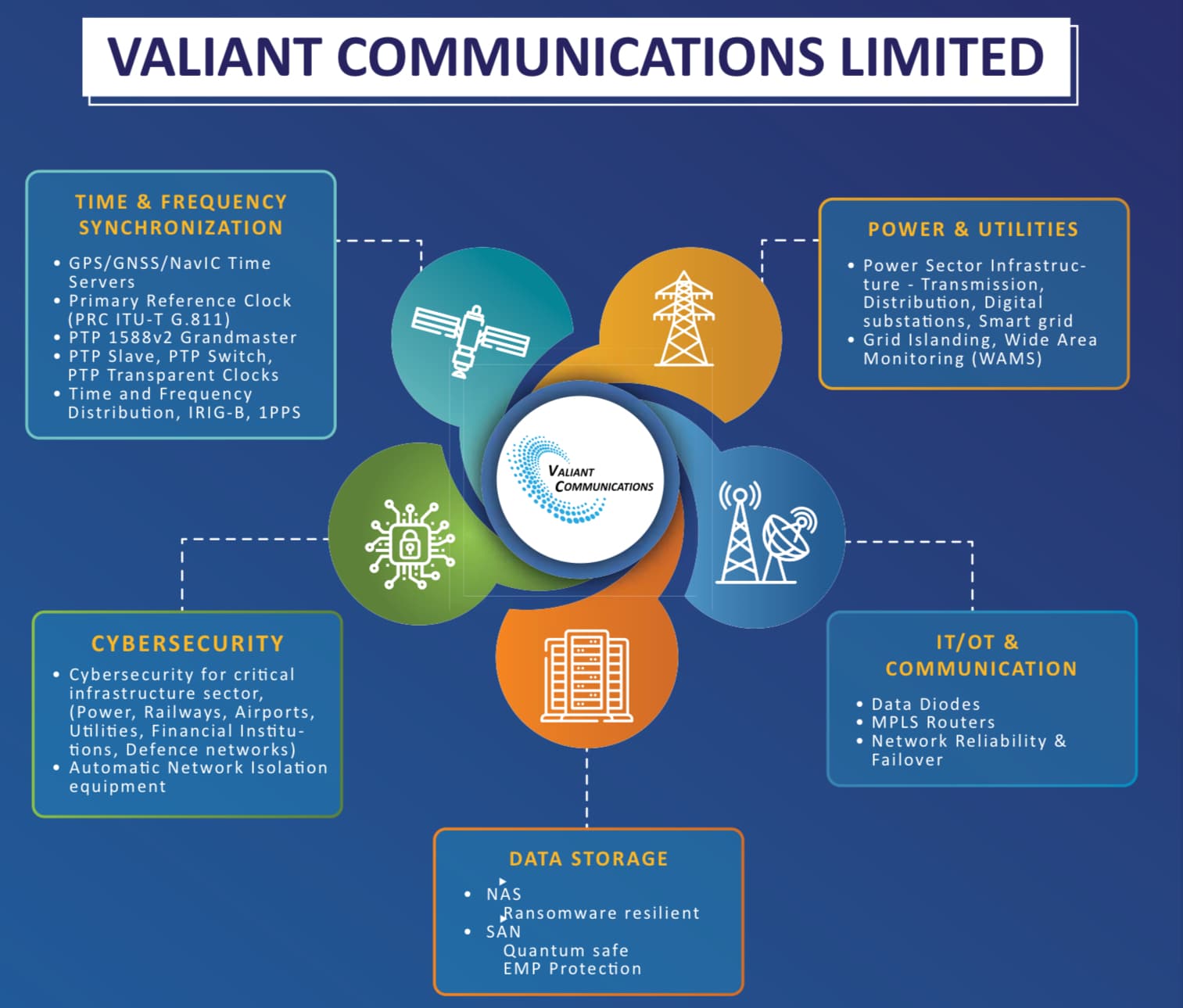

Valiant Communications operates as a technology-driven enterprise focused on communication and transmission solutions for critical infrastructure sectors. Its product portfolio encompasses IP/MPLS routers, SDH/SONET and PDH multiplexers, IP multiplexers, and ruggedized industrial switches, alongside teleprotection systems, distance and differential protection devices, and advanced cybersecurity solutions. Synchronization technologies form a core part of its offerings, including GPS/GNSS-based systems, Phasor Measurement Units (PMUs), and Phasor Data Concentrators (PDCs). The company provides tailored solutions for power generation, transmission, distribution, Smart Grid, and renewable energy networks, while also serving oil and gas pipelines, railway and metro systems, and airport communication networks. Designed for reliability, redundancy, and secure data transmission, Valiant’s products address the growing need for resilient communication in mission-critical environments. Its cybersecurity solutions further strengthen industrial and utility networks against evolving threats. By integrating transmission, synchronization, and protection technologies, Valiant positions itself as a one-stop provider of communication infrastructure, continuously innovating with offerings such as parallel redundancy protocol switches and automatic Ethernet failover systems. The company’s business strategy emphasizes serving high-value sectors where reliability and security are paramount, ensuring sustainable growth and global competitiveness.

The company has a focus on providing security hardened solutions across sectors.

Its main bread-earner at the moment is power and utilities where it gets about 70% of its revenues but it also has various devices aimed at other sectors as well .Its recent offerings include..

- Grid islanding Solutions which allow isolation of a section of electrical grid to operate separately and self sustain .This isolation can be intentional or unintentional like a fault situation or cyber attack .This solutions are important specially where renewable energy grids are to be connected with the main electrical grid as it allows the operators to handle all the uncertainties like intermittent power,phase and frequency shift .

- SAN and NAS data storage solutions which are quantum-safe(authentication and encryption) and EMP pulse protected,Network Isolation equipments and vaulted data storage through data diodes. All these are aimed at protecting Critical Information infrastructure which can become more important going forward .

- It has added NAVIC compatibility alongside GPS to all of its synchronisation equipments as GPS is a system provided by US military and has been jammed in the past in the hour of need during Kargil war . They have also added GPS anti jamming and anti spoofing features . Since these synchronisation equipments are critical for sectors like banking, defence and other critical infra , these actually provide a sovereign option to the nation .

- They are testing their MPLS routers designed for defence and utility networks and has already received orders for these .

All the above things are going to be useful as there are mot many Indian companies who make these kind of cyber security focused devices .

In 2022, Valiant Communications received approval from the Grid Controller of India (formerly POSOCO) for its cybersecurity equipment designed for deployment in India’s national power grid network. This approval was part of a pilot project to strengthen grid security against cyber threats .Its not that no other company had approvals for these devices but all of those were foreign multinationals like siemens ,abb etc. Two years down the line this has translated into orders from various state electricity boards that has lifted the companies revenues to a different orbit. One can hope that with focus on sovereign self dependence ,the devices and solutions mentioned above will also generate good revenues in near future .

However, VCL has about 28% of sales from international markets as well and their client list is impressive. Apart from those in the picture above, there are various state police / power/ transport departments from countries like Italy,Chile,Bulgaria,Denmark,France ,USA etc. has appeared in past years.They are gaining traction in latin American markets recently as per their updates .

They also have a tie up with Tejas networks whereby Tejas uses Valiant products for projects they win (not all projects they win) .The good thing about valiant is that for a small company, the provide regular business updates and informative power-points during quarterly results .One can check the below link for recent updates…

https://www.valiantcom.com/whats_new.html

Results and Financials

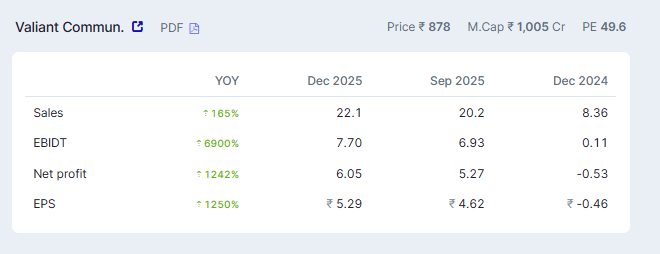

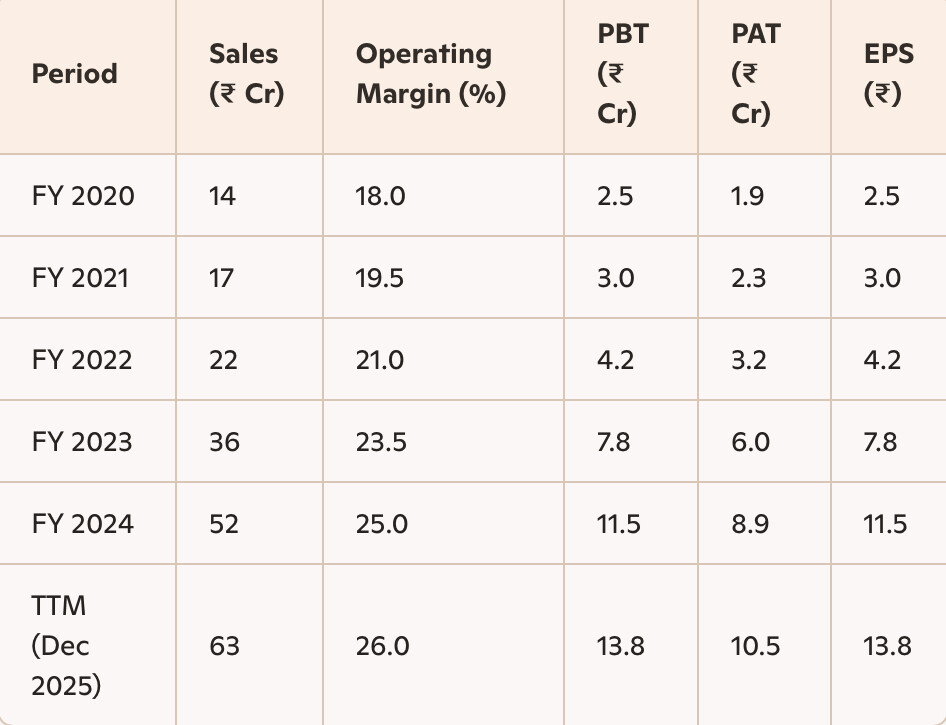

The consolidated results for past few years ..

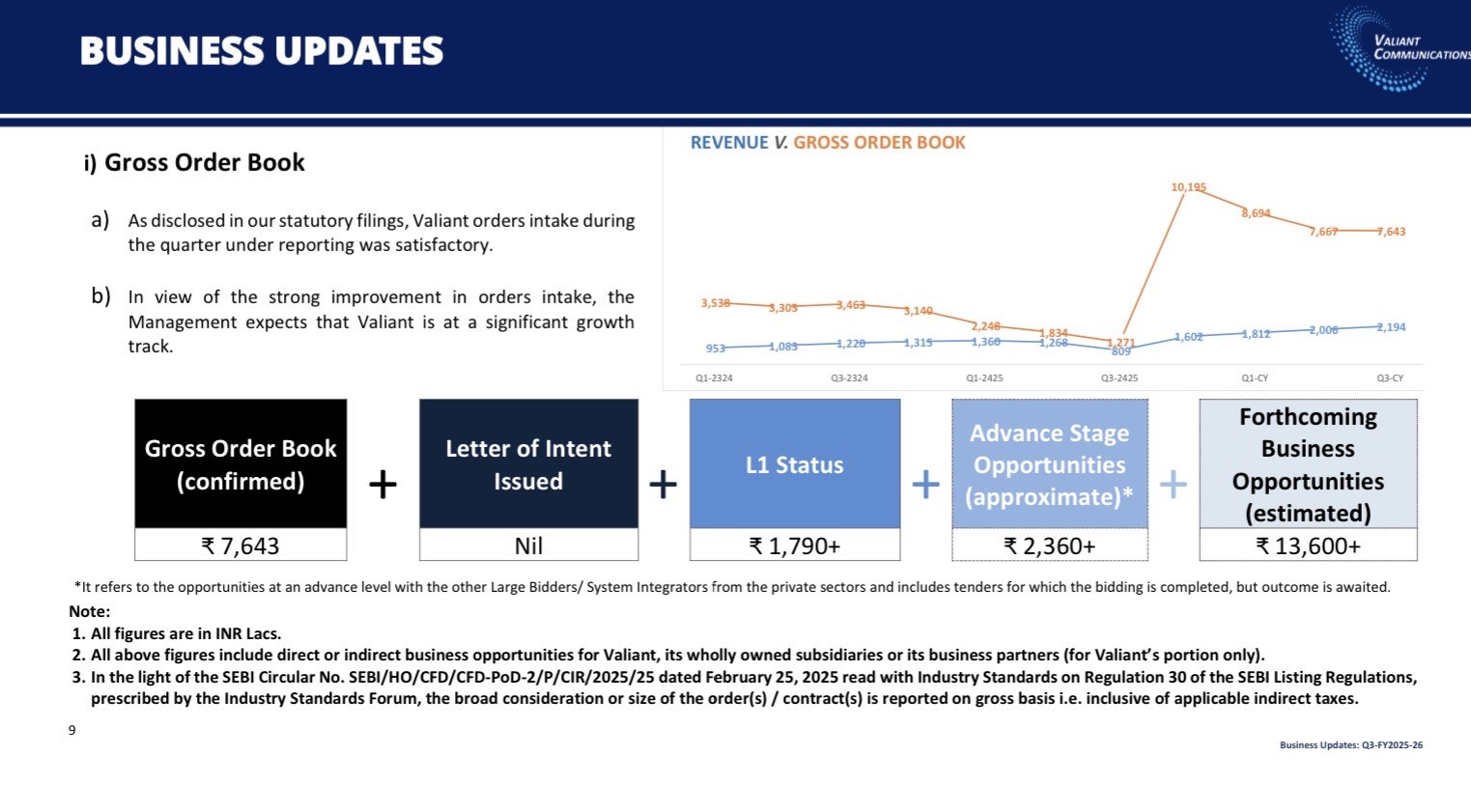

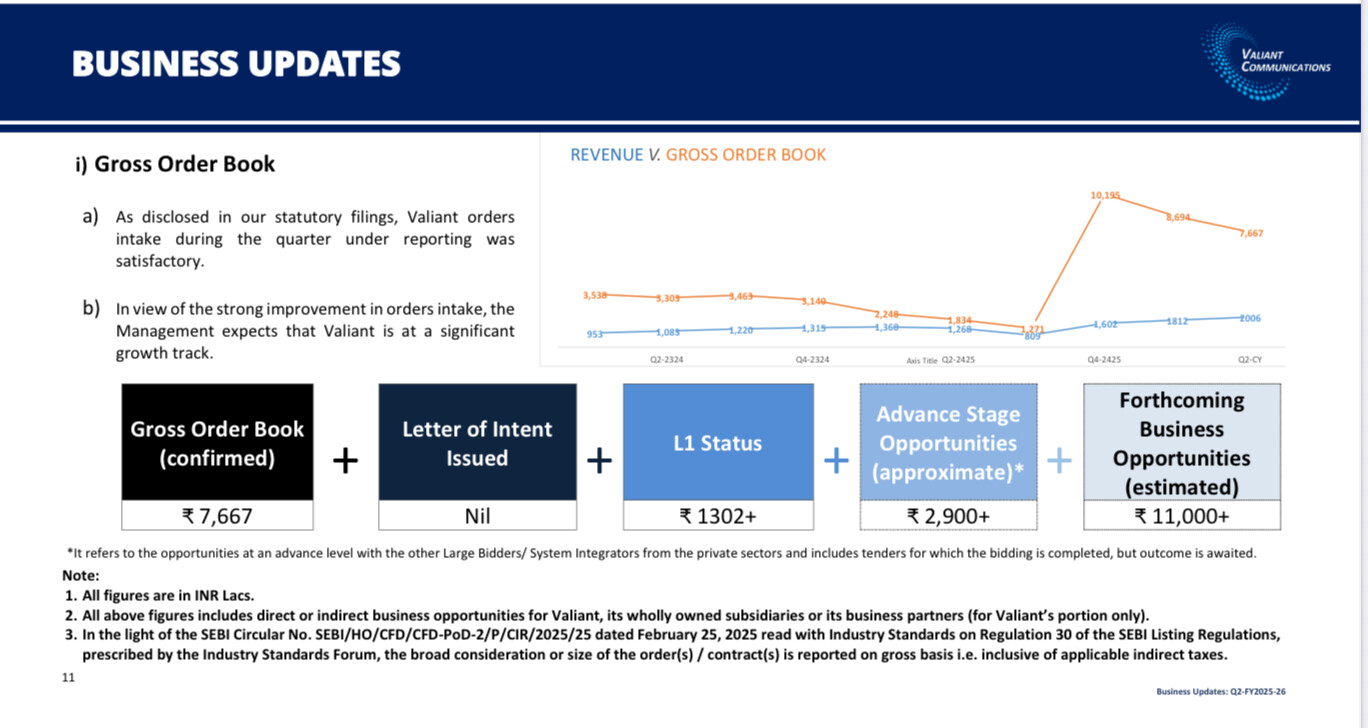

The company got a few large orders from Gesco and Tejas a few quarters ago which lifted the company revenue to 40 crores per year to 80crore year range . As per their latest update in after Q2fy26 they still have almost 10 months worth of orders at the current rate .

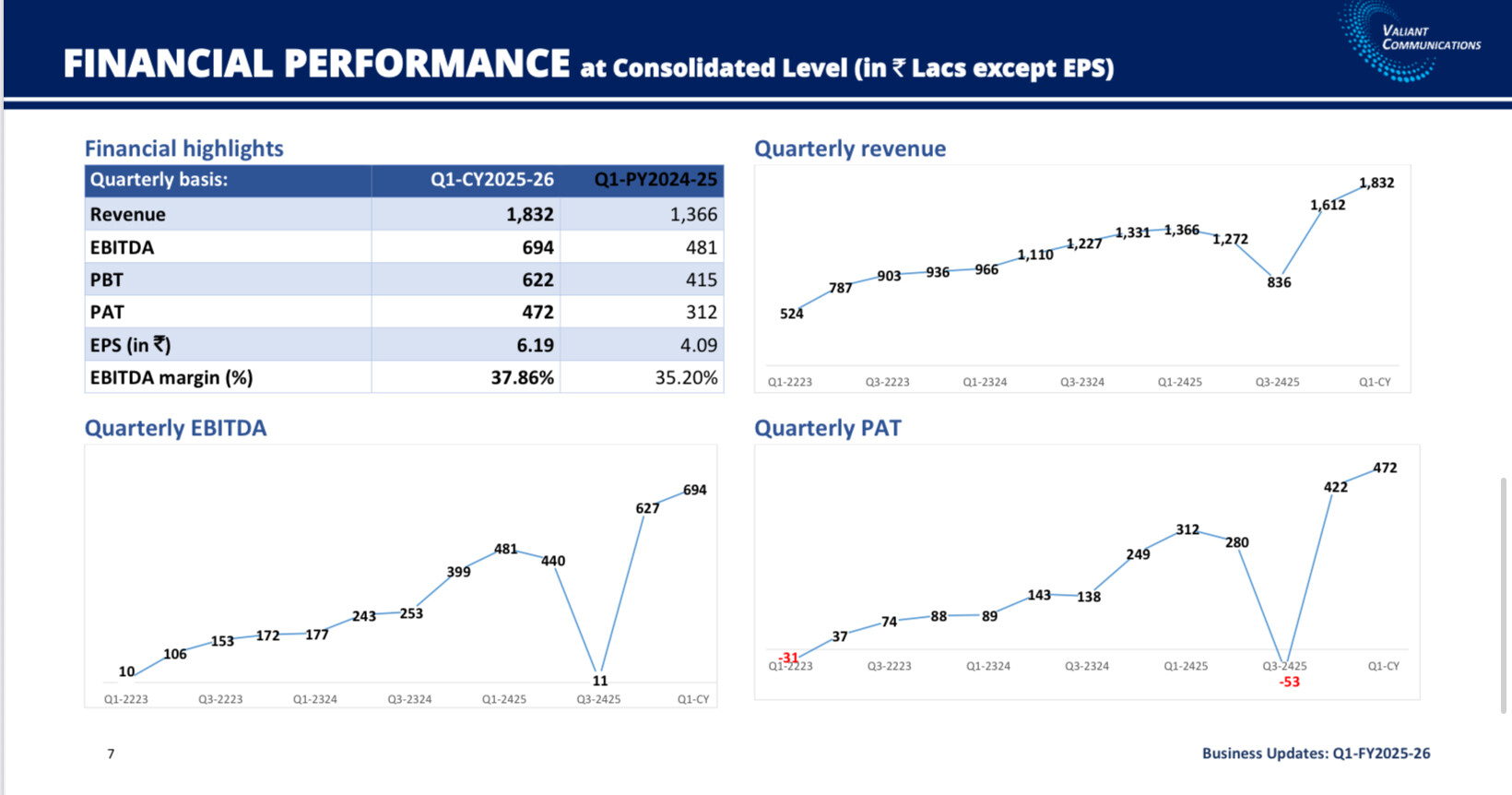

However its small company and it can give negative surprise sometimes as there is lumpiness in QoQ results.Check what happened in Q3 Fy 25.

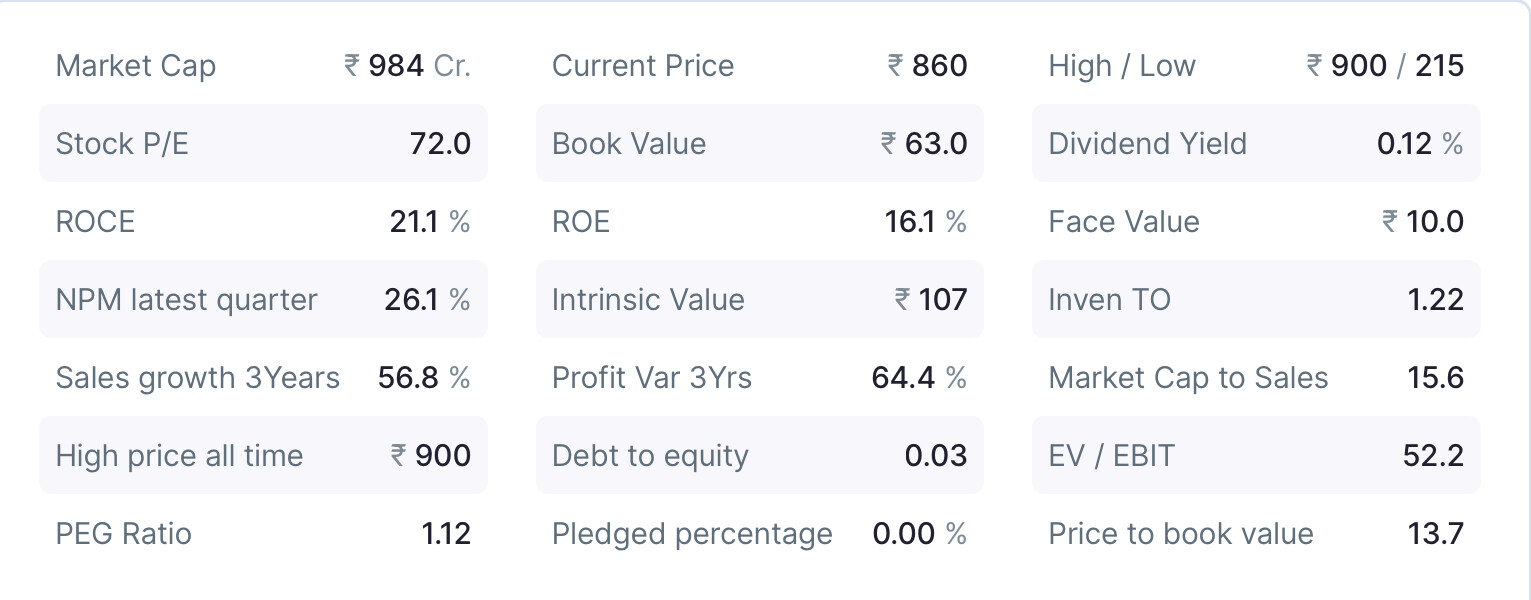

Currently the stock is not exactly cheap as even assuming 16 rupee eps at the end of the year , its trading at 55 PE ,but it seems to be able to hold strong during marketwide panics recently and has not gone anywhere near the 200 DMA even after rising 3x since the month of March 2025 .

The company has unimpressive working capital days and duly has done preferential issue twice in past 3 years . Some well known investors like Shankar sharma bought more than 2% in. 2023 at around 200 rupees ( adjusted for the bonus in 2025) and again bought warrants at 768 in 2025. A couple of funds like Niveshay and Rajiv Khanna too bought warrants at 768 .

I am not from commerce background and hence won’t try to go deep into various metrics .Instead, I will just say why I had spotted it back in mid 2023 .

My Angle

I came across a post in twitter that this company of 250 crore mcap has gotten an approval that will allow it to bag all the grid security related orders ,because of make in India drive and central push on grid security. While this post was not fully correct,I looked at the company and to me it looked like a very good bet because ..

- For a smallish company ,it made complex electronic equipments and had proven itself by being able to sell it to european and american local government departments .

- It had a handhold in a difficult sector where ABB,Siemens etc.ruled the roost.Who knows, if make in India actually takes off ..

- It gave good PPT with enough info each quarter and sometimes mid quarter too.So it was easy to track even though they did not do concalls( they don’t even now)

2 years have passed and that 2nd point has worked out and should continue to do so .So I am still bullish on it but have taken out the initial capital as its already up about 4x from my buy price and I want to bet on new horses as well . The remaining portion is still 4.5% of my portfolio.

Risks:

Ultimately its a small company and the stock is somewhat illiquid.This past year it was mostly in ASM of one kind or another and spent a significant portion of time being hobbled when it was traded over auctions.

Business wise, they sell small amounts to many customers world over and does not seem to have concentration risks as such ,but the present orderbook is somewhat concentrated as GESCO gave large orders .They have done a preferential allotment ,so they should not be stretched for want of capital soon but cashflow remains a thing to look at .

In Summary,Valiant seems like a good small company that has shown execution ability and innovation ,operates in a sector where not many Indian listed companies are present and have some tailwinds due to India’s recent focus on sovereign solutions for its critical infra .Its still below the thousand crore marketcap and hence remains a good bet for long term smallcap investors.I do not have anything more to add just now but I hope VP community will take the discussion forward .