62 PE for 0-10% growth is quite expensive. Isn’t it?

Focus needs to be on higher margin at lower topline because they have exited all low margin franchisees and cleaned up the balance sheet. Earnings growth will justify the valuation

2 Likes

United Spirits Limited Q3 FY’24 Earnings Conference Call January 24, 2024

-

Prestige & Above segment clocked a double-digit growth of 10% year-on-year and overall net sales value growth of 7.5% year-on-year

-

The renovated bundle of Antiquity Blue is performing well in the launched markets

-

The steady strong performance of Signature and Royal Challenge American Pride

-

Royal Challenge American Pride continues to be our fastest-growing innovation. We have expanded the brand to 3 new markets: Himachal, Arunachal and Uttaranchal

-

In Assam, we have launched McDowell’s No. 1 premium smooth variant, which is at a premium to the core McDowell’s No. 1 Luxury in the state

5 Likes

3 Likes

It is not just growth but growth+longevity of growth which matters.

3 Likes

Hello Folks,

Interesting thread, I would like to ask about the topline growth?

i am asking because there is actually Degrowth in volume terms but due to premiumization top line in value terms is barely up in Single Teens.

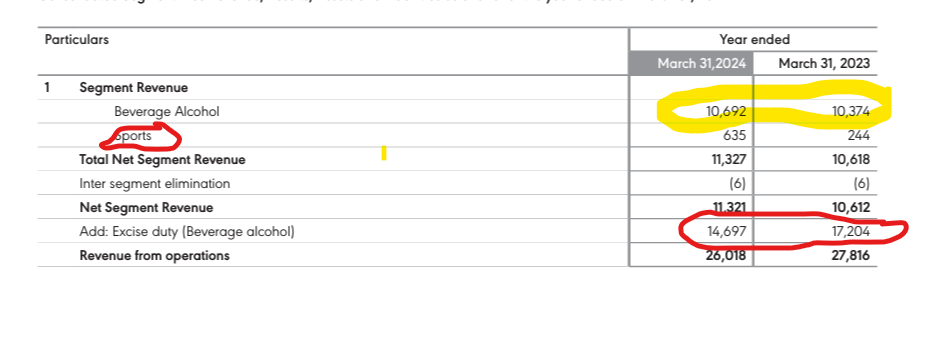

secondly, about segmental information, they had actually identified another segment as Sports, which is due to IPL and other sponserships.

so, if anyone had any thoughts about volume and topline growth prospects please explain the same.

Attaching a screenshot about segmental information.

Bodes well for USL

1 Like

RCB valuations now forms 18% of USL valuation.

1 Like

Summary of Q1FY26 Concall :

- The company isn’t sure about the overall impact of the new Maharashtra excise policy but their assessment says that the demand for IMFL will mildly contract due to rise in prices.

- Progressive policy changes in UP, Jharkhand, MP ec.

- Royal Challenge American Pride(RCAP) entered the CSD channel.

- Double digit YoY growth for pocket pack of Royal Challenge.

- The company expects some volatility in glass prices in Oct, Nov this year due to planned furnace shutdowns by key suppliers in the country.

- There might be an increase in freight costs owing to glass factory shutdown as there will be cross regional sourcing(supply from other regions)

- The one off other costs is due to the legal disputes, bunching of some old cases etc of the last five years. This is a short term impact and will see normalization in the coming period. The company looks to neutralize this by some productivity changes.

- There was a 100 bps expansion in Gross margin as the company is migrating to PET.

- The benefit of import duty reduction should start flowing in from April- June next year as the company has a long pipeline of inventory.

- Outlets have doubled in Uttar Pradesh.

1 Like