Some serious deals happening including 3deals worth more than 700cr each!

http://www.moneycontrol.com/stocks/marketstats/blockdeals/view_deals.php?sc_did=VS&classic=true

Some serious deals happening including 3deals worth more than 700cr each!

http://www.moneycontrol.com/stocks/marketstats/blockdeals/view_deals.php?sc_did=VS&classic=true

If u check vakrangee’s recent announcement they have hired ex VP of HDFC

bank and they have issued investment profile

Also there is nothing from SEBI currently on the issue which is highlighted

by Mumbai mirror

In 2 years it has risen so much without any correction or dips so this

negative news which is baseless dragging it down

If u see in the past vakrangee had hit 2 Lower circuits from 170 to mere

80-90 levels n then gained back so strongly

I think it’s just change of hands

Weaker hands exiting and there is a higher jobbing going on by jobbers

It’s a debt free co with cash reserves and has gud independent directors

and tie ups with all leading cos for banking , insurance, couriers & e-mail

governance too

Correction was not coming so this negative dragged it down way to fast

I think all is ok and u just need to stay invested

May be you are right but more than 900 crores transaction in a day with Abt 1.95 cr shares each two deals have been done by some big investors.They definitely r not weak hands.Its time to dig more and be cautious.

BSE announcement -

CEO and CTO appointment.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/c60b2445-eab1-4a94-b7ba-baecb2b588b9.pdf

Transparency in cash deployment - http://www.bseindia.com/xml-data/corpfiling/AttachLive/19e818e9-5ade-4c0d-b6ec-e788619f36d9.pdf

I think today’s correction has following surprises -

(1) High volume change hands (more than 2.5 cr shares)

(2) at this high volume - delivery volume is more than 50%

(3) Large deals

I think looking at Strong growth (Network effect of Vakrangee Kendras) and appointment of telented and experienced people, future is brighter. Hope, this is good opportunity to add more !!

Disc - Invested since 2 years

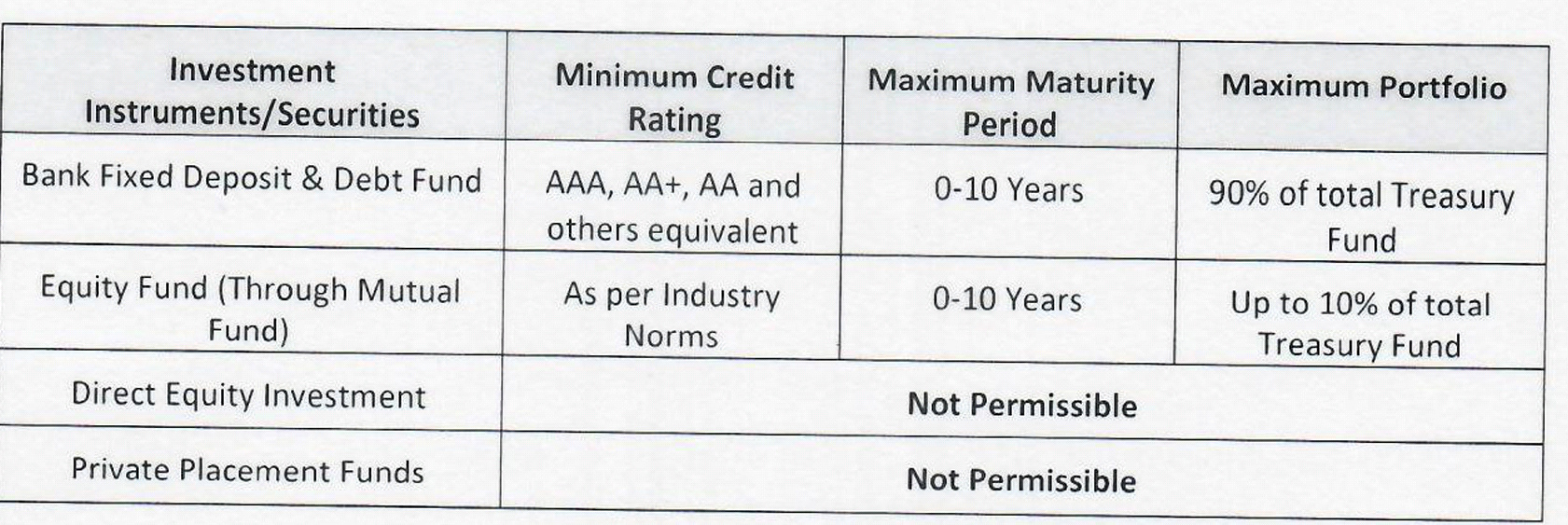

As per their treasury policy no direct equity investment is permitted. So how to explain PC Jeweller investment?

Its is through their subsidiary vakrangee holdings

Another 20% cut. 40 % lost in two days… there is definitely some problem which smart fishes are smelling and we common investors are missing.

Any senior members lease share if having any news.

Disc : Not invested but wishing to enter in, but feeling scared to catch a falling knife.

This is a simple but an interesting table ! but after 43% correction, the valuation has been brought down to 51PE from 71PE, which appears to be still over valued.

In my opinion, any decision of under or over value needs to be taken post investigations. The details published by print media are based on hard exchange data and should not be rubbished.The management statement has neither given any clarification nor any comfort.There are huge deals, which indicates large investors are off loading shares with 20% down circuit day after day.Keeping past frauds in an IT company in view, nothing is impossible .

Let us not try to catch a falling knife.Experienced boarders may pl. share their view/opinion.

From last many years I fail to understand profitability of this Vakrangee Business. They say per BC branch they make 10 lakh Revenue annually, out of which 3 lakh comes to Vakrangee. Even if I assume Rs 10 charge per transactions in these remote rural branch, they need 300 transactions per day to make 10 lakh. Now BLS just got its contract cancelled with Punjab govt, because there avg transaction across all branch was just 8 per day. Magically Vakrangee is able to 30-50 times more transactions!

Also Rs 10 charge per transaction is quite high. If the remote villagers hold a saving account with Rs 1000 avg balance. Banks pay 4% interest and keep 4% to themselves. At this rate Bank makes Rs 15 per month on these accounts. Even if the account holder does one transaction in a month business becomes uneconomical at Rs 10 per transaction.

Vakrangee’s performance defy all logic to me, but may be I am wrong and investors are right.

Tracking Vakrangee from 10 years now, never invested a penny in it and nor will!

Hope you remember ONLY the wire has reported “Aadhar details are available for Rs.500”. Which raised eyebrows and ever since “the ever leaking Aadhar details” are taken little seriously. So, we can’t rubbish that Mumbai mirror was the only one to report (could be a rumor as well), but we can’t directly deny that without a conclusive report/clarification from Vakrangee. Apart from this, I have few doubts. Requesting boarders to pls help me understand.

I have reviewed this company few times over the past 10 years and every time there was some or the other thing that put me off. In most cases it was poor cashflow or growing debt or my inability to figure out exactly how does the company earns revenue or exact nature of its expenses. the only reason I kept on looking at this company every few years or so is because of its growing market cap. Never bought a single share of this company.

Here is the latest one. company claims that its Vakrangee Kendra (VK) are major source of revenues. These kendras are value-added cyber cafes cum ATM machines where customers are provided with hand holding services to use various banking, e-governance and other financial services. To me it sounds like these Kendras are small outlets that it set up to deliver its e-governance services prior to 2013 and later they added white label ATM machines and now using these centers as distribution channel for all kinds of financial products and other consumer services. The business model looks good but that’s where the story ends. When I tried to get details I got stumped. Since these Kendras are the main assets of the company, I looked at past 8 annual reports to get an annual count of these VKs but here is what I found

2013 - Company proposed to set up retail outlets

2014 - 3400 Vakrangee Marts (assuming these are called Kendra now) operational.

2015 - No mention of actual number of Kendra. If anyone as idea, please post a screenshot.

2016 - 21,000 Kendra

2017 - 35,000 Kendra

9M 2018 45000 Kendra

These numbers are approximate numbers that I can recall. AR reports are full of grand vision and mission statements as if company is trying to build a reputation based on what it is going to do instead of what it has done. There is no mention of operating matrices of a kendra (cost to set up, revenue share with franchisee, cost to operate etc). Even investor presentations are full of fluff and lacks specifics.

Company says they serve all PIN codes but they are present in only 17 states and they are not there in 4 southern states.

At peak market cap of 50,000 Cr just a few days ago, each of this kendra is worth 1 Cr each. That’s just too much. Anyone can set up this Kendra at fraction of this value. Moreover, staggering growth of these Kendra from 3400 in 2014 to 44,000 today is just unbelievable.

For any company, first thing I try to find out is the sources of revenue and risk to revenue. I could not get enough details on exactly how does this company earns revenue. Does the customers pay them a service fee? Probably not. Does the service provider pay them a commission? Most likely. What % of that commission does the franchisee keep? But there was not much details about who are biggest clients, how much revenue company is generating from them etc? They provide all kinds of services from banking, telecom, goverment programs etc. I was trying to get a break up who paid Vakrangee and how much.

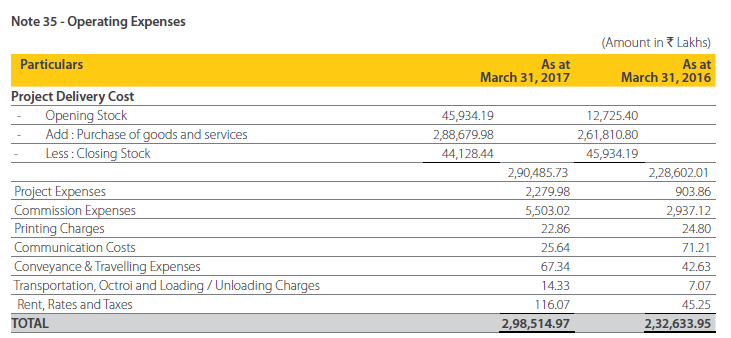

Same with major expenses. Here is a major expense from the ir AR.

I have no idea what is this Project Delivery Cost and what goods and services they are purchasing? Is this payment made to franchisers? may be, but that’s just my guess. There were no details available in any of the annual reports.

Overall, I got more questions than answers and that’s usually when I let go a company no matter how interesting it appears to be.

Another point at 5800 cr Revenue and 3 lakh per branch. They need to have 2 lakh branch or kendra already. They only had 35000 till last year, magic continues.

These Vakrangee kendras sound so much like the Sanwaria kiranas (and perhaps 8K Miles’s customers) from my research on the latter. I like how the possible cooking of books was speculated so beautifully in this post on VP.

can the share holders on this forum seek a con call from the management to post questions and seek some answers?

There is some more confusions from the numbers…

Segment assets… Why is most Rs 1539 cr unallocated?

Generally this number is very small. But when compared to total assets, it is 57.7% of the same.

Employee benefit cost of Rs 18 cr (quarterly) seems too low for the company of this size…

what happend to this stock? anyone having idea?

Jus a needed correction as it was not coming from last 2 years

42% correction of price in a week is not normal correction…something mr market knows which we dont

no no i m asking about SEBI investigation???