In case of Tech M a major chunk of their revenues come from BPO arm.

In case of Wipro execution seems to an issue.

In case of Tech M a major chunk of their revenues come from BPO arm.

In case of Wipro execution seems to an issue.

In recession environment, the offshore spends on AI, machine learning etc (all the cool projects usually) might actually reduce as short term focus of many companies would shift to profitability. Hence I feel Happiest minds etc have currently corrected much more due to fear of recession.

Some experts are giving the opposite reasoning. Since during recession, companies are focussing more on cost-cutting, hence automation and AI implementation will rather increase and hence business of IT.

You might recall that during 2016-2017, all experts were saying that IT sector will go down and companies will eventually go loss-making…But what we see in last 2 years, the sector was the biggest performer , thanks to covid etc.

Wipro lost the game a very long time ago. They did multiple mistakes in acquisitions which did not integrate well with their culture. They also experimented a lot with CEOs (joint as well as a couple from BPO sector which was not their core strength) and none of them were able to turn around the company. This used to be a company that generated a lot of future leaders who went on to become CEOs of startups and MNCs but has now turned to an expat CEO to turn around its fortunes. There is lot of fat even now in the middle and senior management layer and is one of the reasons I quit Wipro a decade ago. I don’t see any drastic change since then. The only positive about Wipro is the cash, regular dividends, integrity of its high profile Ex-Chairman Mr. Premji and debt free nature.

I still prefer TCS (Agility, low cost, low attrition, low risk appetite), HCL (ERD space is growing fast, aggressive management which complements) and TechM (Telecom)

Yes but in reality, any listed company would avoid layoffs currently to avoid media attention and cost cutting usually would start from offshore projects.

Yes automation would continue but there are lots of so-called cool projects which will take a backseat for now, in my opinion. And even in important automation projects, clients will push for more efficiency (lesser resources in project, faster turnaround), putting further pressure on margins and margins are already being impacted due to resources constraints and higher attrition rate

Personally feel there is some more pain left in IT sector as leverage play enjoyed by many IT companies continue to weaken.

Gentlemen, any feedback on Zensar Technologies? No new posts on forum’s company thread. The past performance is obviously not good and hence the cheap valuations. But since there is new CEO and few business vertical hires, so I think this would be interesting.

The stock price is 52 W low and PE stands at 13. Would the current valuations not protect from further down side?

“One of the report’s findings was that a lack of quality management or leadership is a major factor in higher employee disengagement and that 20-22 lakh employees are expected to leave their jobs by 2025…”

“…The survey indicated that 57 percent of IT professionals would not consider returning to the IT services sector in the future.

According to the report, one of the most common misconceptions is that increasing salary or perks is the only way to improve job performance. While employees will accept a pay increase, employee needs and priorities have changed, such as the desire for flexibility, career growth, and employee value proposition. Employees are reevaluating their jobs on these grounds and quitting well-cushioned jobs, the report said.

“With the usual demand for salary hikes and other benefits, the main attraction for employees in their new jobs is ‘Great Reflection’ on the internal policies and external factors that should be relooked at by employers as we are viewing great changes in the employees’ feelings about work and life,” he said.”

IT services attrition at 25.2% for 2022, troubles to continue: Teamlease report (moneycontrol.com)

57% of total IT workforce is a huge number. While I have no doubt that such number may be wanting or planning to quit IT sector for good (as per the post above) but if they really do, which other sector is employable for so many people of this background unless majority of them become self employed, which sounds desirable but is it really possible?

Hi All,

I would add few points here:

In IT services, though most of the companies do similar work more or less, the pricing power varies from company to company. TCS has always maintained OPM of 26% to 28% post 2015, where as TechM has maintained OPM of 15% to 18% post 2015. This is partially due to large portion of TechM work being Maintenance & Support and BPO apart from some Development, Design and Automation work.

Due to this difference, TCS may trade between P/E of 20-35 but TechM may find it difficult to fetch P/E of more than 20.

TechM has traded even at P/E of 11-15 for most of the time during past decade. There have been large acquisitions by TechM in the past which has impacted their margins severely.

I will prefer TCS & Infosys only in IT services space as a part of long term portfolio, and other IT services companies are good for short term holding only (2-3 years). This is my personal opinion.

I believe this article just creating the sensation. Being in IT for 15 year, I know everybody talk about leaving the job, but at the end probably 1-2% people do it. That is because of good salary in IT which they cannot obtain in some other sector immediately. Also other skill need to be garnered which is also difficult while working in IT. So I don’t see this is not even as concern.

Disc: Invested in TCS,INFY and HCL TECH. Left IT recently after 15 year.

I also hold TCS and Infosys in my Portfolio. What are your views on LTI, HCL texh and Tata Elxsi? And do they fit innyour category of short term holding of 2 years?

Hi Mudit,

I am not holding LTI so no views on that as of now. Though it is a high growth story.

I was holding Tata Elxsi, since late 2019, and added little more during April 2020, but my position size was small. After about 900% up move in stock price, I decided to exit mainly due to over valuations. Having said this, it is niche business and one can hold it for long term based on your temperament. P/E of above 100 this year was looking too high for me hence booked profit.

I am holding HCL Tech since past six months, so I am holding it due to reasonable valuations of P/E of close to 18. I was not able to buy it earlier during April 2020, but decided to buy it in this year 2022, with moderate expectations. HCL Tech seems to have focused more on their Products & Platforms business and it is some thing which looks good to me. ERD revenue is growing better which is high margin business. I am not expecting it to be a multi bagger or 20% Price CAGR story, but mainly holding it for good dividend yield and reasonable valuations. Most of my investments are from 3-4 years perspective, including HCL Tech. Now I believe lot of patience will be required as tail winds of 2020-21 are over. Now EPS growth will be mainly in lower range like during 2017-2019, as per my opinion. Rupee depreciation will be one of the positives but to a limited extent.

Disc Holding HCL Tech only. There could be better options like LTI, LTTS and others but I am not holding those. I have worked in IT sector for about 24+ years.

Thanks for your views. And its really amazing that you could ride 9 bagger on Tata Elxsi. And you are right…in next 1 year atleast patience will get tested. Hope we all stick to our stocks innthese testing times.

TCS result is out

Re Rev 55,309 Cr Vs Est Rs 54905

EBIT at Rs 13279 Vs Est Rs 13079 cr

EBIT 24% Vs Est 23.8%

PAT 10431 Cr Vs Estimate of Rs 10248

Dividend 8/Sh

Ref: Twitter person named as Sumit Mehrotra (I don’t know him).

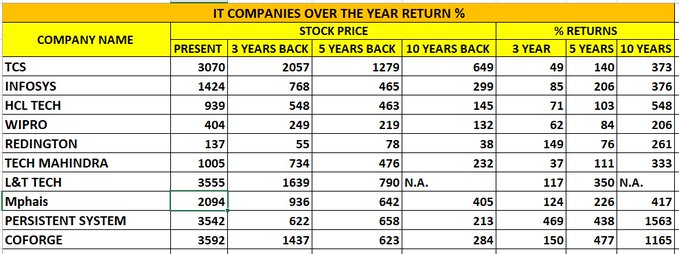

Stock returns are good for for 3/5/10 years even after recent brutlity.

Also as per Ramdev A IT services in 2001: 1% of corporate profit of all companies of India which is in 2021: 24%.

Disc: Though we discussed data only, am invested heavily in IT services hence my views are biased.

esds are providers of webspace to small businesses similar to godaddy. Mid and large businesses use cloud services or their own server.

As per my knowledge listed IT services had tie up with Amazon web services, Azure from microsoft and google cloud. Webspace providers are like commodities and scale is too small for listed IT companies in the same space as esds. HCL deals in server etc (Hardware) which those companies use.

esds has plans to list in sme ipo sometime back - don’t know recent progress.

Even after recent corrections in IT stocks, nearly most of the famous names are still quoting 20+ PE as compared to 15+ PE pre covid.

So wanted to understand whether those stocks are re-rated and 20+ PE is now the norm or can we expect mean reversion to PE of 15?