These are the EPS and Sales forecast for the company. The company is actively covered by 2 analysts at the moment.

EPS

Sales

These are the EPS and Sales forecast for the company. The company is actively covered by 2 analysts at the moment.

EPS

Sales

Can I ask you from where you get this earnings forecast data? I can’t see in Tijori or Tickertape. Any new website, or research reports?. Please share the resource

The above screenshots are from ticker tape. Will be visible to Pro Subscribers.

EMS operates at10-15 % win rate for the bid while Va Tech has a win rate of 30-40%, thats why VA Tech has Order Book to Market Cap ~ 2 while EMS is at <1, so it boils down to either better EBITA or robust order book

WABAG Wins ₹360 Crore Orders from GAIL & IOCL

Chennai, March 13, 2025 – VA TECH WABAG, a leading water technology company, has secured two major orders worth approximately ₹360 crores:

GAIL Project (₹340 Crores) – WABAG will design, build, and operate a Zero Liquid Discharge (ZLD) plant, an effluent recycling unit, and a wastewater treatment facility at GAIL’s petrochemical complex in Pata, Uttar Pradesh. The project includes 24 months of construction followed by six months of operations & maintenance.

IOCL Contract (₹20 Crores) – WABAG has received a three-year extension for operating and maintaining the Tertiary Treatment Reverse Osmosis (TTRO) plant at IOCL’s Panipat Refinery, Haryana. WABAG originally designed and built this plant, India’s first industrial water recycling facility in the oil & gas sector.

WABAG’s Head of Sales & Marketing, Mr. S. Natrajan, highlighted that these repeat orders reflect strong customer trust and reinforce WABAG’s leadership in industrial water treatment.

Wabag’s numbers are amazing. It’s not just the current quarter or year, but the last 5 years of Net Profits, especially Free Cash Flows - rock solid!

And when one looks into their history, it’s easy to understand why they are optimising for Free Cash Flows & higher Profit margin business only.

Wabag suffered & went through the painful years from 2015 to 2020 because of multiple factors going against them (discussed extensively on the thread above)

After that, they came up with the ‘Wriddhi’ strategy, and the results have been the Analyst’s dream.

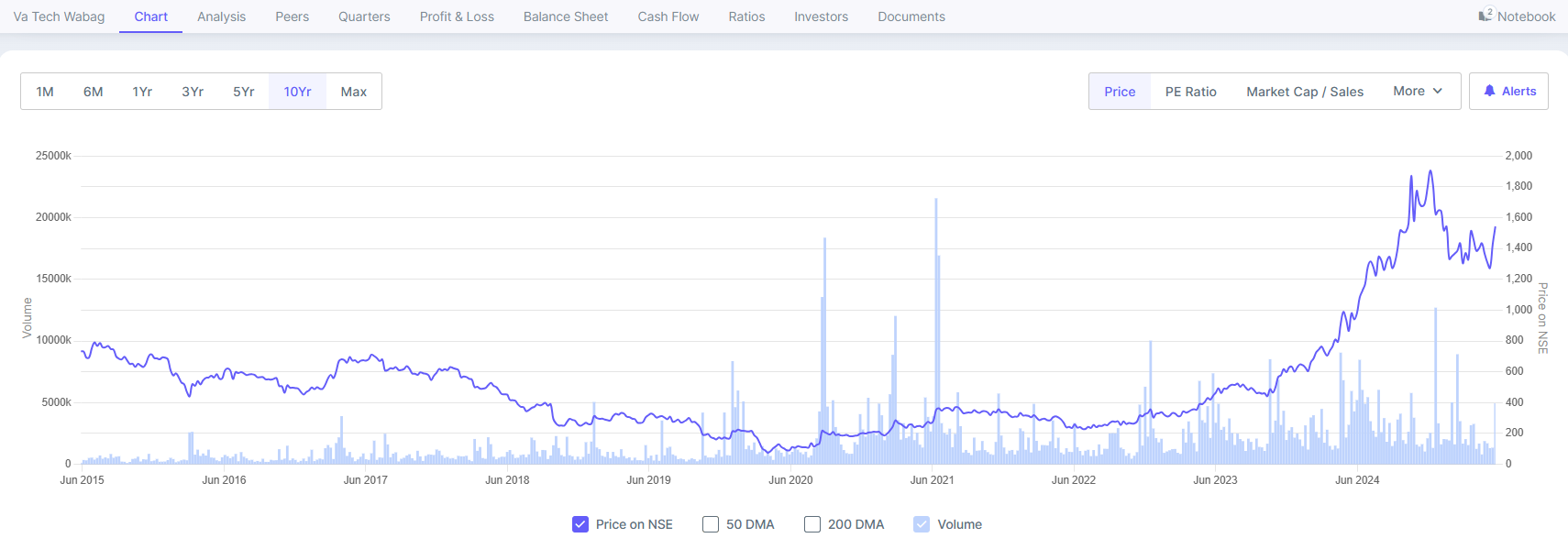

This has majorly reflected in the stock price over the last 10 years.

Now, what would be the right valuation can be subjective to each.

Zooming out to a 15-year horizon, it’s in the upper bandwidth of historical valuations, from all metrics - PE ratio, Market Cap to Sales, Price to Book

Going forward, there is high earnings visibility with a strong orderbook at Rs137 Bn. That’s 4x Revenue, beating their guidance of 3x. And likely, they’ll have more order wins (inc the big Saudi order) soon.

https://youtu.be/D0wklt0_3CQ?si=PwitvL4tkOiHDzgT

Management has also clearly shifted focus from European subsidiaries to emerging economies - India, the Middle East, and Africa.

That is for better profitability, with labour cost likely to be the difference.

However, Europe might have better Water sanitation projects

At the same time, there’s the risk of the USA cutting funding for projects outside of the USA. The Trump administration is clear where their priorities are, along with DOGE having a singular objective of reducing the US Debt/ spending.

So, to conclude, Wabag has already executed their strategy ‘Wriddhi’ quite well & improved all the business metrics, especially from the ‘analysts’ pov & it’s reflecting in the valuations.

A couple of key metrics, such as Revenue growth, EBITDA%, and others are at the lower end of the guidance.

There is good revenue visibility, and there are evolving macros.

The speed of executing projects will be the key monitorable going ahead.

Usual disclaimers apply. Pl do your Due diligence.

VA Tech Wabag sees a significant opportunity in cleaning India’s rivers, including the Yamuna, with potential projects worth $1 billion over the next 3-5 years, [according to ICICI Direct]. Wabag plans to participate as a technical EPC (Engineering, Procurement, and Construction) and O&M (Operations and Maintenance) partner to execute these projects. Specifically, Wabag has been involved in sewage treatment plant projects in cities along the Yamuna, like Agra and Ghaziabad.

Growth runway looks strong: ![]()

No Reco ![]()

I attended the annual Investor Meet last Friday.

In addition to the summarised details above, here’s what I make of Wabag at the current juncture.

Most of the conversation/ focus was on what has been accomplished.

The Middle East and Africa, especially the GCC, will be the only growth region going forward.

At the overall level, while there are chances that Wabag will execute fast, I sense that Revenue growth as well as EBITDA will, at best, reach the upper end of guidance.

No problems there. It provides consistency and stability of a mature business.

Most of the management, right from Rajiv Mittal, looks quite content with what has been achieved. And deservingly so, Wabag has done well.

As for Rohan Mittal, a snapshot of his LinkedIn profile gives an idea of how quickly he has risen through the ranks. And is already at the leadership team.

The confidence with which the management spoke about the Saudi order, it will be surprising now, if there isn’t a positive announcement within a few weeks.

While there’s always a possibility of higher valuations, to me, Wabag is fully priced in. So, I’m happy to book the profits here (soon).

Disclosure: Likely biased. Not a registered Investment advisor.

https://x.com/ETNOWlive/status/1935301234195402826

— sit tight on your investment

— as they say “market can stay irrational longer than you can remain solvent”

Deep analysis on WABAG: https://youtu.be/cF9cq1nHN1A?si=WGs9S_gXuNYJbjcb

Must watch !!!

Order

WABAG secures INR 380 Crores Order from BWSSB, funded by World Bank, for State-of-the-Art, Energy-Efficient Water Reuse Facilities in Bengaluru -

WABAG receives a Letter of Award for a 300 MLD Mega Sea Water Desalination Plant in the Kingdom of Saudi Arabia, worth about USD 272 Million (SAR 1,019 Million / INR 2,332 Crores)-

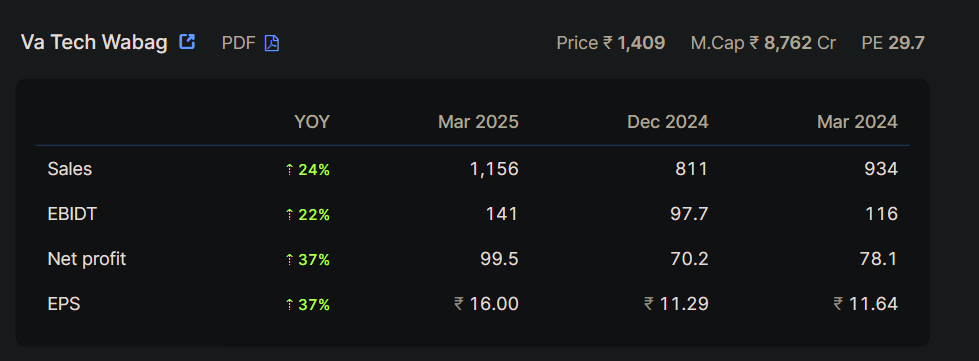

Superb and consistent performance delivered by the company. YoY the revenues have increased almost 15 percent to Rs 734 Cr and the NP has increased 20 percent to Rs 66 Cr , with the operating margins intact at 13 percent. The order book stands at Rs 15800 Cr which is 4 plus times the annual revenues. Press release attached.

Wabag.pdf (134.8 KB)

I am attempting to understand how to most accurately forecast VA Tech Wabag’s operating revenue. There are two approaches:

Pro: straightforward

Con: order book has consistently grown faster than revenue, and it seems revenue is being somewhat capped so that the company can focus on delivering profitable growth. Hence, the relationship is not linear.

Pros: Most accurate method to forecast long term infrastructure projects

Cons: VA tech wabag does not have an easily retrievable list of ongoing or recent orders. Announcements of orders also lack details such as expected start/end date, breakdown of DBO between build and operate, and so on.

Does anyone have a reliable source for details regarding the second method? If so, let’s collaborate on making the most apt revenue forecast that can be updated with every passing quarter.

I conducted a DCF on VA Tech Wabag and derived a fundamental value of 1,039 whereas the stock is currently trading at a 1.5x multiple.

My assumptions were 14.8% growth and a 14.2% WACC, with 5.4% terminal growth. The 1.5x premium currently indicates that the market is pricing in 23% growth with the remaining assumptions.

Relative valuation also indicated that VA Tech Wabag is trading at overvalued status.

If you could explain the assumptions behind WACC @14.2%?

Any comments on the WACC assumptions?

I was hoping you could explain your the assumptions behind WACC