Always thought IT sector had high PE since they’re asset light. Their major expenses will be employee expenses like salary, bonus, ESOP, ESPP, travel, visa, hotel bookings, etc.

When did they have 15+ PE?

Always thought IT sector had high PE since they’re asset light. Their major expenses will be employee expenses like salary, bonus, ESOP, ESPP, travel, visa, hotel bookings, etc.

When did they have 15+ PE?

5 Yr median PE of HCL is 15. Crème de la crème (tcs, info, etc.) which had 20+ pre covid are 25+ now. I am not considering the ER&D companies but pure IT play/services.

Bottom line is PEs of all companies are above their precovid levels.

@Patel_Bhai In my opinion going IT stocks should quote a bit higher than the pre-covid multiples for a few years to come. A few reasons.

a) Covid has meant outsourcing and remoting are more acceptable so the TAM has increased and this is irreversible.

b) The move to the cloud and SAAS platforms both of which offer significant cost savings has just started, so there will be increased growth for the next few years.

c) Covid has accelerated the digitalisation of business processes. This also leads to higher growth for a few years.

d) As companies grow bigger they benefit from economies of scale.

e) Cloud means even smaller companies can compete. Cost of offering SAAS platforms is greatly reduced and they is an equal playing field with majors such as IBM.

Traditionally IT stocks have Median P/E (10 Years) as below:

TechM: Median P/E - 17.7, Current P/E - 18.72

Infosys : Median P/E - 19.4, Current P/E - 27.5

HCL Tech : Median P/E - 16.3, Current P/E - 19.7

TCS : Median P/E - 24.6, Current P/E - 29.0

Except TCS, All large IT service companies have traded at P/E range of 15 to 20, over a period of 10 years.

From my experience of investing in IT stocks since 2004, there have been periods of bloated P/E(s) which last for few quarters and then P/E generally revert to mean.

From this perspective, I believe that, Fair P/E of most the companies except TCS should be below 20, and for some it could be even lower, based on their margins and ROE and ROCE.

Going forward, following are tailwinds for IT sector:

Headwinds:

Overall, it looks tough to take a call whether P/E reversion to mean will take little longer this time or not. An investor need to take calculated risk here, and prefer those IT stocks which have better margins, ROE and ROCE to be on safer side.

To me, valuations look rich except HCL Tech. TechM is low margin business hence my valuation band for TechM is lower than current P/E. Generally when P/E of the sector goes up, stories to justify higher P/E will be circulated but I do not believe much in those.

I may be wrong in my analysis.

Disc: Worked in IT industry for 25 years. Holding only HCL TECH now.

I do not track Wipro much hence not included in above list.

I think as new technologies are created, new verticals of revenue emerge, old verticals see a change both good and bad, and as everything about IT will be known to everyone quickly, the impact both good or bad will be determined easily, so if there has been a PE rerating across the board, it must be a structural shift, so if the current PEs are higher than the old PEs, maybe they will remain so. Of course there will be exceptions depending upon a company’s verticals, margins etc.

Have some exposure to IT, not from IT, just my thoughts.

As an investor into Indian IT since 2020 lows and adding on upside in 2022 crash…the question I would ask myself is that is the PE of 15-20 that they used to trade at justifiable?

P/E reversion to mean - this question would arise to me only if I believe that earlier PE of 15-20 was justifiable…

Good to know you are an industry veteran. I have been associated with Indian IT for significant time as well…and honestly in 2020 pandemic, I have been converted from a disbeliever to a believer…never invested in Indian IT before 2020, remember in 2015 when I had written off Indian IT considering emergence of new technologies across the globe…and now having seen the tremendous evolution of Indian IT in last 5-7 years and the way they navigated the pandemic - both with Customers & employees…one word comes to my mind…and that is…Magnificient!

Above may not necessarily result in a good investment but what I know is that prior to all this, the PE what the market considers as “mean” does not hold true for me…as I see no reason for such Magnificent companies command a PE of only 15-20…and if at all that “mean” still holds for the market, I would be a buyer at such “mean” PE because the “mean” for me has grown tremendously with the evolution I have closely observed…(I maybe wrong and any dip in growth/recession can bring PE to below this “mean” also)

Point to note here is that I am mostly invested into Mid-cap IT and hence track them more & interested in them as compared to large-cap IT. Hence all above PE discussion may not hold for large-cap IT and my argument may not hold true at all…

Disc: Invested hence highly biased. Not eligible for any recommendation. I can be completely wrong in all my assessments

Yes, you might be right.

As industry matures and evolve, P/E re-rating and de-rating both can happen.

It seems that, all those people which were pessimistic about IT have now become optimistic, which is good for sector valuation, and the same thing becomes risk as well for Value investors.

I invested in IT sector during 2008 crash and also during 2011 till 2018, and after that, mostly have booked profits, due to my conservative approach about IT sector valuations.

Every investor can have different understanding and that makes investing interesting. When some investors are Sellers, there will be Buyers as well. Only time will tell whether Buyers were correct or on the wrong side. As an investor, you should be optimistic.

Agree with @gsapte & @Investor_No_1. Like you guys I was the founder of a Healthcare IT company for 2 decades.

You both covered PE and other aspects in length.

Let me give you some data of stock returns and retail holdings

CAGR stock Returns for

HCL - 10 Y @ 21%; 3 Y @ 22%

Infosys - 10 Y @ 17%; 3 Y @ 25%

Similar for other large caps and better for many mid caps. Source: Screener.

Public & FII shareholding for

HCL public 5.5%, FII 18%

TCS public 5.8% vs FII 13.5%

In 10 yrs TCS gave return of 3.73x, Infy 3.76x and HCL 5.48x

Those return one got without any PE re-ratings, as indicated by gsapte PE of HCL 10 yrs vs now is 16.3 vs 19.7. with Dividend Y of 3.74% HCL is no brainer for me (check disclosure)

I have the same view - PE won’t go down much but the chances of getting the same return in 3,5,10 yrs are bright. - Data proves it.

Am feeling pains when a relative child working at TCS for 5 yrs, he and his father was holding Bob, ONGC etc but not TCS.

I was going through Diwali pick by 7-8 MF, only 2 have one IT share in each (One has TCS and other has LTTS). This is painful. It seems FII is taking advantage of the IT services sector where retail is left for looking for multibaggers in other sectors.

Disc: Invested in TCS, Infy, HCL, KPIT & LTTS since covid and before that. Currently IT services is 35-40% of PF. No recent transactions. Views are biased.

Thanks for your response. Would love to hear your views on LTI from long term (5 to 10 years) perspective?

Deven has done good analysis of Stock Price CAGR returns and it looks promising but in the hindsight.

If one can check these 10 year returns in March 2017, March 2018, March 2019, or even in March 2020, they would have been much lesser.

Let us take an example of Infosys.

March 2019 - 10 Yr Price CAGR - 13.35%

March 2018 - 10 Yr Price CAGR - 12.3%

March 2017 - 10 Yr Price CAGR - 7.5% (This was due to tough head winds in IT sector since 2015-2017)

The above date taken from screener clearly shows that till 2019 and also till 2020, IT sector has under performed most of the sectors like BFSI, Pharma, FMCG and many more.

So during such periods, why Retail investors should have invested in IT sector? There were large lay offs in almost all large IT companies post 2015-16, so how an investor will keep faith in such sector?

I believe that, looking at current returns based on inflated P/E ratios of TCS, Infosys, and few others is not the correct picture of IT industry performance. Till March 2020, large IT companies have given returns in line with NIFTY and not better than that, unless you have bought at low valuation and sell at high valuation.

HCL TECH is probably an exception where there is marginal P/E rating increase but CAGR gains are still better.

I still believe that, recent run up in Stock prices and PE ratios during 2021, are still on higher side and may not indicate correct picture. Post Covid, there are definitely more opportunities, but we need to see actual EPS growth. Are these companies growing at 20% or more to justify P/E of 27-29 in case of Infosys and TCS.

Infosys PAT CAGR is only 10% in past 10 years as per screener and P/E is 27.

TCS PAT CAGR is 14% in past 10 years as per screener and P/E is 29.2.

Are these high P/E ratios sustainable? If Yes, can we say that, these companies will grow much faster than past 10 years due to Cloud, Automation, 5G, IoT, SAAS, Digitization now? Are there sufficient evidences now that these companies can grow their EPS at 15%-20% rates?

I am doubtful on these parameters at least for large caps.

Mid Caps may able to grow at 15%-20%-25% PAT CAGR to justify their high valuations, but large caps may not.

I still believe that, reversion to mean generally happens if such high market expectations are not fulfilled by the sector.

Again, I may sound pessimistic, but on several occasions in the past, my pessimism has actually materialized.

To me entire IT sector looks overvalued expect few stocks like HCL TECH and TechM, and there could be few more. I do not track Mid Caps as of now but was invested in Tata Elxsi, and moved out in April 2022, when its P/E crossed 110!!

In nutshell, IT companies need to show lot of innovation, and grow faster to justify such high valuations…

Few bad quarters generally wipe out all the gains in the past few years, and then Price CAGR looks low. See TechM share correction during 2015. It corrected from 750 to 400 in few quarters after few bad results. It can happen with any company. So an investor like me will be very cautious to touch IT stocks at current valuations!! Mostly I am the Seller of IT stocks in 2020 & 2021 except HCL TECH.

Again, I may have got it wrong this time, and it may happen that, current high P/E rations of few companies may sustain for 4-5 years and then the whole thing will look very bright.

This is applicable to all sectors not just IT. And since IT is export oriented, weak dollar always helps them. Recession fear will cool the job mkt and hence attrition will get into control; employee cost is the major expenses for IT co.

All the above CAGR calculations are based on lumpsum investment in certain point of time. Is it possible to see XIRR which will do rupee-averaging? Is there a tool/website which can do that?

I respect your views however you specifically mentioned about infosys. Infy has company specific issues, specifically CG issues from 2017-2019. Just to mention Vishal Sikka resigned in August 2017.

Said so we have enough discussion and I rest my case…

Hi All,

10 Year price CAGR analysis for TCS is as below:

March 2017:14.92%

March 2018:20.75%

March 2019:29.82%

March 2020:15.01%

High returns in March 2018 & 2019 could be due to suppressed prices during March 2008 to March 2009. Excluding 2018 & 2019, which was on the low base of March 2008 and March 2009, when most of the stocks including IT were corrected, it is marginally better than NIFTY.

Hence, it seems that, in IT sector, you need to select stocks carefully. Entire IT pack may not perform well, but some specific IT companies may do well.

This is similar to all other sectors as well.

Entry and Exit points are also important in IT stocks.

Broadly it is secular sector but from time to time, it can throw surprises of low returns due to rupee appreciation (this happened in 2015 to 2017 to some extent), Visa issues (again during 2015-2017), Margin contraction and mass lay offs (2015 to 2017).

One need to be very careful with valuation of IT companies, and should not get carried away by stories which are floated around. Having worked in large IT companies myself, I am aware that, there is tendency of the managements to panic when margins drop by few basis points, and immediately lay offs start. This is one of the main reasons of low confidence of general public in IT companies and sector in my opinion.

Many people which work in IT industry also have some exposure to IT sector since they receive large ESOP(s). In spite of such large ESOP(s), Retail investment in the sector looks low. So one need to understand the risks involved in this sector.

I am just trying to be realistic about IT sector valuations. I will continue to study the sector further and if my views about valuations change, I will certainly write about it.

I would say, bang on! I used to think sometimes that why IT sector/companies are not highly valued like say FMCG even though their earnings have been pretty much predictable over long term and variables impacting them are not that great, neither any capex needs, although employee cost and investment in bench is there…

I used to think that major reason is possibility of big volatility in earnings, while that reason is still there but major reason for lack of confidence of investors, specially retail & even employees in general on IT companies is because of your bang on statement above…the management gets panicky & layoff starts…a company/sector which does not have strength to support employees during bad times is certainly not worthy of long term premium valuations…

One of the reason I became a believer in Indian IT is because I saw them supporting their employees in one of the worst times of the century…the Pandemic…

Now, I am confused about the reason for that support…was it because of the DNA of these companies/sector or because they could see huge growth & margin improvements ahead (less travel, WFH, more demand etc.)…

If the reason is second one, then I would rethink my thesis of these companies being “Mangnificient”. I would rather then call them ordinary with their better days around making them seem “Magnificient”…Thanks for this perspective and I am still thinking…

Just a few points that come to my mind. I could be totally wrong in some.

Agree with all your well thought over points…just one addition here…

Point to think is why does such thoughts of layoffs and stock freefall comes to mostly IT employees?

Would HUL employees also sell all their Esops regularly with same thought?

Recently got to know of some people getting Esops in IT division of some healthcare devices related MNC and that too it’s only listed in US, but they never think of layoff or stock free fall and selling because of any reason although that company’s stock has practically gone nowhere in last 10 years or more…they think of it as their retirement help…

What a difference of perspective between employees of similar profile but different industry…

Disc. Above thoughts only academic and I can be completely wrong in all my assessments

Less than 5% employees actually follow their company’s performance like an investor do. Most of them only see the stock price movements. Esops are immediate gain, the difference between allotted price and the price on the day it reaches their demat accounts. And I think esops are alloted with some discount (I’m not completely sure of discount). India listed company shares can be purchased anytime from market.

Disc: I work for a leading smartphone SoC making MNC listed in USA and I get ESPP and RSU. And our company has opened an demat account with Etrade with which we can only get these shares provided by Co. We cannot purchase even my own company share from mkt let alone other company’s shares. So even if I know the share price is at higher end / resistance level I won’t be able to sell now and buy later. I haven’t sold any share so far, I’m keeping it as my retirement fund just like the people you got to know. But all my colleagues have sold at least their ESPP. ESPP we get at a discount of 15% of either the start or end (current) price of the 6 months period. So there’s a minimum 15% profit if a person sells it on the day they get it.

Good discussion on ESOP(s).

ESOP(s) are generally given during specific time periods, and the employee exercising the ESOP has to pay perquisite tax based on the difference between CMP and ESOP price. This tax is as per the employee tax bracket.

Generally ESOP(s) are purchased by employees when this difference is high so that they can see some gains immediately. If they believe in company business and growth then certainly they hold these ESOP(s) for longer time-frame. But as an investor if the the CMP exceeds way beyond Intrinsic Value, then it makes sense to sell some ESOP shares and book profit. You need to think just as an investor in the business.

There will be situations when you may get share at CMP which is close to (ESOP Price + Perquisite Tax), then you can buy directly from Market instead of waiting for exercising ESOP(s). ESOP(s) have generally longer exercise period of 5 years, so you have to exercise ESOP(s) as per this schedule of 5 years.

Just thought of highlighting few points for understanding of all.

Is there any website where we can find Order Book of IT Companies? (And Non-IT if it exists)

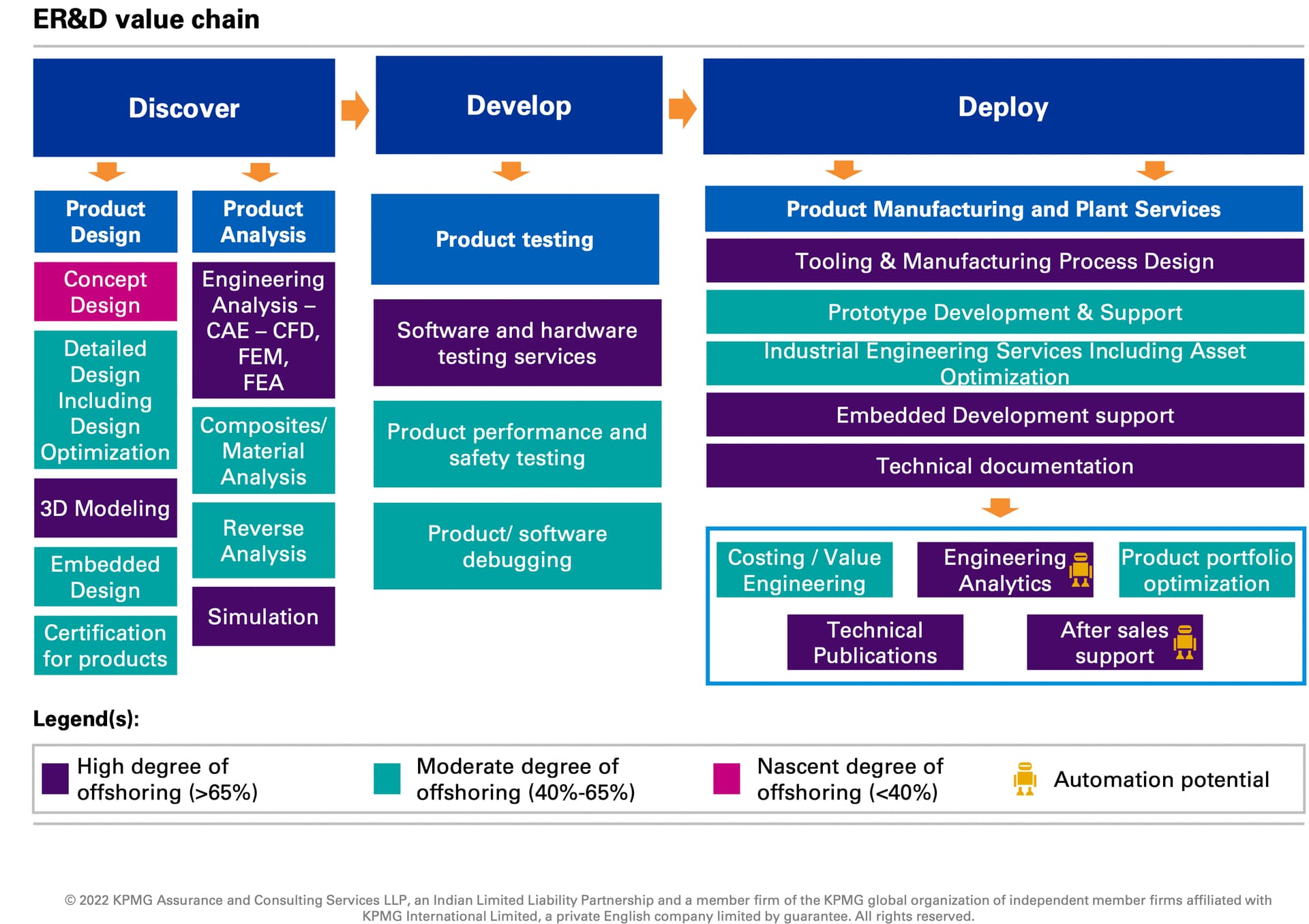

I often get asked about the difference between ER&D and IT services, especially from investor friends, who want to dig deeper into LTTS, Elxsi, etc. Here is my attempt to simplify it (Disclaimer: I am not from ER&D). Hope this helps someone.

IT Services vs ER&D

Let’s compare TCS (IT Services) and Tata Elxsi (ER&D) from the house of Tatas. BFSI, the top business vertical of TCS contributed 39% to its revenue in 2022. Elxsi on the other hand got 36% of its revenue from the transportation vertical. TCS caters to the transportation industry too. It has verticals like Transportation, Manufacturing, IoT etc.

So does it mean TCS and Elxsi are doing a different kinds of work within the same industry?

Well, not necessarily. Google “TCS connected vehicles” and you would get a thousand results. One would expect this to be a core capability in Elxsi.

What’s the difference then?

Let’s take the example of “Connected vehicles”. Connected vehicle = Some semiconductor chips and software that make a vehicle smart, and communication (e.g. Phone to Car, Cloud to Car, Car to Car) make it smarter. Plus tons of applications being built on top.

TCS may approach a connected vehicle ecosystem, from say Insurance sector (usage-based insurance, search term = “TCS Digital Insurance Telematics solution”) or a digital platform for OEMs (search term = " TCS Autoscape"). Outside-In approach of sorts.

Elxsi on the other hand, wouldn’t have started from the adjacent industries. It would start from the vehicle, and its architecture (mechanical, hardware, software) and then go outwards.

TCS may not go deep into the core of the car. Similarly, Elxsi may not build competencies around the insurance industry, and say evolving self-driving regulations across geographies.

There is no “planned” meet-in-the-middle strategy here either, by the two entities. In the hyperconnected world of technologies, boundaries are only getting blurred. Even within one organization, different business units step on each other. What varies is the frame of reference. DNA of TCS is to build software applications, say a bank’s portal & backend platform, digital channels for a hospital etc. For Elxsi it is more than just software which puts in the category called “ER&D”.

So what is ER&D?

There isn’t any textbook definition of ER&D. The two parts “Engineering” and “R&D” do not help narrow down its meaning either.

Engineering has tons of specialized branches and sub-branches. ER&D for the most part go with the traditional meaning of “engineering”. It focuses on tangible products e.g. automotive, aerospace, defense, industrial machinery, and so on.

R&D- We kinda know what it means.

So in layman terms, ER&D is the use of science and mathematics in solving engineering problems. But here is what makes it interesting. Engineers nowadays don’t design their products on pieces of paper (remember blueprints?) and then test them on the field. Well, for the most part. As computers became mainstream, software-based tools evolved. You design a car-part using CAD (computed Aided Design) software and test the design with FEM (Finite Method analysis) software, for various loads, vibrations, temperatures etc. And you do all this sitting in front of your computer, without actually manufacturing it.

And, why stop designing a piece of metal? How about adding a few chips, sensors, and software to it, and call it “connected XYZ”. You know where I am going with this. Extended that to other industries - Healthcare, defense, manufacturing, aerospace, appliances, semi-conductors, and opportunity size become huge.

The kind of skills required are different (or additional) to the regular IT skills like UI/Mobile app, back-end dev with various programming languages. Domain knowledge becomes important. Say someone with Mech engg degree, an understanding of the tools (e.g. CAD/FEM/FEA. Usually taught these days ) can qualify to join ER&D. Add to that AI, ML, IoT, 5G, Cloud, and other evolving fields and it becomes more exciting.

Here’s an interesting value chain of ER&D (Source: KPMG/NASSCOM) with respect to offshoring, where companies like Tata Elxsi, LTTS, Axiscades etc focus on.

Hope this helps a few here. I will expand on the industry structure in the future, but next time someone says ER&D, just think of software used to virtually design/test something which is physical. OR software abstracting hardware/sensors abstracting some mechanical components.