Urban Company Limited (formerly known as UrbanClap Technologies India Limited) is a technology-driven platform primarily engaged in providing home and beauty services.

Core Business and Model

- Primary Business: The company operates an e-commerce platform via its online portal (www.urbancompany.com) and its mobile application (the “UC App”).

- Function: The platform enables registered customers to search and hire service professionals for their household and beauty needs.

- Product Sales: The Group also sells various items related to its services:

- Products, tools, and consumables to its service professionals for use during service delivery.

- Home appliances to consumers under its ‘Native’ brand.

Corporate Details

- Incorporation and History: The company was incorporated on December 22, 2014. It was initially named “UrbanClap Technologies India Private Limited” and was rebranded to “Urban Company Limited” on April 2, 2025.

- Promoters: The promoters of the company are Abhiraj Singh Bhal, Raghav Chandra, and Varun Khaitan.

- Geographic Focus: The business segments include India consumer services and an International business segment. The company launched operations in Dubai in 2018.

Financial Performance & Health

| Revenue Segment | FY23 Revenue (₹ Cr) | FY24 Revenue (₹ Cr) | FY25 Revenue (₹ Cr) |

|---|---|---|---|

| India Consumer Services (Core Services Commission) | 570.0 | 709.5 | 881.4 |

| International Operations | 66.6 | 89.5 | 147.1 |

| Native Brand Products (RO Purifiers, Smart Locks, etc.) | 0.0* | 29.0 | 116.0 |

| Total Operating Revenue | 636.6 | 828.0 | 1,144.5 |

| Feature | Description |

|---|---|

| Model Type | Closed Marketplace / Full-Stack |

| Control over Quality | High ; the platform mandates standardized training, verification, and background checks for professionals. |

| Pricing | Standardized across services, controlled by the platform. |

| Commission/Fees | Charges a High Commission (e.g., 20% to 30%) on every service booked, which is its main revenue source. |

| Vendor Autonomy | Low ; the platform controls the process, pricing, and job matching. |

| Additional Revenue | Sells branded products/service kits to professionals, charges for training, and earns revenue from premium memberships and advertising. |

| Value Proposition | Convenience, Trust, and Guaranteed Quality due to centralized oversight. |

Urban Company’s expansion plans are centered on a multi-pronged strategy encompassing geographical growth, service diversification, and a major push into instant services and own-branded products.

Here are the key aspects of the company’s expansion plans:

1. Geographical Expansion

- Deepening India Presence: The company plans to expand its network from major metropolitan areas to Tier-2 and Tier-3 cities across India, aiming to eventually serve the top 200 cities in the country.

- International Strategy Shift: After facing operational difficulties, the company is shifting away from building standalone operations in new global markets.

- Focus on Partnerships/JVs: The new approach is to leverage partnerships and joint ventures, such as the one in Saudi Arabia with a local partner and a partnership with e-commerce platform Noon for the UAE and Saudi Arabia.

- It continues to operate in UAE and Singapore, but with a recalibrated strategy. The company has previously exited markets like the US and Australia.

2. Service and Product Diversification

- The “Native” Product Line: Urban Company is making a significant move from being purely a service provider to a services-plus-products company by launching its own line of consumer durables under the ‘Native’ sub-brand.

- Current Products: This includes smart RO water purifiers and electronic door locks.

- Future Plans: There are plans to expand this product line further, with sources indicating a potential launch of its own line of air conditioners (ACs) in the near future.

- New Service Categories: The company is continuously adding new categories to meet evolving consumer needs:

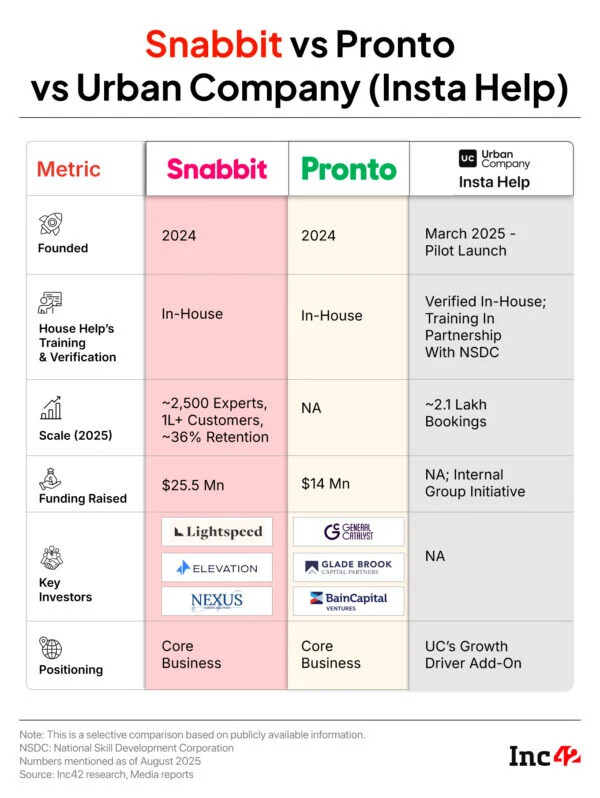

- “InstaHelp” (Instant Services): This is a new major focus to offer on-demand services, such as domestic help or cleaning, within minutes (e.g., within 15 minutes in some core markets). This is a strategic move to capture the quick commerce demand and build a “strategic moat” around its core business.

- Potential Future Categories: The company is exploring high-growth categories like fitness, elder care, and healthcare services.

3. Technology and Operational Investments

- Technology Development and Cloud Infrastructure: A large portion of the IPO proceeds is specifically earmarked for new technology development and scaling cloud infrastructure. This investment is crucial for supporting the planned expansion into 200 cities and the rapid deployment of new services like “InstaHelp.”

- Data-Driven Operations: The company uses proprietary machine learning and AI to optimize micro-market operations (3-5km radius areas), which helps to minimize travel time for professionals and maximize their earnings, thereby supporting the scale-up of instant services.

- Marketing Activities: A portion of the IPO proceeds is allocated to marketing for customer acquisition in new cities and brand building in competitive markets.

Core Profitability Strategies (Revenue Model)

Urban Company’s strategy to achieve and maintain profitability is based on a “full-stack” model with diversified revenue streams:

- Commission from Services (Primary Revenue): The company earns its primary revenue by charging service professionals a commission (typically 20-30%) on the total price of the service booked through the platform.

- Lead Generation Fees: For non-fixed services, professionals pay a fee to buy and bid on customer leads, ensuring a revenue stream for Urban Company even if the booking is not finalized.

- Product and Kit Sales (High Margin): The company generates additional revenue by selling proprietary and branded tools, consumables, and service kits (e.g., facial kits, cleaning solutions) to its service partners, earning an average margin of 20–30%.

- Direct-to-Consumer (D2C) Products (Native): The company has launched its own hardware brand, Native, for products like RO water purifiers and smart door locks. This is a strategic move that creates a closed-loop system, as the products require future maintenance and replacement services, increasing customer stickiness and generating high-margin revenue.

- Subscription/Membership Plans: The platform offers paid premium memberships (like UC Plus) to service partners for benefits such as priority leads, better visibility, and marketing support, creating a recurring revenue stream.

Operational and Growth Plans for Sustainability

- Customer Retention and Unit Economics: High customer loyalty is a major factor, with 82% of its Net Transaction Value (NTV) in the consumer services segment coming from repeat customers in FY25, which significantly reduces customer acquisition costs.

- Focus on Operational Efficiency: The company is driving operational leverage in fixed costs and increasing efficiency across its cost base to improve its bottom line.

- “InstaHelp” Instant Services: A major future plan is to aggressively expand its instant service offerings (like domestic help within minutes) to attract clients who expect quick commerce, though this new vertical may require initial investments that could temporarily pressure margins.

- Partner Empowerment: By investing in training, providing living wages (average earnings of service partners are approximately ₹26,400 per month, net of costs, in FY25) and social security benefits, the company ensures a high-quality, stable supply of professionals, which in turn drives high customer satisfaction (average rating of 4.81/5) and retention.

- Strategic International Expansion: International revenue grew by nearly 64% in FY25, and the company has adopted a strategic approach by shifting to joint ventures in some markets after achieving operational profitability in markets like the UAE.

Competition Landscape:

| Competitor | Key Services & Model |

|---|---|

| Housejoy | Offers a wide range of services including painting, carpentry, plumbing, pest control, and beauty services. It is one of the most popular platforms and a major rival in India. |

| HomeTriangle | A key comparison point; it operates an Open Marketplace model, connecting customers with service providers who have more flexibility to set their own rates and manage their schedules. |

| Zimmber | A comprehensive platform covering a wide range of home services including cleaning, repairs, and pest control. |

| Quikr Services | One of India’s largest commercial expert services, offering over 20 services in 600 localities. It is a community-based infrastructure and marketplace. |

| Timesaverz | Offers home cleaning, beauty services, appliance repairs, and other household tasks. |

| Handy & TaskRabbit | Global/cross-market competitors that connect customers with professionals for various tasks, including cleaning and home repairs. |

Comparison: Urban Company (Closed) vs. Open Marketplace (e.g., HomeTriangle)

| Feature | Urban Company (Closed Marketplace) | HomeTriangle (Open Marketplace) |

|---|---|---|

| Vendor Autonomy | Low; platform dictates pricing and process. | High; vendors set their own rates and manage their schedule. |

| Customer Choice | Limited; based on platform algorithms and vetted professionals. | Extensive; customers can choose from a wider range of competing vendors. |

| Commission to Platform | High; covers operational and quality control costs. | Low; platform has minimal operational control. |

| Quality Assurance | High; guaranteed by platform-driven training and standards. | Moderate; quality is vendor-driven. |

Financial & Business Risks

- Profitability Track Record and Sustained Losses The company has a history of incurring significant net losses and negative operating cash flows in previous financial years. Although it turned into a consolidated net profit in FY25, its long-term financial viability depends on generating adequate revenue growth and improving cost efficiency. Some analysts noted the FY25 profit was largely due to a deferred tax credit.

- Intense Market Competition The home services sector is highly fragmented, and the company faces intense competition from both offline players and other online platforms, which could negatively impact demand and service professional retention.

- High Valuation Analysts have cautioned that the IPO was fully priced at the upper band, meaning the valuation assumes the company will sustain its high growth and margin expansion, leaving little room for error or a near-term re-rating.

- Risk from New Segments The company’s aggressive expansion into new verticals like Native branded products, small home projects, and subscription services has a limited operating history, which adds uncertainty and makes it difficult for investors to evaluate long-term potential.

Operational & Labor Controversies (Gig Worker Issues)

- Partner Protests and Policy Disputes Urban Company has faced significant backlash and protests from its gig workers (“partners”), particularly in the beauty segment, over alleged unfair labor policies and working conditions.

- Stringent ID Blocking A major point of contention is the company’s policy of temporarily and permanently blocking partner IDs. Partners claim this is often done arbitrarily for reasons like low response rates or falling below stringent minimum rating requirements (e.g., 4.7 or 4.8 out of 5), which workers argue are difficult or impossible to maintain and out of their control.

- Unrealistic Performance Standards The new policies, sometimes associated with a “Mission Shakti” campaign, have been condemned by worker unions for allegedly implementing unrealistic minimum rating requirements and prioritizing customer happiness over worker well-being, leading to “slavery-like situations”.

- Operational Risks and Oversight The company is exposed to operational risks from misconduct or errors by its thousands of independent service professionals, which could materially impact its brand reputation and customer satisfaction.

Regulatory and Other Risks

- Pending Litigation There are pending legal proceedings against the company, its directors, promoters, and subsidiaries, which could result in penalties, liabilities, or reputational damage.

- Regulatory Exposure on Gig Workers Potential regulatory changes concerning the rights and classification of gig workers could lead to increased compliance costs and affect the company’s business model.

- Uncertainty in IPO Proceeds Use The planned use of IPO proceeds is largely based on internal management assumptions without external appraisal, introducing a layer of uncertainty on whether the capital will yield the expected revenues or profits.

Near-Term Key Monitorables (KPIs) :

| Area of Focus | Key Monitorables (KPIs) | Significance |

|---|---|---|

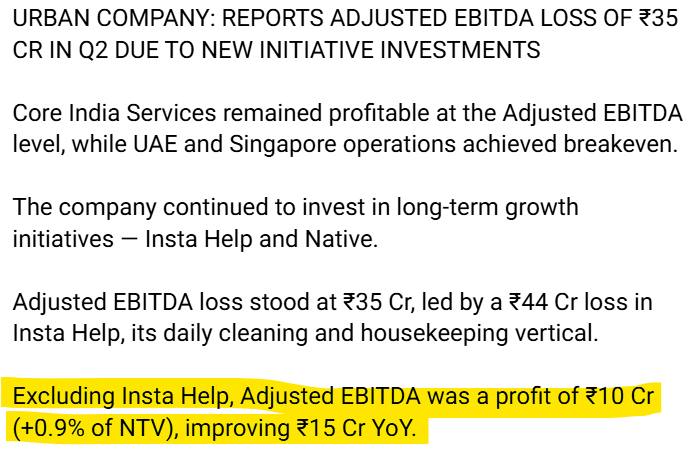

| 1. Strategic Growth: New Verticals | ‘Insta Help’ Scaling & Loss Trend: Order volume growth and the rate at which the segment’s quarterly loss widens or narrows. | Insta Help (on-demand household help) is a significant near-term investment. Monitoring its user adoption, repeat usage, and strategic long-term importance is crucial to justifying the short-term impact on consolidated losses. |

| 2. Strategic Growth: ‘Native’ Products | Revenue Growth & Adjusted EBITDA Margin: The growth rate of Native’s revenue (which has been surging) and the continued improvement in its Adjusted EBITDA margin. | The ‘Native’ product line (e.g., RO Water Purifiers, Smart Locks) is key to expanding the lifetime value of customers and the company’s ecosystem. Its path to profitability is a clear monitorable for the product strategy’s success. |

| 3. Financial Health | Consolidated Net Loss Reduction: The trend of overall consolidated net loss, moving towards or achieving the company’s first consolidated net profit. | While standalone operations may be profitable, the pace of loss reduction at the consolidated level is vital, particularly with heavy investments in new verticals and international markets. |

Longer-Term Key Monitorables (KPIs) :

| Area of Focus | Key Monitorables (KPIs) | Significance |

|---|---|---|

| 4. International Business | UAE & Singapore Break-Even and KSA Joint Venture (JV) Success: Sustained growth in profitable international markets and the effectiveness of the new JV model with SMASCO in the Kingdom of Saudi Arabia. | International expansion is a core part of the growth strategy. The KSA JV transition is a critical test of a market-localised, asset-light expansion model that addresses local market complexities. |

| 5. Ecosystem Stability | Service Partner Earnings & Retention: The average hourly earnings of service partners (especially female partners) and the continued investment in training, welfare, and wealth creation initiatives (e.g., PSOP). | A healthy supply-side ecosystem is the foundation of the marketplace business. Sustained high earnings and low partner attrition are long-term leading indicators of business quality and competitive advantage. |

| 6. Unit Economics | Service Partner Utilisation & Market Density: Improving service partner utilisation rates and deepening market density to drive faster service fulfilment and operational leverage. | The fundamental efficiency of the marketplace depends on these metrics. Improving these drives better margins and a superior customer experience, which are essential for long-term scale. |

Public Offering Details (IPO)

The RHP is for the company’s Initial Public Offering (IPO), which consists of a Fresh Issue and an Offer for Sale (OFS).

- Total Offer Size: The total offer size aggregates up to ₹19,000 million.

- Offer Components:

- Fresh Issue: Up to ₹4,720 million.

- Offer for Sale: Up to ₹14,280 million by several investors selling.

Proceeds from OFS: ₹14,280 million will be remitted to the Selling Shareholders, will not be available to Urban Company Limited.

Proceeds from Fresh Issue (Net Proceeds) : ₹4,720 million, which go to the company, are proposed to be utilized for the following objectives:

- New technology development and cloud infrastructure: ₹1,900 million.

- Lease payments for our offices: ₹750 million.

- Marketing activities.

- General corporate purposes: Up to 25% of Gross Proceeds.

Past Acquisitions:

| Acquired Company | Acquisition Date | Focus Area |

|---|---|---|

| Glamazon | March 2020 | A beauty services platform. This acquisition likely helped strengthen Urban Company’s core beauty and grooming vertical. |

| GoodService | August 2016 | A hyperlocal personal assistant and services app. This acquisition helped enhance the company’s technology and service booking capabilities. |

| HandyHome | January 2016 | A provider of after-sales services and repairs for home appliances. This move allowed Urban Company to expand into the appliance repair segment. |

Leadership Team:

| Name | Current Position | Education | Past Experience Highlights |

|---|---|---|---|

| Abhiraj Singh Bhal | Cofounder & CEO | # MBA Business Administration (IIMA) # BTech, Electrical Engineering (IIT Kanpur) | # Consultant, The Boston Consulting Group |

| Raghav Chandra | Executive Director & CTPO, Co-founder | # B.S. Computer Science and Engineering, Electrical Engineering (UC, Berkeley) | # Founder, Buggi, # Software Engineer, Twitter. |

| Varun Khaitan | Executive Director & COO, Co-Founder | # BTech, Electrical Engineering (IIT Kanpur) | # Consultant, The Boston Consulting Group (2+ years) # Engineer, Qualcomm California # Inventor on 6 US patents |

| Abhay Krishna Mathur | Chief Financial Officer | # Chartered Accountant (C.A.) # Ranked 49 (Final) and 42 (Intermediate) in C.A. exams | # Head Finance - HomeCare South Asia, 12 years at HUL |

| Mukund Kulashekaran | Chief Business Officer - India | # MBA (The Tuck School of Business at Dartmouth) # B.E., Computer Science (NIT Tiruchirappalli) | # Chief Business Officer, Zomato (3+ years) # Project Leader, Boston Consulting Group (3+ years) |

| Neha Mathur | Chief Human Resources Officer | # MA, Personnel Management and Industrial Relations (Tata Institute of Social Sciences) | # Head HR, Ridesharing (Uber, 2+ years) # Principal, Management Consulting (Accenture, 7+ years) # HR Manager, Reckitt Benckiser |

| Kanav Arora | Senior Vice President - Engineering | # B.S., Electrical Engineering and Computer Sciences (UC, Berkeley) | # Founding Member, Full Stack Developer (Stuph Inc.) # Lead Mobile Developer, Pocket Gems, # SDE II, Microsoft (3+ years) |

| Rahul Teotia | Vice President - Marketing | # M.B.A., Gold Medallist (IIM Indore) # B.E., Mechanical Engineering (Delhi College of Engineering) | # Consultant, The Boston Consulting Group (BCG) (3+ years) |

| Richa Mohanty Rao | General Counsel - Legal | # B.B.A.L.L.B (Symbiosis Law School) | # Partner, Cyril Amarchand Mangaldas (4+ years) # Senior Associate, Amarchand Mangaldas (7+ years) |

| Nitesh Agarwal | Vice President - UT DMCC | # MBA (IIM Ahmedabad) # B.Tech., Mechanical Engineering (IIT Kanpur) | # Senior Director, Swiggy (1+ year) |

| Sonali Singh | Company Secretary and Compliance Officer | # Post Graduate Diploma in Management (Finance) (IMT Ghaziabad) | # General Manager - Company Secretary, Paytm (2+ years), # Senior Manager - Corporate Secretarial, Indigo (7+ years) |

Offered Services and the user experience:

| Most Booked Services | Rating | Users given rating |

|---|---|---|

| Bathroom cleaning | 4.79/5 | 3.5M |

| Haircut for Men | 4.88/5 | 472K |

| Décor installation | 4.83/5 | 67K |

| Plumber consultation | 4.72/5 | 73K |

| Switchboard repair & replacement | 4.82/5 | 37K |

| Cupboard Repar | 4.76/5 | 39K |

Disclosure: Started tracking and have a small position. Not a recommendation. Do your own analysis before making any investment decision.

Sources:

Urban Company CEO On FY25 Profits, Margins & Growth Roadmap: