Vadilal is an Indian ice cream and flavoured milk manufacturer

It has been active for about 115 years.

27 Awards Over 4 Consecutive Years At “The Great Indian Ice Cream Contest”

Voted As India’s Most Trusted Brand In The Ice Cream Category By Trust Research Advisory Board.

Vadilal has so many divisions and product lines under its roof, dairy products like ghee, milkshakes are also exclusively produced

Has opened a retail store “Melt in” which has huge franchising opportunities

The business is extremely seasonal with maximum sales happening during the summer months.

The company is increasing its thrust into the global markets especially US. The company acquired Krishna Krupa Corporation, an Illinois (USA) based ice cream parlour to better understand the ice cream parlour business in the US.

INDUSTRY ANALYSIS

India is the largest producer of milk with about 1/5th of the total production providing ample raw materials for the company

The ice cream market in India is forecasted to exhibit a CAGR of 17.03% during 2016-2021.

The total organised Indian ice cream market is estimated at approx 6000 crores. Though overall organised & unorganised ice markets are estimated near about 10,000 crore

Compared to western countries, per capita ice cream consumption in India is low

The rise in disposable income and the “eating out” culture in a ramp will give a steep increase to demand for desserts, especially ice cream.

There is huge scope for ice cream market expansion and penetration with an innovative product mix to attract India with all class & mass of Consumers.

The global frozen food market is expected to grow from $167.34 billion in 2020 to $174.4 billion in 2021 at a compound annual growth rate (CAGR) of 4.2%.

The global ice cream market stood at a value of $62.3 billion in 2020. The market is further anticipated to grow in the forecast period of 2021-2026 at a CAGR of 7.5% to reach $96.1 billion by 2026.

COMPANY DEVELOPMENTS

Vadilal to consolidate leadership brought in various measures including rebranding the logo, slogan etc. Brought in many different variants of ice cream

The company took on serious marketing campaigns to attract the customer base

The brand’s existing variants like Gourmet, Badabite, Flingo Jumbo Ice cream Cups and Ice trooper continue to show substantial movement in the market.

Vadilal is growing, the brand spread its wings wide in South India, and enjoyed widespread acceptance. Vadilal ice creams and frozen desserts were introduced for the 1st time in Tamil Nadu.

Has started exclusive parlours in three formats: Scoop Shop, Hangout & Express along with the newly started Melt in

Currently the brand’s ice cream production facilities are located at Pundhra in Gandhinagar district, Gujarat and the other at Bareilly in Uttar Pradesh.

Possesses the best infrastructure in the market from machinery to networks

Apart from ice creams, Vadilal is also vigorously expanding in categories which offer value chain benefits and show a strong potential to grow.

The international competition has encouraged Vadilal to grow and improve. It now has a premium section with Melt-in to compete with the international brands

The company had launched Waah! Vadilal campaign and took to extreme advertising to gain market share

Vadilal has presence in over 45 countries including the countries in North and South America, Europe including the UK, the Middle East, South East Asia and Australasia. Hence, strategy for every territory has been planned on the basis of respective country’s market demands and thorough research.

VADILAL FOREX in its 25th year of services – is Numero Uno in Gujarat having more than 450 Corporates associated with it

RISKS

High Competition from foreign brands.

Change in consumer view after the pandemic

Online selling which can bring in more revenue and reduce administrative expenses is not a strength for the company.

There are certain concerns like infrastructure and rising input costs.

The major raw materials for manufacturing of ice-cream are SMP (skimmed milk powder), milk, cream and nuts, which the company procures from local dairies near its manufacturing units. It also procures palm oil for manufacturing frozen dessert. There have been significant fluctuations in prices of key raw materials in the past and is possible in the future as well which can cause significant changes in margins.

Vadilal was promoted by Vadilal Gandhi who started ice-cream business in 1907. Currently, the operations are managed by the third and fourth generations of the family i.e. Rajesh Gandhi, Managing Director, Devanshu Gandhi, Managing Director and Mr. Kalpit Gandhi, Director and CFO (Son of Rajesh Gandhi). While Rajesh Gandhi looks after the overall operations of the company, Devanshu Gandhi looks after the sales, marketing and distribution functions. Apart from the finance function, Kalpit Gandhi looks after the plant operations on day to day basis.

The promoters own nearly 65% of the equity of the company.

During FY19, Vadilal’s two sets of promoters made various allegations and counter allegations on each other

Was primarily due to the fact that some personal expenses were treated as company expenses, Fund management and price dissemination.

One promoter director and the CFO have accused another promoter director of claiming personal expenses amounting to Rs. 25 Lakhs to Rs.33 Lakhs as official expenses between 2018-2019

The latter has accused the other director and his family of treating travelling expenses as office expenses between 2015-2019 which amounts to over Rs.23 Lakhs

Vadilal stated that the outcome of this event would not have any material impact on its financial statements.

Personally, have been consuming Vadilal’s ethnic frozen Gujarati uncooked vegetables for 8+ year now in the US. Their offerings back then were limited to few Indian flavored ice-creams, frozen vegetables, and some Gujarati dry snacks.

Vadilal started to put extra focus on US business about 4-5 years back and started offering ready-to-eat frozen Indian appetizers and entrees in frozen section of a desi grocery store.

Haldiram dominated ready-to-eat frozen section almost like a monopoly with numerous SKUs. Vadilal caught-up with Haldiram on SKUs and now offer equivalent (if not more) SKUs. Having more SKUs is very critical in this business since capturing the limited freezer space at grocery store is a competitive advantage. It becomes very difficult for a new entrant to not only have multiple SKUs but then offer them at a price that is good enough for grocery store to replace with older incumbent brands. I feel Vadilal might be serving more than 50+ SKUs including both ice-cream and frozen ready-to-eat segment.

As part of their new focused approach for US markets, Vadilal decided to do direct distribution to end customer (desi grocery store) instead of a distributor. This meant that there is no one in between except Vadilal, from manufacturing facility in suburbs of Ahmedabad to local grocery store in the US. Vadilal invested in having 3 warehouses in the US in New Jersey, Illinois, and California serving the entire country. This is the biggest competitive advantage for Vadilal which can be seen in its US margins. This business has tremendous operating leverage.

Vadilal hires third party logistics solution provider. A long haul reefer truck (refrigerated truck) leaves each warehouse every fixed day of the week to deliver goods that are ordered by the clients. All transportation costs are structured in such a way that the client pays for transportation. There are restrictions on minimum order that needs to be placed for Vadilal to load an order for delivery without any extra charges.

Vadilal started a new warehouse in Florida to serve south-eastern and south-central market. This should be very beneficial to turnaround on an order from southern market in 1-3 days as compared to 4-5 days from New Jersey warehouse.

Vadilal has almost monopoly in ice-cream business. There are 1 or 2 Pakistani players but their offerings are limited to Kulfi. Vadilal also caters to B2B in ice-cream segment by helping grocery store owners set-up ice-cream parlors within their grocery store.

This pic confirms that Vadilal’s US subsidiary acts as the distributor. I didn’t find any distributor name on back of Haldiram’s packs which leads me to believe that it has multiple distributors for each region of the country. I was able to confirm through some sources that Haldiram doesn’t distribute on its own in the US.

Disc: invested from lower levels and not a buy recommendation.

Excellent scuttlebut and appreciate efforts in sharing details and pics!

One thought, above does not seem a very difficult moat to break…also it seems because of better cold storage facilities and transports in US, setting up distribution there maybe easier unlike India…getting a place and setting up few warehouses and some long haul trucks i think other serious players can also do if they have that intent…

Also read somewhere, big players like Tatas are.now targetting US markets be it in food or jewellery…Tata smartfoodz , Titan etc. Would be interesting to see how they fare in capturing market share in US…

Also above views are only on the distribution moat of any incumbent in US and not specific to Vadilal…I am sure Vadilal has been doing transformative as evident from its stock movement and ongoing rerating…Not eligible for any advice…

Not true and not true. Seems like you haven’t worked in a distribution heavy or B2C industry. Distribution moats are difficult to break because they are investment led. For Indian companies targeting the Indian diaspora in the US, the market size is limited and it is just not worth developing their own distribution for. There are large existing distributors that companies would rather work with. Vadilal is one such large distributor and will have inherently large margins and ability to introduce newer products to the market.

Did anyone attend the AGM last week? Would request anyone who attended to please share some notes.

Good to know its not true. I have certainly not worked in such industry. There has been no need for me to work in such industry.

Exactly my point. In India distribution moats are very difficult to build (so far with rural issues and less digital) while in US, they maybe easier as making an investment is an easy thing to do than getting hands dirty. Buying warehouses, cold storage facilities, trucks etc. may take time but relatively easier to build as compared to India rural IMO (I may be wrong)

This is a good point that such investments by big business houses may not be worth it. If its worth it for them, its easy to build (of course with some time)

Agree! Till time the diaspora size is not worth addressing by bigger and better players, its really good for players like Vadilal. They may well develop real moats wround distribution as well as other areas as time progresses…

It’s on days like today where the lack of information sharing from the management in terms of the absence of concalls hurts. The share price seems to be correcting on regular profit booking, but it is difficult to muster the conviction to add with such little information available and build a large position.

Did anyone attend the AGM? I was logged in but also had work on the side so couldn’t pay full attention. There were discussions around the international and India businesses, and the management spoke of 15-20% volume growth on a consolidated basis. They spoke of how they have exhausted the penetration in the US, and future growth there will come from increasing the share of wallet through introduction of more frozen products.

Anyone else having any more information, please do share. Still trying to understand the longevity of the India business and it’s unit economics.

On account of various disputes between two brothers of the promoter group who were also on the Board of VIL and VEL, auditor had issued disclaimer of opinion on the accounts for FY19. However post that, the promoter directors have withdrawn their major counter claims against each other and the quarterly results of the company are also getting published within timelines. Further, both promoter brothers are re-appointed as Managing Directors of VIL. Also, an external law firm & CA firm were appointed by independent board members to verify the left out claims of the promoters. During FY21, the company had already received interim audit report on certain matters which exhibited no adverse observations or findings regarding the allegations related to operational and management matters. However, the auditor have maintained a qualified opinion due to pending receipt of the report over other allegations levelled by the promoter directors on each other over potential personal expenses that were claimed as business expenses. Further, a new allegation raised by a promoter director in FY21, in VEL, relating to matter involving operations and management issue wherein marketing expenses of advertisement amounting to Rs.38 crore paid by the company during the period FY16 to FY19 alleged to be done without following the due process of the company and which were also handed over to same independent CA firm and law firm to investigate, the report of the same is still pending.

Moreover, one of the promoter group (Virendra Gandhi and family) had filed a petition in FY18 against the Vadilal group in National Company Law Tribunal (NCLT, Ahmedabad Bench) for alleged oppression and mismanagement. The said matter is under preview of NCLT and no decision has been arrived yet. Resolution of the said allegation as well as NCLT matter will remain key rating monitorable.

Another dispute exists in Vadilal chemicals between the three brothers. Been going on since 2015. Case is in NCLT.

From the credit rating

Story looks interesting, but risks exist due to fighting between the promoters.

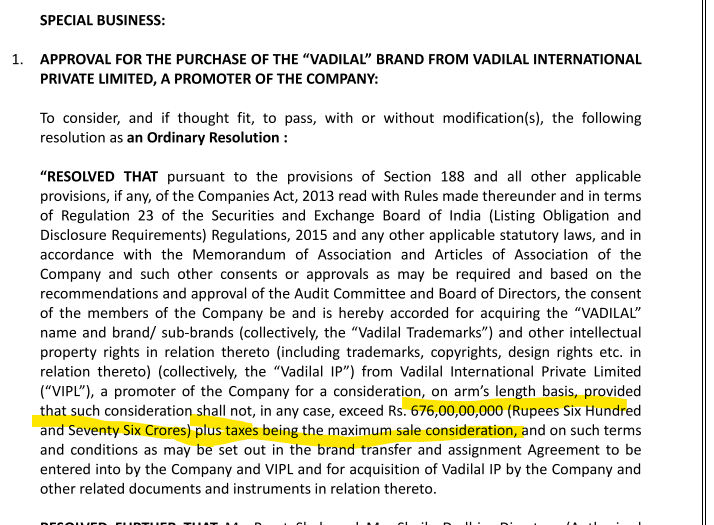

Big development!

Vadilal could become a special situation. If this goes through, it can pave the way for a PE acquisition of Vadilal Industries. If that happens, all the promotor disputes overhang will be out and the stock can relate to normal FMCG like multiples.

Page 14-15 of this report by @ankush12495 details this scenario. Very good resource.

Vadilal Industries buying the brand from Vadilal Promoter entity for 676cr. Also non core assets being sold by Vadilal for 40cr. Market cap of the entire company at 1900cr. So brand being valued at 35% of the current market cap. Any idea how the deal will be funded by Vadilal Ind - could be way of raising funds from PE investors imo. In that case could see a big valuation rerating.

Disclosure: Owned and interested

Wrote a twitter thread on Vadilal Industries this morning. Pasting the contents below:

I was very excited when I found a fast growing FMCG business trading at commodity valuations. Recently, it has also become a potential special situation. But even though it seems a no-brainer on first principles, there are many blind spots. The curious case of Vadilal Industries.

Vadilal is one of India’s oldest and largest ice-cream brands, with over 10% market share. The market is projected to grow at 15% CAGR and the share of organized players will increase. As India gets richer, ice cream will move from an indulgent dessert to a snacking essential.

They have the highest range of flavours among Indian ice-cream, catering to premium and mass market segments. Marketing expense to sales is the lowest in the category, showing the strength of the brand. They have also forayed into flavoured milk, frozen foods and Indian sweets

The most exciting part though is their international business which has grown at well over 25% every year for the last five years. Vadilal is the biggest Indian ice-cream brand in the US which has a large Indian diaspora. Other categories are fast gaining traction too.

They have a huge distribution moat in the US. They are one of only four national distributors of Indian ethnic products. This gives them better margins and bargaining power for shelf space, reinforcing the brand strength, and allows launch new products easily and efficiently.

They have also opened to their distribution to other Indian brands in non-competing categories. As more brands get added, Vadilal gains distribution revenue with minimal additional costs, leading to further margin expansion through operating leverage – large growth runway.

Total sales in the first two quarters of FY23 are almost equal to total sales for FY 22. Profits are already higher. Such a business trades at 18.5 times trailing earnings.

Why? Promotor disputes - family has 4 brothers. But this overhang may be going away soon.

One brother runs the Bombay Division (holds IP for Maharashtra and south states). Rest form the Ahmedabad Division and control Vadilal International (promotor of Vadilal Industries) which owns Vadilal IP and licenses it to Vadilal Industries for rest of India and international

Ahmedabad division brothers have been fighting from time to time, lodging cases on each other (no impact on business). This has been an impediment to Vadilal Industries (and Vadilal Enterprises – the distribution arm for rest of India) getting sold to a PE – tried and failed.

Last week Vadilal Industries announced its intention to buy out the Vadilal IP from Vadilal International at maximum consideration of 676cr. This may pave the way for a potential PE buyout of Vadilal Industries and (maybe) Enterprises. There are unanswered questions though.

How has the value of 676cr been arrived at? Is this too much, as the company itself trades at 1800cr? Or is this reasonable as the company is growing rapidly and the operating cash flow for first half FY23 are already 130cr? How will this be funded? Is a buyer identified?

Upside potential: if there is indeed a PE buyout, the promotor overhang will be gone and we can be sitting on a massive rerating to normal FMCG multiples. US and international business should continue to grow at 20-25% and the India ice-cream market is also picking up steam.

Risks, uncertainties, unknowns:

All points listed in 10

No PE buyout at all

No regular information flow from the company – no concalls, no ppts, very few interviews

Seasonality

Slowdown in the US impacting demand

India business not gaining share

In spite of the risks, I personally find the risk-reward favorable. I have taken a small position (4% of PF) and will add if a buyout goes through – remember there is no announcement, this is just me speculating. This is risky and not investment advice. I may sell anytime.

No idea @ashutosh37, no announcements from the company. The delivery lercentages are not very high so looks like speculative activity in tbe run up to results - possibke that people on the inside expect good results.

I haven’t made a re-entry yet. Want the re-entry to be either at an extremely low price so I can digest the tisk of some of the randomness that comes with their business delivery, corporate actions and price manipulation, or at a higher degree of confidence that the domestic business is turning around for good. Weighing the risk reward from.time to time.

NCLT case closed that was filed in 2017-18, no notice filed in NCLAT till now. looks good. numbers quite decent despite strong season. not sure if they are loosing market share

I’ve been comparing Mrs. Bectors’ business with Vadilal Industries. Despite similar sales and PAT figures, Vadilal has better current and historical ROE and ROCE, and a decent balance sheet. However, Vadilal’s P/E ratio is about one-fourth of Bectors’. Could this be due to factors like a lack of updates on Vadilal’s expansion plans (no quarterly updates since 2020), minimal FII/DII presence, or history of conflicts among promoters? Are there other reasons

/red flags for this discrepancy? Your insights would be appreciated.

Disclosure: Interested but doesn’t hold any position currently