Wabag entry in Solar PV Sector by bagging an order worth Rs 1000 Cr

Va tech.pdf (417.8 KB)

The business is doing good, I’d say stay put, don’t make the mistake I made. I sold it after it gave me 2x, and the stock price is up 50% from those levels and I regret selling it now.

technically, every town, city needs a water treatment plant and we are nowhere near there in any sense. This company will grow ONLY if the clean India movement is taken up holistically and water treated before discharge. After the Jal Jeevan mission, if the Gov funds water treatment plants both for drinking and sewage at scale, this company will be big.

The downside is, only the Gov state or local will do this and money flow will forever be inconsistent from the time of winning the bid to actually seeing the money flowing in as revenues.

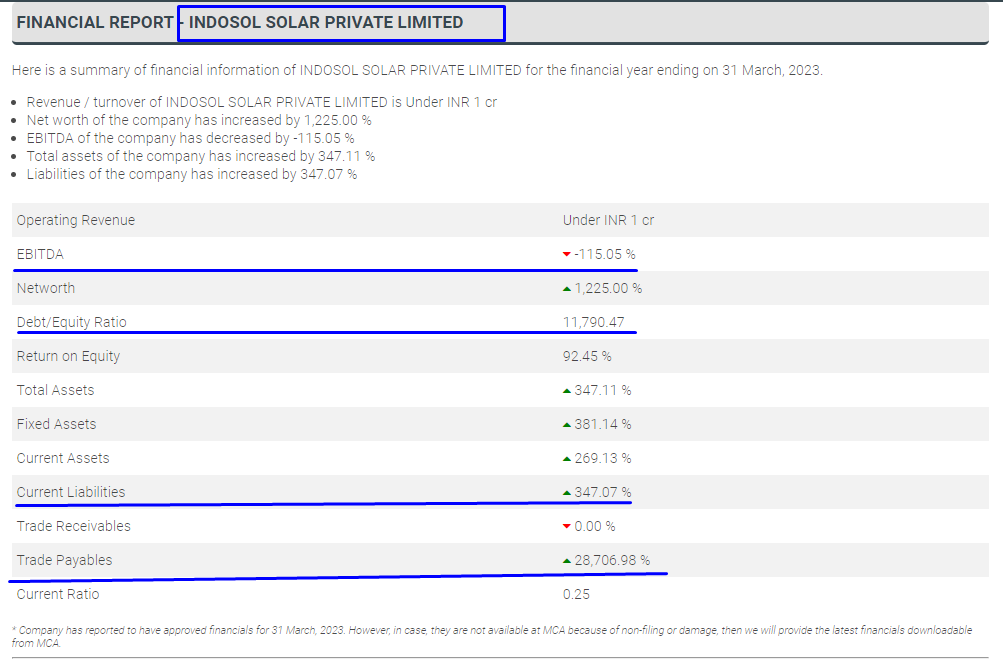

Good observation. It seems Indosol Solar’s financials are stretched. But I’m sure Wabag’s order will be backed by some Multilateral agency’s guarantee, as the management has always stressed on that.

Stock is in a blow-off top following a breakout from running wedge. while hard to pinpoint the top, paying 45x PE for a 15% growth(incl semiconductor, green hydrogen tailwinds) doesn’t offer good risk-reward. Euphoria around order wins and orderbook is not factoring that orders are executed over years.

While the valuation may be stretched. But this is how generally markets work. An undervalued stock over time becomes overvalued. Just like a stock can remain undervalued for extended periods of time same can can happen with overvaluation. Hence selling on such overvaluation is very difficult. However, if you suggest me a better company in the sector having better prospects I may think to swap.

Unlike, consumer focused sectors, cyclical and infrastructure plays don’t remain overvalued for longer period.

Also, technically, looking back at winning stocks, I’ve seen stage2 phase in a stock typically lasts for 12-18 months. Then stock undergoes either time or price-wise consolidation.

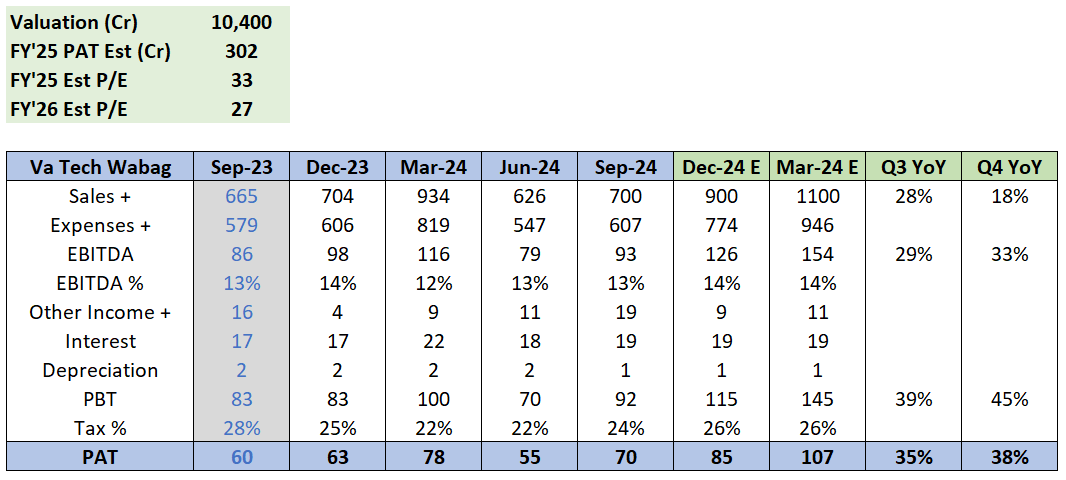

I feel if we take forward earnings of 2026, expecting a PAT of around 300 cr. That values it at 35 times fy26 earnings. I also feel the 15% growth will get re rated to a higher number on actuals. The management is very conservative in my view and may surprise on the positive side. Markets are factoring it now and the move last week was due to fund buying

Based on my own experience over several years of investing in small caps, I’d argue that one should be very careful with optimism on stocks where multiples have run way ahead of their earnings which is the case with Va Tech Bag where stock is now 3x its historical valuations.

That’s already too much premium factored in by the market based on all the potential positives including the ones you have mentioned.

Forecasting certain growth numbers for a company is full of risks. It doesn’t work for established players, let alone smaller companies. You can have regulatory changes, technological disruptions, competitive threats etc that can swing ratings either way for a stock. While we mostly think about the upsides, downsides is what one should be careful of and having a good margin of safety is what will protect one’s portfolio from potential downside.

We all have seen or heard about retail investors chasing great narratives and growth forecasts in PSU defense, railways and oil and gas stocks as well as new age stocks at crazy valuations with not so happy consequences. And this all happened in the middle of institutions still buying into these stories, launching new fund offers etc.

P.S.- This is not to say that Va Tech is not a good company. But as they say in investing, good company always doesn’t translate into a good stock and vice-versa. I have seen people holding Dmart, a highly promising story in 2021 disrupted by quick commerce, for last 3 years without any return. Doesnt make Dmart a bad company though, but those hoping for similar returns as stock gave in preceding years have been disappointed, having fallen on the wrong side of valuations.

While Wabag has been 3x of historical valuations, the PAT has also grown at a 45% CAGR + the Sector as a whole has picked up only now. Where i derive the valuation comfort is below

Based on the Management guidance in the recent concall - They have guided for 2k Cr topline with margin in the range of 13-15%. Basis this for next 2 quarters, i would forecast a rev growth of 28% and 18% respectively coupled with a PAT growth of ~30-35%. This would result in an annual profit of ~300 Cr for this year.

If we extrapolate the guidance for next year with a 15% topline growth and a 20% bottomline growth, the fwd valuation comes to ~27 times FY’26 earnings which passes my check on valuation comfort

What is comforting to me overall from a longer term perspective

Global leader in Water Technology - 100 years of survival speaks volumes

Conservative and Prudent Management

Sectoral tailwinds across the globe

Net Cash Balance sheet

Orderbook visibility

Semiconductor play - Orders should start flowing in from H1 Next Year

Risks

Execution Risks - Hence review every qtr if management is walking the talk

Regulatory Risk - Govt policy changes / Annual budget allocations

Disc: Invested for longer term since 1 year. Pls do your own due diligence

One important math’s of order book economics

EP Projects: 24-30 months

EPC Projects: 36-42 months

O & M: 2years to 10 years

As per my understanding and execution capability under Three Phase strategy, Design and Egg (15-20%), Construction and Supply (50-60%) & Lastly Installation and commissioning (15-20%), at the H2 part of FY26 will be very promising for the company.

Intimation to exchange.pdf (490.6 KB)

WABAG secures 7 years Operation Contract order worth ~USD 14 Million (~INR 121 Crores) for the BAPCO Refining Industrial Wastewater Treatment Plant, Kingdom of Bahrain

Wabag | Rating Update

India Ratings & Research (Ind-Ra) has upgraded VA Tech Wabag’s (VATW) long-term credit rating to ‘IND AA-/Stable’ while affirming its short-term rating. The upgrade is due to improved profitability (EBITDA margin at 13.2% in FY24) and debt-free status.

Strengths:

- Leading player in water treatment with a strong order book (₹134.1B)

- Focus on profitability and stable revenue

- Strong credit metrics and asset-light model

Weaknesses:

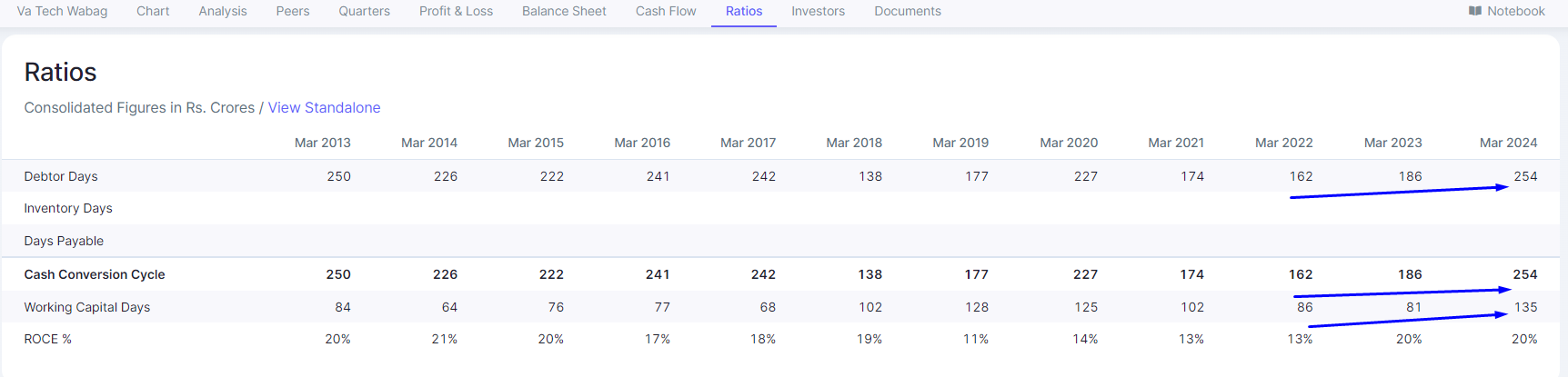

- Elongated working capital cycle (receivables cycle at 250 days)

- Exposure to cyclicality and forex risk

Liquidity: Adequate, with ₹5.2B in cash, stable cash flow, and manageable debt repayments.

Future Outlook:

- Positive: If profitability & working capital improve further

- Negative: If working capital cycle worsens or profitability declines

WABAG secures consortium order worth USD 371 Million (~INR 3,251 Crores) for Al Haer Independent Sewage Treatment Plant located in the city of Riyadh, the Kingdom of Saudi Arabia

Full Link - BSE

Va Tech Wabag | Management Interview

- Comfortable at 13-15% EBITDA Margin range; Guided for 15-20% revenue growth

- Company will execute Rs 1,700 Cr out of the Rs 3,251 cr order received for the sewage treatment plant in Riyadh, Saudi Arabia

Watch the management interview here

this is a video to see the quality of work by WABAG.

Delhi Yamuna river

— massive opportunity in making for co

— more-fully so because we have a strong & decisive government at the anvil

— it will be interesting to see how they take advantage & benefit from it

— plus they already have executed 3-4 projects in past entailing yamuna