I am still waiting for autonomous cars that were supposed to make drivers obsolete, this hype peaked a few years ago. Similar fate awaits open AI.

1 Like

As I mentioned earlier, P/E ratios of most of the IT stocks have reduced now close to their Fair Value.

TCS PE has corrected from 40 to 27.

Infosys PE has corrected from 38 to 22.

HCL TECH PE has corrected from 31 to 19.

To me, this looks close to Intrinsic Value of the stocks, based on Median P/E for the past 10+ years. Reversion to Mean has happened to a large extent.

We will now see most of the analysts talking negative about all these IT companies, and this will give an opportunity to long term IT investors to take major exposure to IT stocks.

Some further correction may happen in all these large cap IT stocks since weakness in North America and Europe markets will continue for 2-3 more quarters, as per my experience.

If an investor follows value investing approach, it mostly works in IT sector, as PE improvement also can happen once inflation in all the developed nations start falling, and also in India. Margins may also improve partially but real gains can come from sales and PAT improvement after few quarters.

Disclosure: This is not a recommendation or an advice. This is just based on my observations of IT sector over past 3 decades.

2 Likes

How relevant is the median PE in the context of IT, as the business of IT continues to evolve as new technologies are created, and as such, new clients, new requirements could bring in more profits, higher margins, so median PE does not apply and PE will be high compared to the past?

1 Like

I consider Median P/E important for an IT sector based on my investment experience in the sector since TCS IPO in 2004.

There have been instances when few IT stocks move from P/E of 15 to 30 based on momentum, only to fall back to P/E of 15 once the momentum is over. You can understand this trend in TechM stock during 2006 to 2020. Now it has become more resilient but still can go to P/E of 15 since TechM business is marginally risky business as compared to other Large Caps.

New clients and technology does keep evolving. Over a period margins start reducing as other companies also develop expertise in those technologies. Margins of few IT companies will be higher than others due to their premium charging to customers, either premium Fixed Price or premium Time & Material pricing. T&M is used only for less projects and Fixed price us used in most of the long term projects.

When IT company offers modern technology, initially it commands premium margins for those technologies, but slowly it moves towards more average margins of that company.

If ROCE of the IT company keeps improving, P/E gets elevated which is common with all industries, but it will remain within some range. This range can vary from company to company based on their ROCE, Operating Profit Margins, Consistency in Sales and PAT growth, Management Quality and IPR. TCS commands higher PE due to some of these parameters as compared to other large IT companies.

This is my personal view and I may be wrong in analysis.

2 Likes

For those of you, who think that a basket of IT stocks entry in SIP mode is better in comparison to selective stocks in large and midcap, the alternatives are IT BEES and 2 MFs (Tata Digital and ICICI Pru Tech…of the 2, my experience is Tata contains the downside a bit better (conservative) while ICICI is good, when the bulls resume control). There are others but this comes to my mind immediately (i am sure there must be smallcases of different varieties floating around for the basket too)

2 Likes

Instead of putting blindly in IT index or these mutual funds, is it not better to identify 2 good large cap and 2 good midcap IT companies and sit tight with it for long term?

1 Like

Here’s 2 cents from ChatGPT

As an AI language model, I can provide you with a list of major Indian IT companies whose customer base is primarily from the United States and whose order flow could be potentially disrupted by advancements in large language models and AI agents:

- Tata Consultancy Services (TCS)

- Infosys

- Wipro

- HCL Technologies

- Tech Mahindra

- Mindtree

- L&T Infotech

- Mphasis

- Cyient

- Hexaware Technologies

However, it’s important to note that while advancements in AI and language models have the potential to disrupt traditional IT services, these companies are also investing heavily in AI and related technologies to stay competitive and offer more advanced solutions to their clients.

A plumber with tools will eventually replace plumber without tools, but we will always need plumbers. AI will revolutionise IT but tend to overestimate the impact.

-

Only part of enterprise budget goes in greenfield projects. Trillions of lines of existing code will have no (or little) impact. We require humans to maintain the existing IT estate. Sure tooling is improving everything but patching existing code is not same as coding something ground up. Indian industry has major penetration here.

-

Software lifecycle is much bigger than coding/testing. The subjectivity of other phases require humans. You can have AI to find/fix technical defect but not say functional defects. Not anytime soon.

-

Coding/testing is much more than mere coding/testing. It is one thing to create 5 page web application, and another to write 500 page applications sitting on tons of existing systems. The architecture, the frameworks, the technology Infrastructure, there are tons of aspects, that humans decide.

I can go on and on. From web to mobility to cloud, Indian IT industry has only matured. This time may be different but not as different as we tend to believe.

9 Likes

Just to add on to @pahaaadi comment. Automation testing itself need human intervention. Basic code generation can be done thru AI but putting different logic as per client’s requirement is a different ball game. There is much more complicated scenario present which for now AI is not capable of. We will see in future how it shapes.

1 Like

The thread is again hijacked to AI discussion. Please keep the discussion related to investments only.

1 Like

Hi, I have a question for domain experts, which has more potential for growth over a 10 years period, if I am adding money monthly on a SIP basis, NIFTY IT, Midcap IT or FAANG ETF. I had been thinking of adding IT companies to my portfolio for a long time but failed to understand major differentiation among companies hence decided to go with FAANG etf.

Is there any midcap IT based etf?

If I am not looking for specific stocks and aiming at 15% return over 10 yrs, which index has more potential?

1 Like

There are IT based mutual.funds like Tata digital India Fund , Aditya birla digital.india fund…

Since companies in Large cap are just 3-4 most funds will have large cap and.midcap.together…

Dont think that any midcap IT fund exists

2 Likes

1 Like

Thanks for the help. If you’re asked to pick one out of them, what would you choose for a 10 year period, FAANG ETF / NIFTY IT ETF/ any IT Sectoral fund? (As of now I lack clarity in understanding moat of individual stocks)

Not from IT, and except for some very elementary idea, I don’t follow the sector much, nor have I invested for longer duration in these stocks, so take my view with some salt.

I am not sure if Indian IT and US IT stocks can be compared, particularly the FAANG, Microsoft etc. And I think if the R&D that happens does not happen as envisaged in these companies, there is no innovation, competition arises elsewhere, product failures, and if they are trading at high valuations, they will fall, along with the fact that the kind of shorting that happens with US stocks.

Indian IT more or less has the same large caps for the past many years, along with many mid caps, and new age tech companies in the past few years. So one can have a relatively easy view for Indian IT. Sectoral bets have to be taken with some understanding and basis, despite the sector looking like a secular SIP one. Maybe this could be looked at as a defensive sector, provided bought at decent valuations, with the dividends, it could bring some stability to the PF, if one is not into IT. 15% can happen, but as with any other stock, the ride could be a up an down one, and as there are many global factors that influence the sector, the downtime could be long.

I remember having Birla tech fund, also had a position in Nifty IT ETF, couldn’t invest more, so sold my positions, don’t have them now.

Again, not from IT, so could be wrong with some of the points.

3 Likes

@Akashdeep Everything is fair in L, W and Investing. So FAANG is ok but it’s risky, am not sure Faang etf via indian MF is available?. Instead you may consider NASDAQ 100 index Fund, able to invest in INR via Motilal, Kotak, Navi and many others.

Regating Indian IT - Index fund is not available. However Tata, AB, ICICI MF has tech fund which is better option. Even if index fund is available, the weight of top 5-7 will be more than 70% (numbers are appro) hence better to invest in tech MF than index fund.

2 Likes

Hi @Deven ji, thanks for helping. Mirae Asset NYSE FANG+ ETF is there, I have been adding money there since Jan as I was not sure on any domestic IT company

1 Like

Q2, 2023 economic growth in USA may be a good news for Indian IT industry in coming days

Not only S& P 500 companies have the highest growth of the century , even USA technology sector had excellent growth. ( pl refer 2nd link )

Discl : I remain invested in Indian IT. My investment in Mirae FAANG+ technology ETF given me 50% return over last 1 year.

This is not a buy or sell recommendation on IT … Please do your own assessment before investing

4 Likes

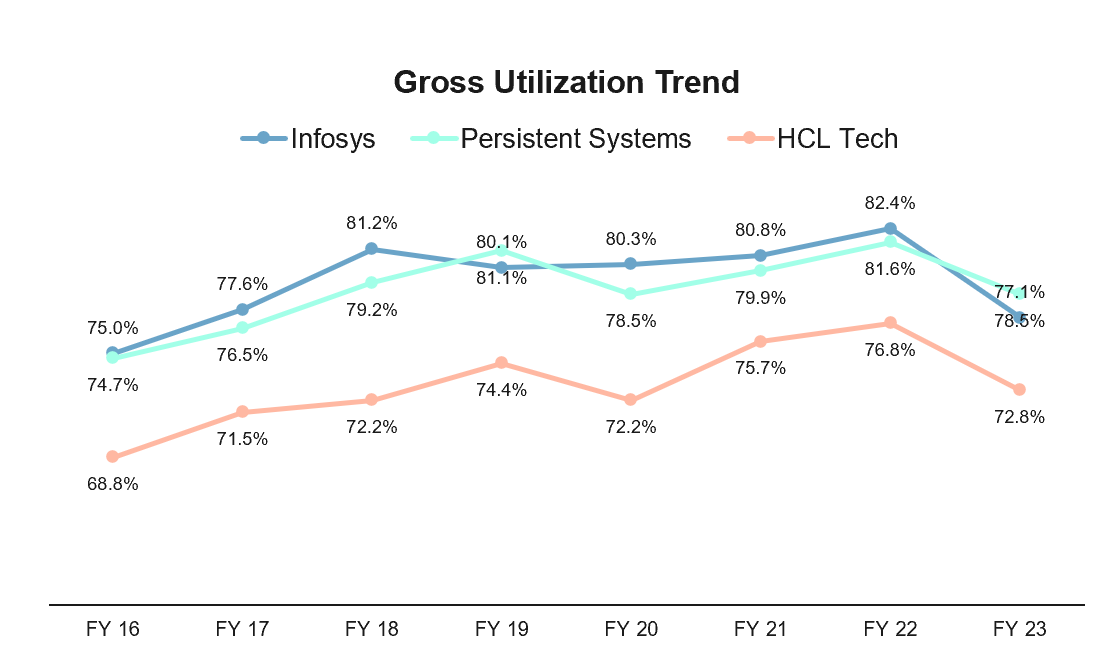

Hi there, here is a little history along with data points that may interest you.

Due to macro headwinds, during 2016 to 2019, demand led growth was limited. So, entire industry used resource utilization as the lever. Please see the chart to observe how employee utilization went up for all companies (TCS does not provide that data point, hence not included).

As utilizations went up from ~70% to ~80% there was limited room (called bench strength) to take on new large projects or internal R&D, etc.

However, with Covid-19 pandemic (which no one could foresee), the demand zoomed and the industry faced severe supply challenge. Therefore, the industry hired aggressively to meet massive demand during 2020 to 2022. I am not at all saying the managements are ill-willed, but taking care of employees during and post Covid was a business necessity.

On a side note, number of new hires was a leading indicator of growth of an IT service company during Covid times. However, now that demand has softened (see how utilizations have come down in the chart), the companies feel they’ve over-hired and are focusing on flattening the pyramid. They are letting senior managers go and hiring only at bottom levels. As a result, the hiring number is no longer relevant metric to assess growth of a company. I am working on a detailed write up on key factors of an IT services business. I will update here soon.

Hope it helps!

Mahesh

Let’s connect on Twitter ![]()

10 Likes

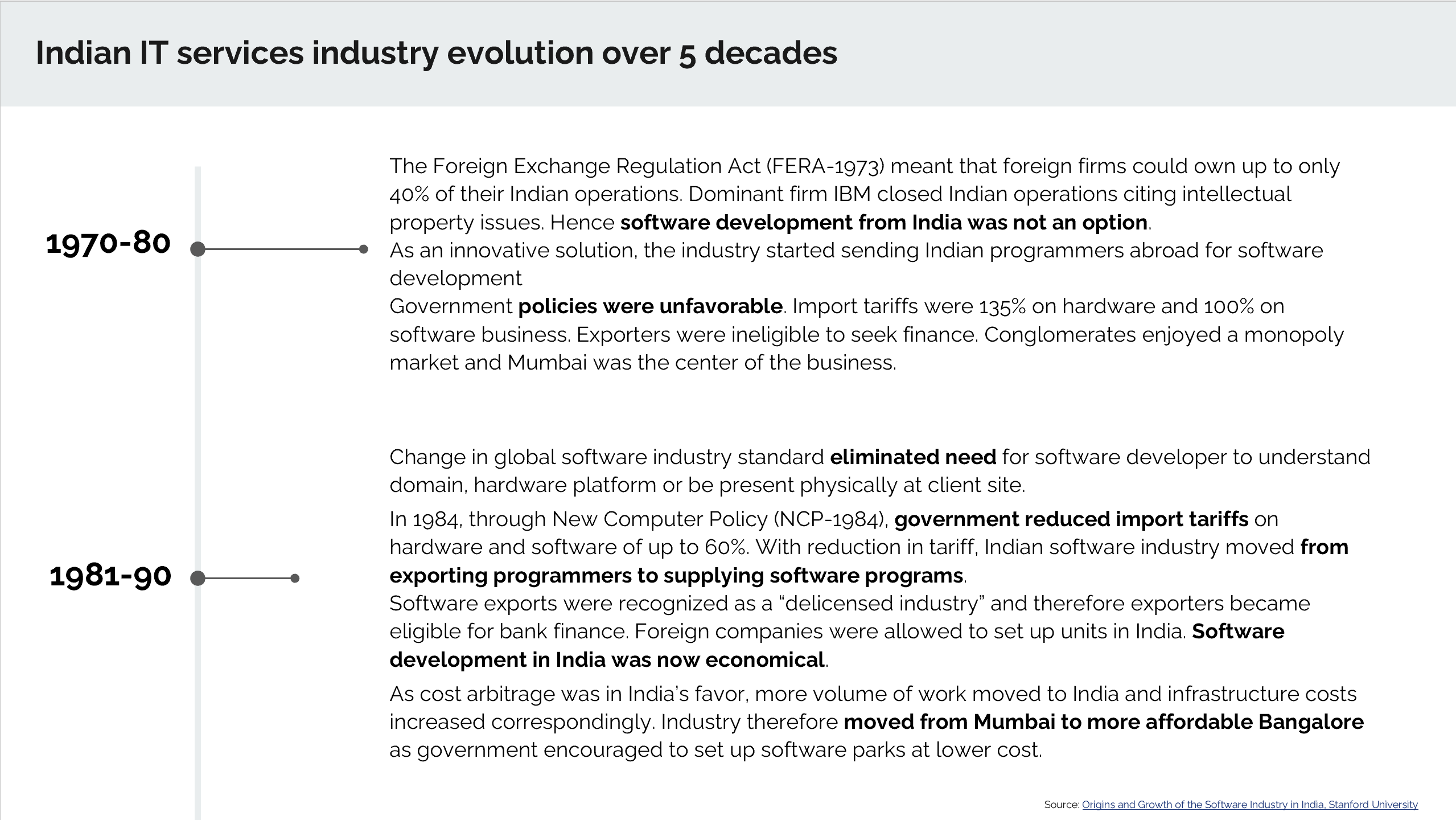

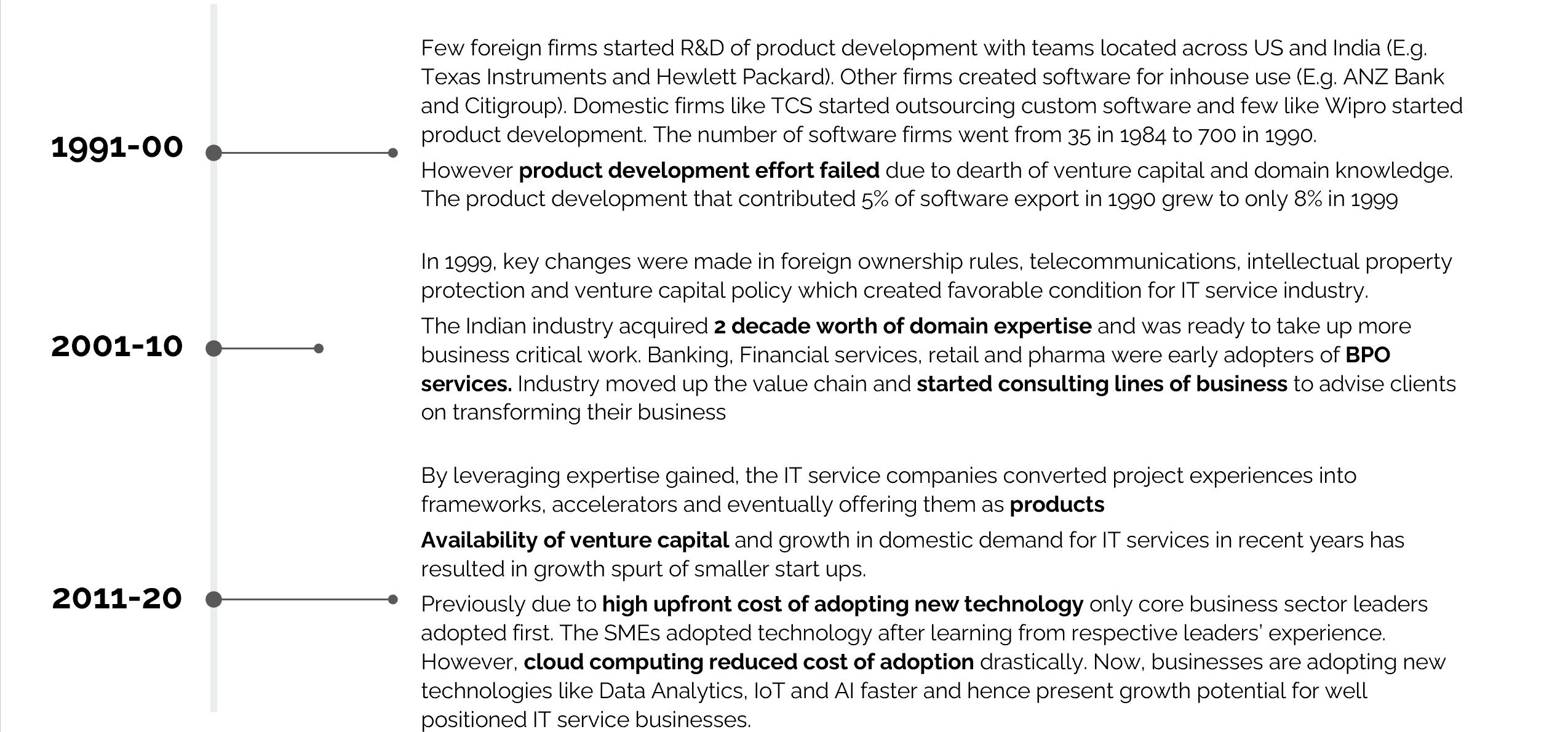

Prepared a short history of evolution of Indian IT sector. Request seniors to add any more nuances that I may not have captured.

Mahesh

Let’s connect on Twitter ![]()

6 Likes