What is the market share of Ultramarine and Pigments?

Who are the main competition to this company?

Whether the surfactants and pigments are manufactured in the same company in Ranipet. If no, what is the capacity utilization of pigments company

Does not the have any specific moat.

Are the surfactants or pigments business dependent on Crude oil price

I understand that there is an increased demand for all chemical companies following the increased government regulations in China.Please go through this thread Change in Chemical Industry dynamics

Hence was going through few chemical companies and found this interesting given the high ROCE

Good Judgement @harshitgoel on - the new 70 cr plant could add approx 70 to 80 % new capacity based on existing gross block

However we still do not know the surfactant to pigment precise division. I guess it would be more towards surfactant based on their existing business.

Do anyone have any idea if china chemical ban has helped boost ultramarine with their margin? And if so should we factor any future margin deterioration based on it??

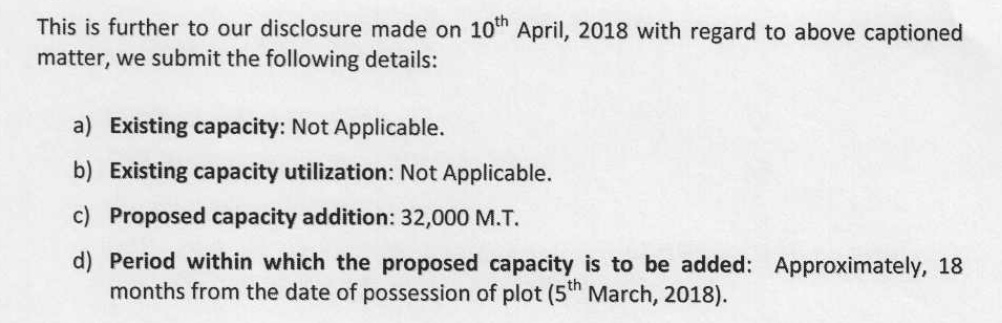

The capex is for surfactant and not pigments, See excerpts from annual report, "Your company is setting up a greenfield surfactants project with an annual installed capacity of 30,000 Tonnes in Naidupeta, Andhra Pradesh. The estimated project capital outlay for the same is approximately ` 70 Crores. The Company will contribute one third of the planned capital outlay out of surplus funds and the balance by way of a term loan. We expect to commence commercial production by third quarter, 2019.

The annual report says third quarter, 2019. So this could be 3QCY19 or 3QFY19. I guess safer to assume 3QCY19 which is next year September to December 2019 instead of 3QFY19 which would mean in the current quarter

hi Venkatesh,

THanks for the break down sheet.

Would you know what kind of It & ITEs, BPO services the company offers. I have not been able to get details in the AR.

This is application for EC, the company is yet to receive EC, thus it seems that the new plant commissioning shall be delayed and not happen before December 2019. The conpany guided for 12 months from the date of obtaining EC.

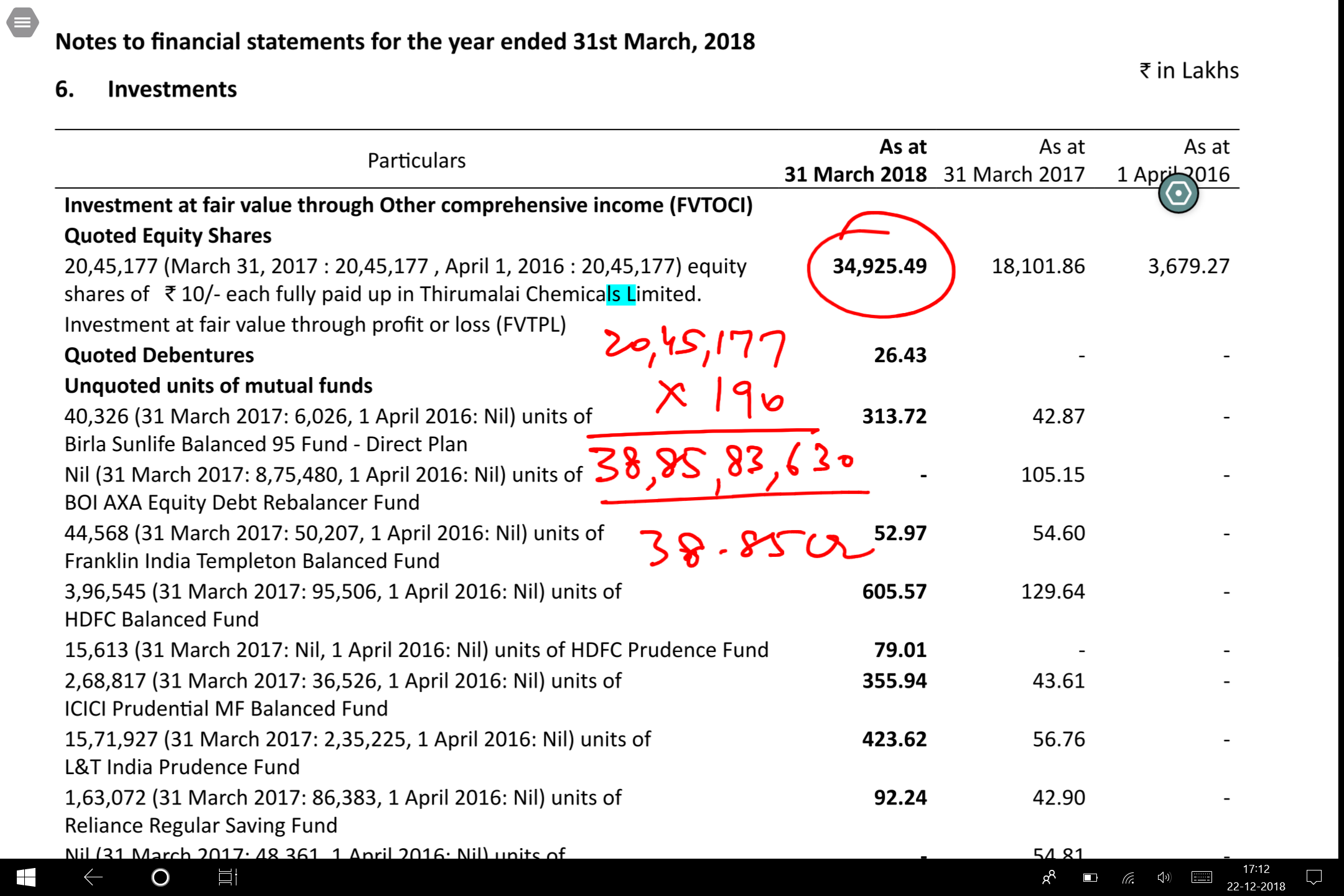

The market value of investment in Thirumalai Chemicals Ltd.

As per my calculation it is ~38 crores. But in the company books it is shown as over 300 crores. Am i missing something.

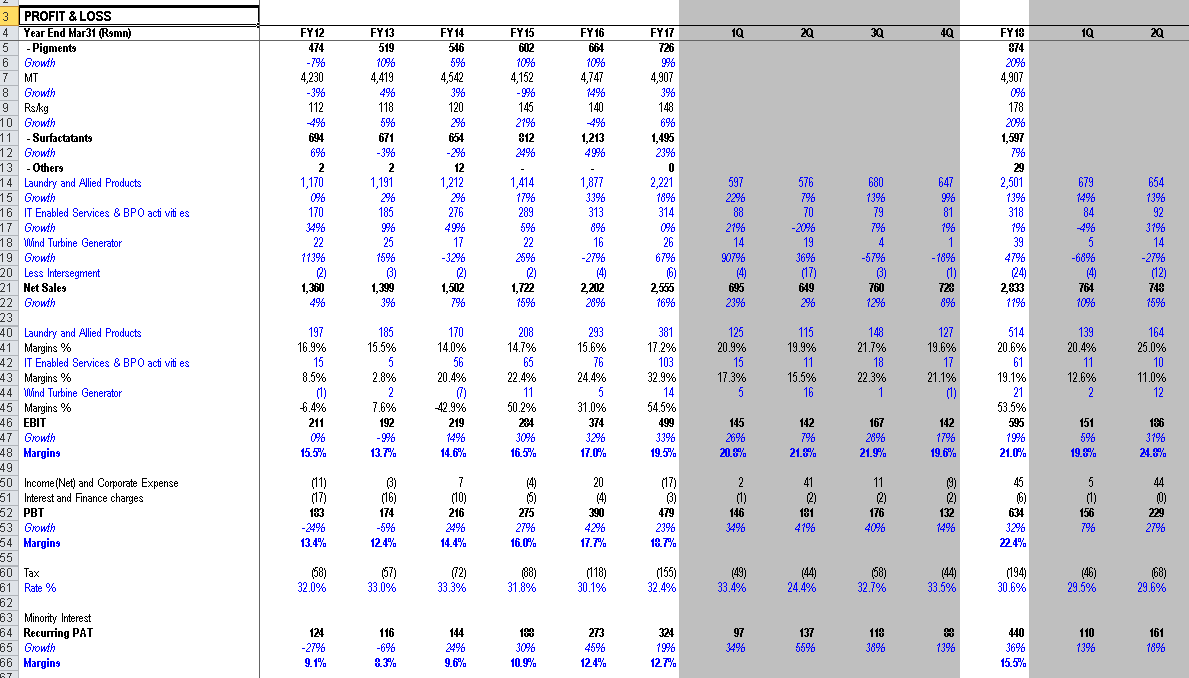

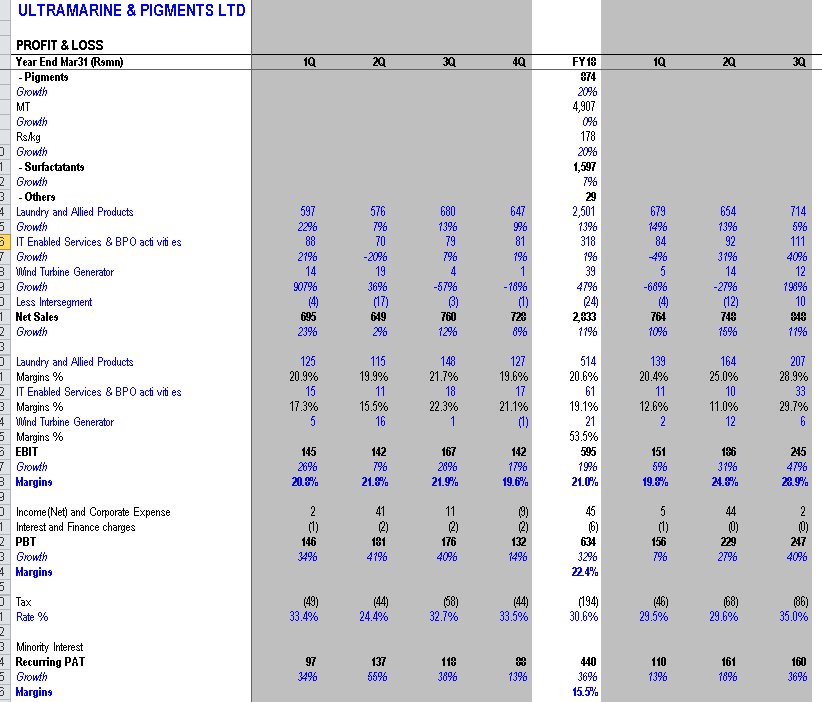

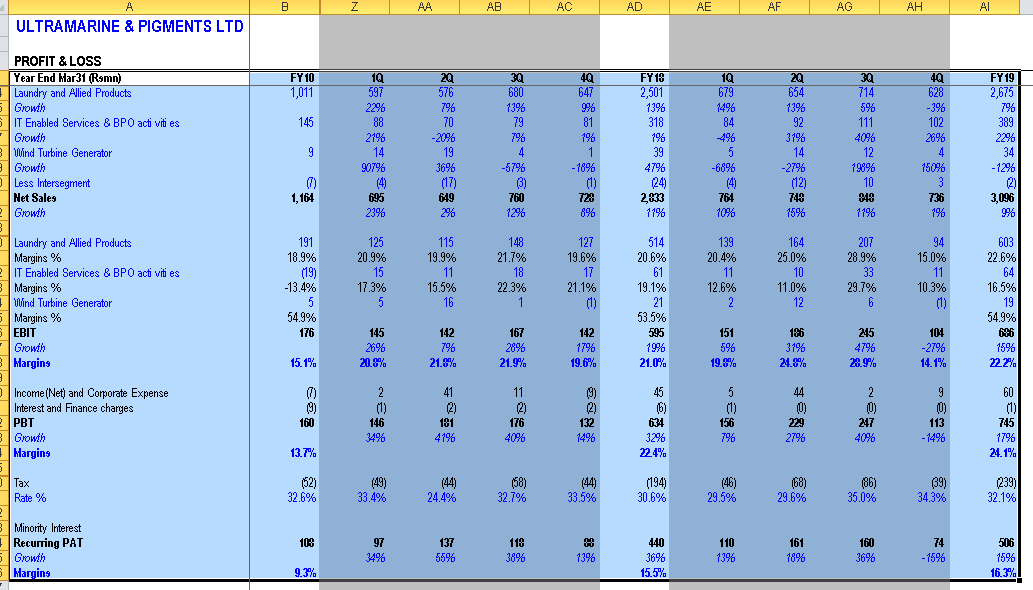

Ultramarine had a not so great 4Q19. PAT declined 14% YoY. However despite this FY19 PAT was up 17% YoY. Dont know if 4Q is an aberration or start of a trend?

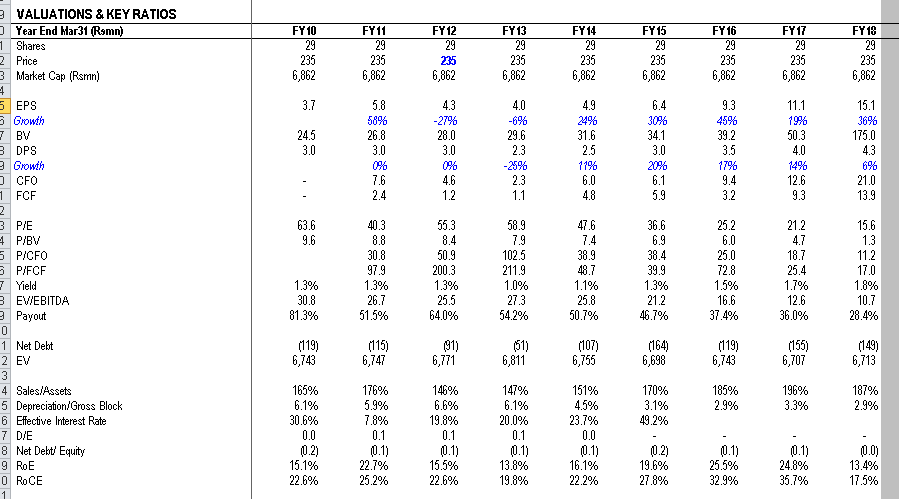

Stock has corrected sharply. **At Rs209 stock at 12.1x trailing FY19 P/E.

As per the information available, the EC has been granted for the proposed expansion project (cost Rs. 80Cr) and construction works were supposed to start.

However, in spite of trying several times, couldnt contact the co.

If you look at fy18 balance sheet …investment value was 400 crs, for fy19 investments are at 221 crs. This is mainly due to drop in share price of thirumalai chemicals.

For the year they have sold some investments…which is reflecting as other income.

Overall sales are flat. Next growth in sales likely after q3 after completing CapEx of 70crs which is likely in q3.

There is drop in margin this quarter. If you look historically, company has had 17% margin. Only last 2 years margins had shot up to 22-23%, I feel last 2 years margins are not sustainable. We might go back to 17-18% margin.

I think margins have returned to normalcy this quarter. 17-18% margin likely going forward.

We should analysis the company based on 2 things.

A)keeping margins at 17%

B) based on their investments. (Since they hold 20% of thirumalai , tracking thirumalai performance is a must)