Hello everyone. This is my first post on this forum. I hope

this post is on-topic. While this post isn’t about investing in

equities, which I think is what this forum is mostly about,

it’s closely connected. Apologies in advance, because this is

going to be verbose.

I’m trying to understand the differences between overnight

funds and a bank savings account or fixed deposit in terms of

safety. These are both common ways to park money for short

periods.

I know that overnight fund is a kind of debt fund where the

debt instruments mature overnight. But there are still a number

of things that are unclear to me about it.

My major concern is safety of the principal. But to determine

safety, it’s helpful to know exactly what is being done with

the money. As the saying goes: what you don’t know can hurt

you. And also, the devil is in the details. (The latter is a

saying I really like.)

Traditionally, the standard way in India to hold money is in a

savings account or FD. However, savings accounts/fixed deposits

in India are not safe. Indian deposit insurance is among the

lowest in the world. It was until recently 1 lakh per account,

and I believe that this has recently been increased to 5 lakhs

in light of the PMC debacle. This is in contrast to USD 250,000

for the USA, and Euro 100,000 for the EU. Also, my understanding is that in the case of bank failure, even this amount will not be made available immediately, but only once the bank is liquidated, which may take years.

Since deposit insurance is so grossly inadequate, in case a

bank runs into trouble, it needs to get help from the govt. But

cooperative banks fail all the time, and the govt does nothing

to help them. PMC is just the largest of such events, so made

the news in a way that the others did not. However, the govt

apparently sees nothing wrong with allowing thousands of unsafe

cooperative banks to continue functioning, nor does it try to

protect the public in any way from the possible consequences of

failure. For example, it has never, to my knowledge, ever

issued any safety warnings about banks. So an obvious defensive

ploy is to only keep money in banks that are large enough that

the govt will be compelled to bail it out. The so-called “To

Big To Fail” banks. I checked, and apparently SBI, HDFC, and

ICICI currently fall into that category. But it would be really

nice not to have to depend on a bail out in the event of a

problem.

In light of the above, the idea of an overnight fund seems

quite appealing. But it’s a good idea to take a long and hard

look at it first.

The article

is one of the few places where I found a discussion of

comparative risks. The author writes:

Unlike debt funds, the risk of concentration is high in

investments like fixed deposits where investors hold large

sums of money and run the risk of losing it all if things go

wrong. There is very little information available to

investors that they can use to evaluate their investments and

they have very few options for exit or redressal.

Open-ended funds, on the other hand, are required to provide

regular information on portfolio and performance to investors

and can exit at the current value of the units at any time.

So the author is saying that if one has an account with ICICI,

for example, all ones risk is concentrated in one bank/company.

It’s ironical he should mention information on portfolios,

because my question is largely about the overnight fund

portfolios.

https://www.sbimf.com/en-us/lists/sid_kim/sid%20-%20sbi%20overnight%20fund.pdf

In many places, overnight funds are mentioned as an alternative

to bank deposits (savings account or fixed deposit. But it’s

not clear to me how the respective risks compare. I’m also

still not clear what the risk of a overnight fund is,

exactly. It’s described in various places as “low risk”, but

I’m not sure what that translates to in concrete terms.

I know that debt funds in general list their portfolio, so one

should look at that for more details. However, looking at this

hasn’t been particularly enlightening. I looked at some

overnight funds (sample

list).

The SBI fund is the oldest, apparently having begun on October

01, 2002

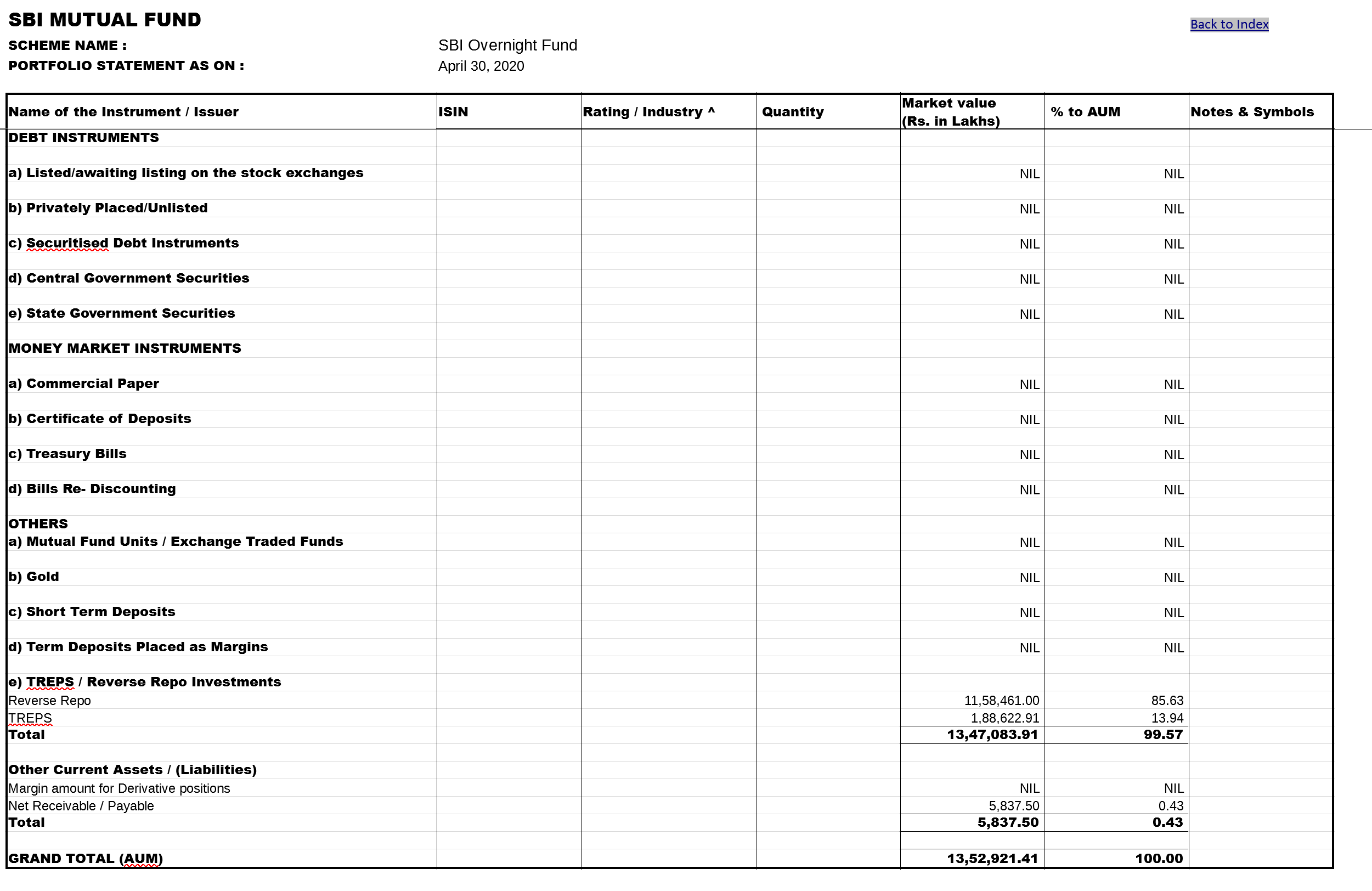

All the overnight fund portfolios I’ve looked at have the

following in various proportions, but nothing else: Reverse

Repo, Net Receivables, TREPS. Usually one of these three is

dominant.

For example, the SBI overnight funds breaks down as follows:

Reverse Repo (sometimes just Repo) 99.10%

Net Receivables 0.63%

TREPS 0.27%

I’m not completely sure what any of these terms mean. Here are

some guesses.

Reverse Repo/Repo: This is vague. Repo is short for repurchase

agreement. Repo and Reverse repo are general terms, but it’s

possible it is being used in a specific sense in this case. The

general sense is that some entity (possibly a central bank)

sells a bond to the overnight fund for an overnight people, and

then buys it back the next day at a higher price, i.e. the

original price plus interest. In other words, the entity is

borrowing money overnight from the overnight fund.

In this case, it’s possible that the entity is the RBI, but

this is just a guess. It might be others. And digging around in

the records of overnight funds revealed no additional

details. If the entity that the overnight fund is doing

business with is exclusively the RBI, then an obvious question

then is - is the RBI willing to sell as many bonds as the

overnight fund wants?

TREPS: This appears to correspond to something called a

Triparty Repo (FAQ - TREPS),

which is a repo contract using a third party as

intermediary. Would this third party hold collateral? It’s not

clear. It’s also not clear how this differs from Repo/Reverse

repo. Does Repo/Reverse repo not involve a third party?

I found the Wikipedia Article

helpful when trying to understand what repurchase agreements

are.

Net Receivables: I’m not currently sure what this is. But a

search bought up this question on tradingqna.com,

Net Receivables in Mutual Funds - #5 by Bhuvan - Personal finance - Trading Q&A by Zerodha - All your queries on trading and markets answered

but I didn’t find the answers there convincing.

Finally, this might be a dumb question, but what is stopping an

individual doing what these funds are doing?