I am trying to understand deferred taxes and deferred tax treatment better. While I understand the concept of deferred taxes, I find it hard to relate to how it shows up in the P&L. I didn’t find any specific topic here that addresses this in detail, so thought I would start a thread, and maybe we can share examples of deferred taxes from P&L statements that are unusual or interesting, and get better informed about the kind of liabilities that show up here and when/how they are reversed. Hoping this can then become a thread that has a good collection of such examples.

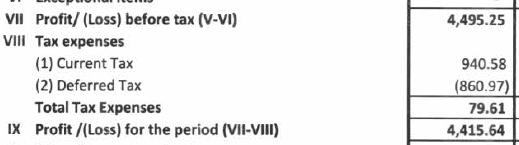

Here’s one example I would like to start with which I am not clear about. This is from the latest results of La Opala (Q3 FY24). There’s a deferred tax reversal of about Rs. 8.6 crores that has boosted their PAT.

When I looked at the notes, here’s what it says “Deferred tax liability reversal during the quarter/nine months period ending December 31 2023 is mainly on account of change in status of certain investments held by the company, i.e. from Short Term to Long Term as per the provisions of Income Tax Act 1961.”

Can someone who understands this topic well explain this (maybe with an example)? Is this like some equity investments for which they had originally provided deferred tax liability at 15% (short term) and have now changed it 10% (long term)? If so, when is it provided for originally? Can it be something else? Thank you!

Hope this is the right category for this post. If not, request the moderators to assign to the right category.

No intention to bump this thread up, but popped up in unread threads and seems something valid worth answering and interested to remind myself. Companies, maintain two P&L always, one supposed to be filed to the Tax Authorities (where mostly revenue recognition differences, tax deductions, depreciation method etc. causes difference from the 2nd one) and One for Financial Reporting which is issued to the general public and Share holders. The purpose is to ensure that the company abide by the tax rules while reporting their Income and the Financial reporting standards are followed for Financial reporting. (Such as ‘Indian Accounting Standards (Ind-AS)’ and IFRS or US GAAP).

These two normally will have temporary differences in Tax reported (sometimes permanent differences too), since some of the revenue/loss recognized can not be reported at the same time in both (due to points mentioned earlier). Hence Financial Reporting Statements will have Tax Liability or Assets that gets reported in the Balance sheet. Later on, these get reversed through P&L adjustments.

Hope the following will give further clarity on the entry shown in the P&L of LaOpala.

A reversal of Tax liability occurs when the circumstances that initially caused the deferred tax liability no longer exist or change, reducing or eliminating the liability. In the above case, the reversal is related to the change in the status of certain investments from short-term to long-term.

Reclassification of Investments leading to the Reversal: When the company reclassified its investments from short-term to long-term, the tax implications changed (We have higher tax rate for Short-term Inv., vs Long term). Normally, long-term investments have benefit from favorable capital gains tax rates, or timing differences related to their treatment may no longer be relevant.

This reclassification must have reduced the future taxable gains (or delayed their realization), meaning that the deferred tax liability set aside earlier is no longer required or needs to be reduced.

Thank you for answering this! I had forgotten about it

If I understand you correctly, it is only the change in the value of the deferred tax that is recognized in the P&L, i.e. when the deferred tax liability was first recorded in the balance sheet as a long term/short term liability, there was no “deferred tax” P&L entry as such. Rather when it originally entered the balance sheet as a “deferred tax liability”, there was also an equivalent “tax/estimated tax” that was deducted from PBT. Now since more tax was deducted in the P&L then (maybe 2 quarters prior), it has to be reversed now since that much tax is actually not going to be paid.

Is that correct or is my understanding wrong? Not an accountant, so some of this is a bit hard for me to grasp.

You are almost there; but your assumption is not correct. Let me try to put it this way; Imagine, a company has 100Cr as PBT (Profit before Tax), in the Financial statement (FS), and assuming a 20% tax rate, they show 20Cr as taxes paid (in FS). Note: this 100cr also include a 50cr from a marketable security or some other investment which has ‘unrealized gain’ of 50Cr.

However, their Tax reporting statement shows total Profit for the period as 50 Cr (for tax purposes, the gain is not recognized until the investment is sold and the gain is realized). Here then the tax actually paid is 10 Cr (20% of 50Cr).

So, company will create a tax liability of 10Cr (since your cash a/c still holds a 10Cr, which has to be paid to the tax authorities in a future date).

The scenario here, has an impact of entry in P&L (entered 20Cr as tax in FS), while in reality not paid to authorities…, and surely it will hit in future.

Hope i havent confused you further here…

PS: One take away point i would add here is, one has to pay bit more attention when we see a significant amount hits P&L under deferred tax Asset/liability. Lets say as a % of PBT.

Right - that’s what I meant actually (difference in entry between FS and tax reporting statement), probably didn’t articulate it clearly enough. This explanation made it clearer. Thanks again.