Hi @ceoji … I absolutely agree to your analysis. V2 was a big part of my holding since 35 levels ( at one point more than 45 % of my PF ) . I had exited partially around 400-420 and the rest after Q2 results and concall. The revenue growth and SSSG was faltering from last year Q3 onwards but I guess ownership bias kept me invested . I was hoping they would be able to sort the issues but that did not happen.

Turning around a business and scaling it up is a totally different ball game. I guess the management was kind of overconfident in their guidance and finally the ground realities caught up. Will be very surprised if they show good growth in Q3 .

2 Likes

I am still holding v2 and confident they can clock a revenue cagr of 30%+, it is still a small company, they are overconfident now, but things will be realised by the management sooner or later,

Good Results from V2 Retail

2 Likes

Yes good results from V2 Retail. Hoping it will continue to expand and increase competitiveness to push same store sales.

Results are good but for some reason Market is not rewarding it. Only reason I think of is Intense competition . After budget and this year we have 50% more auspicious days for marriage than last year , which is a good sign for consumption sector and hopefully V2 benefits from it.

Yes, I agree, the market is not yet convinced about the turnaround and the ability of the management to scale up.

and @ruffles,

You are spot on,This is a consumer-facing retail business, and they have to be at the top of their game.The big players like Avenue Supermart ,Trent and V-Mart,among others,have learned their lessons,plus they have deep pockets.

and @Sailor1980,your remark about the foray into e-commerce, is well taken,as only time will tell.Their target customer segment may not prefer on-line over off-line. E-commerce is a different ball game altogether,with low entry barriers,but multiple skill sets and market strategies to deploy. So, the learning curve could be steep.

and @ceoji, I agree management capability and market perception are key factors on share valuation. Management will have to show consistency in strategies and results in varying market cycles,in retail with retail’s razor thin margins.

So,my take, based on the above discussion, and on the really valuable contributions on this thread, is that the markets are in watch-and wait mode,not only with respect to V2 Retail, but in general also,with the overhang of the coming general elections. So,this could be a long story to unfold.Hence,will hold in wait-and watch mode.

Disclosure. Holding Tracking position,with losses.

V2 is completly different to avenue supermart. Only comparable peer is V-Mart retail.

In hyderabad, Dmart and V2 mart are in side by side

Has anyone recently seen V2 retail store how is the ambiance and footfall looks in the store.

Any news on V2 retail, pls share

My cousin worked as legal counsel in V2 Retail for some months and then quit.

Reason :

- Bad business practices

- Holding payments of vendors for no concrete reason

- Promoters using operator for stock manipulation to make bucks on the side

- Other shady things

Those who are invested can take a call on their position.

Disclosure : Not invested and there’s no bias against the company.

9 Likes

Anyone tracking this company. The valuations have turned very attractive with market cap around 350 cr. For FY22 Mgmt had guided sales of 900 cr from existing stores and approx 100 cr from new stores (20 new stores planned in FY22) and ebidta margins of 9%.

From current valuations this appears very cheap. Are there any red flags?

Trying to ascertain whether the fall in valuation is due to second wave or something else.

Disc. Invested 3% of portfolio. To increas once conviction improves.

5 Likes

Key points from the Q1 FY25 earnings call:

Key Financial Performance

- Record Quarterly Sales: V2 Retail achieved its highest-ever quarterly sales in Q1 FY25, with revenue from operations reaching INR 415 crores, up 57% year-on-year.

- Profitability: Gross margin stood at 29%, and EBITDA grew by 56% to INR 55.5 crores. The net profit (PAT) increased by 162% to INR 16.3 crores.

- Same-Store Sales Growth (SSG): The company reported robust SSG of 37% and volume growth of 55%, driven by a high proportion of full-price sales (93%).

Operational Highlights

- Store Expansion: V2 Retail added 10 new stores in Q1, bringing its total count to 127 stores. The company plans to add 40-50 new stores this year, primarily in Tier I and II cities, and underserved markets.

- Private Label Growth: The contribution from private labels rose to 80%, with a target to reach 100% in the next 1-2 years. This strategy is expected to enhance brand identity and customer loyalty.

- Inventory Management: Inventory aging improved, with the share of stock over a year old dropping to 7% from 23% two years ago. The goal is to reduce aging inventory further.

Strategic Focus

- EBITDA and Margin Goals: Targeting a pre-IndAS EBITDA margin of 8-9% and a PAT margin of 4.5-5.5% for FY25.

- Expansion Strategy: Planning to invest INR 110 crores in store expansion, inventory, and working capital, funded through internal accruals.

- Targeted ROE: The company aims to achieve an ROE of 20-22% through increased sales and improved operational efficiency.

Competitive Landscape

- Positioning Against Competitors: V2 Retail faces competition from brands like Zudio, Reliance’s Youthstar, and others. However, it differentiates itself with lower average selling prices and a focus on family shopping, especially in kids’ wear.

- Pricing and Margin Strategy: Emphasis on cost-effectiveness allows V2 Retail to pass savings to customers without reducing gross margins.

Key Challenges

- Store Profitability: The company has worked to ensure each store contributes positively to EBITDA, with no EBITDA-negative stores this year.

- Cost Management: Rising employee costs due to new store openings impacted margins, but the company aims to maintain cost efficiency through better technology and supply chain improvements.

Future Outlook

- Growth Projections: The company expects revenue and EBITDA to grow by 30-40% annually, supported by continuous demand and a favorable market.

- E-commerce Entry: V2 Retail is evaluating an omnichannel approach, using store inventories to fulfill online orders within city limits, potentially reducing logistics costs.

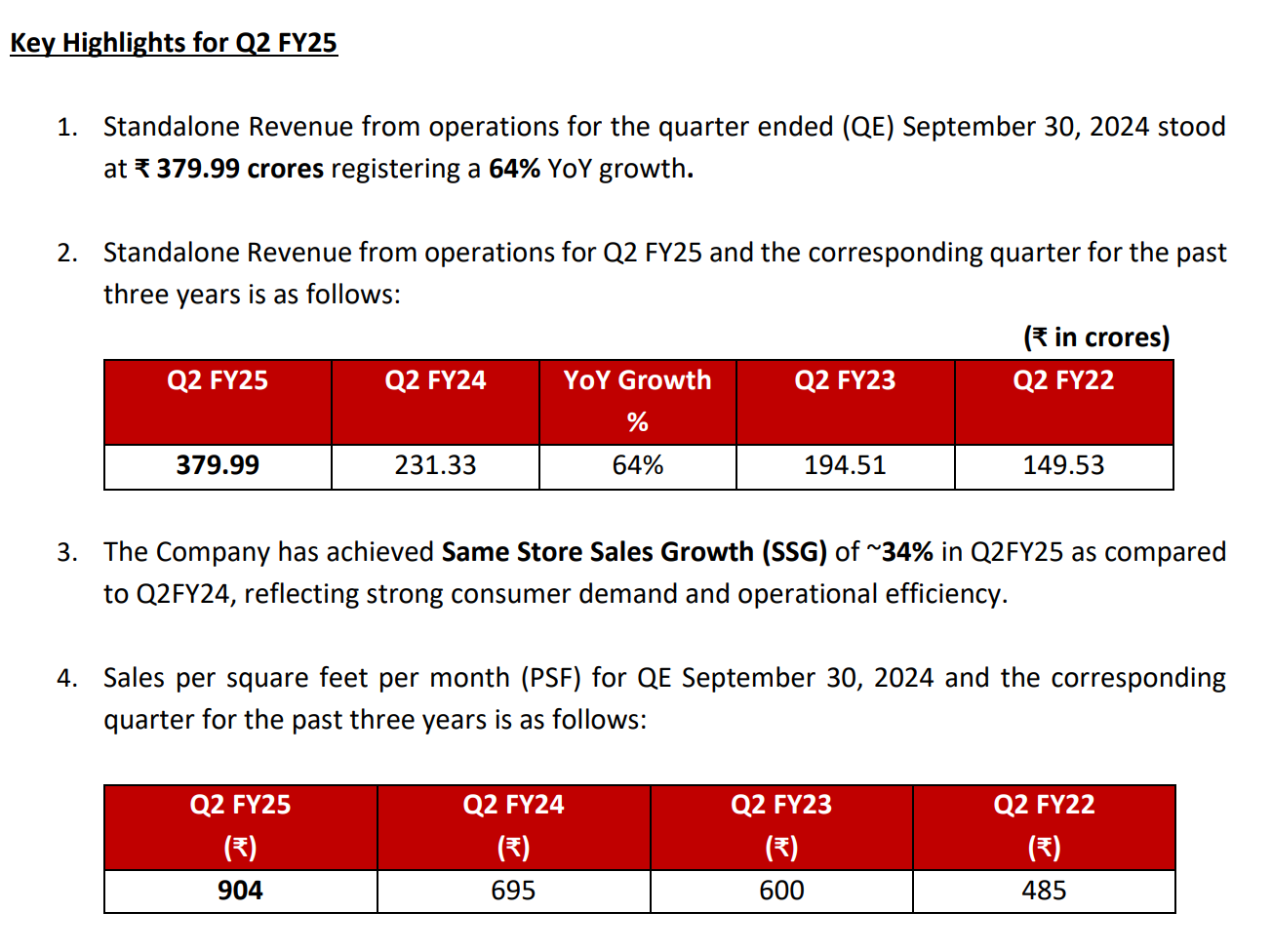

Latest Q2FY25 Update -

Disclosure - Invested

3 Likes

V2Retail

-

30-40 % REV Growth in coming years

-

Targeting PAT Margins 4-5 %

-

RoE > 20 %

Store Expansion Growth 50 % CAGR

-

50-60 stores in FY25

-

60-70 stores in FY26

Management guidance

Fashion theme seems to be picking up wrt value fashion in particular.

V2 retail and Vmart both have done well

5 Likes

A Report on V2 from Nuvama.

4 Likes

Wrote a blog post highlighting the trend building up in Value Fashion-

5 Likes

v2 Retail.pdf (573.0 KB)

another report of nuvama on V2 after Q2 result

Competition update for V2 retail :

BAAZAR STYLE: Company has opened two new stores of Style Baazar one at Sahebganj, Bihar and another at Chakradharpur, Jharkhand today.

With these additions, the total number of stores as on date stands at 197.

The company has 630 crore of debt with debt/equity of 2.19. I am trying to understand the management’s response:

The debt that we have on our books is essentially for bill discounting. So, our vendors have a facility where they can take payments and they can discount their bills whenever they want. So, we have a CC limit from the bank, and we use it because we want to be one of the best paymasters in the industry.

Is it a standard practice in the industry? A company taking debt and paying an annual interest to keep their vendors happy? I am sure it affects the financial ratios of the company. Can someone explain how is it working.

2 Likes