Here are some brief notes on the result and also some events which influence the MFI sector.

What went haywire in the MFI sector?

- Lending to over-leveraged borrowers

- Debt waiver campaigns

- High attrition rates among field staff

- Challenges in debt collection due to extreme weather and elections.

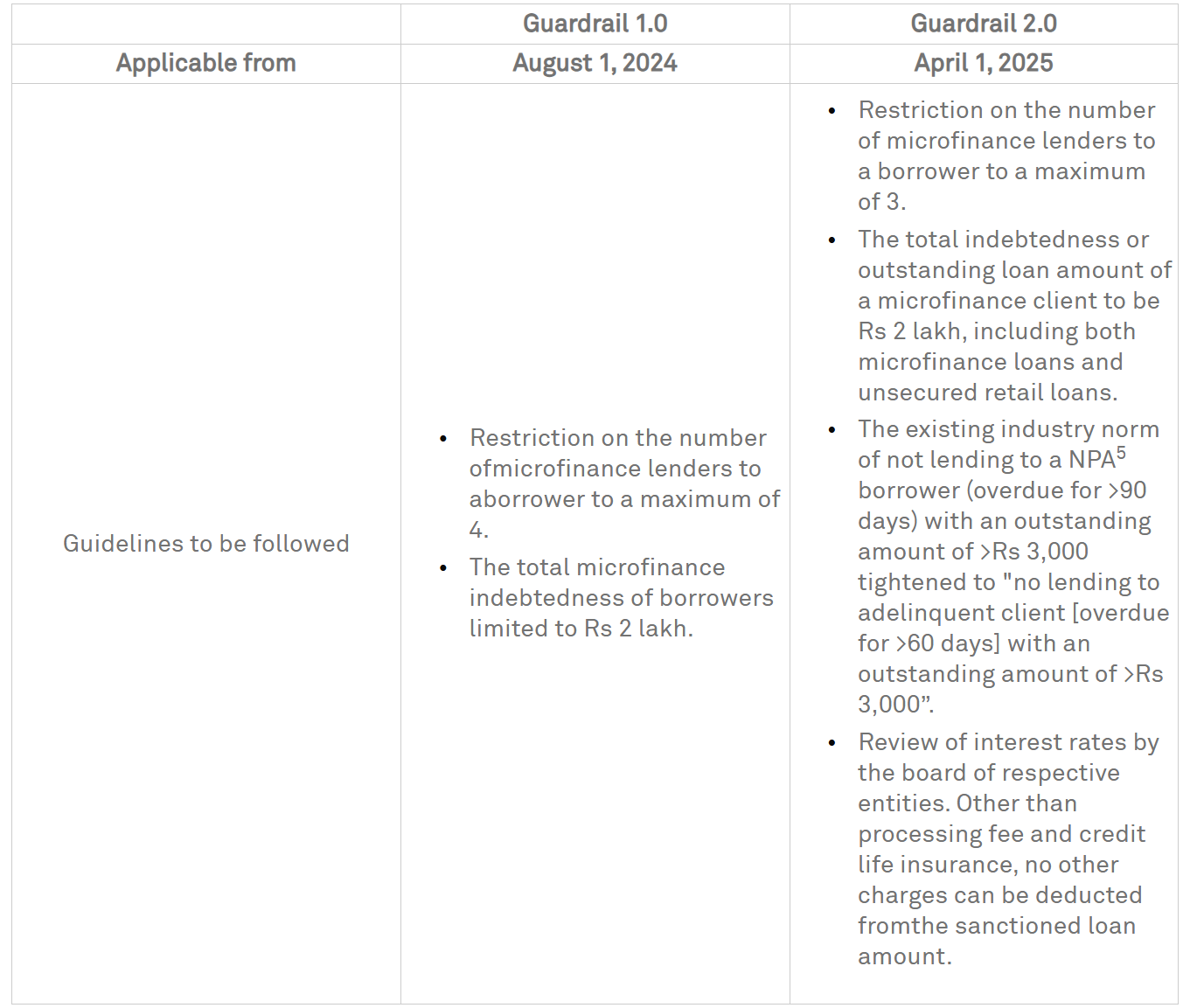

Guardrails

Introduced by MFIN (first Self Regulatory Organisation aka SRO in India)

Overall this has lead to less stress in the sector, improved collection efficiency and has decreased the credit cost. However, it also means there can be compression in NIMs due to higher rejection rates.

A glimpse into the Karnataka issue

- Vulnerability of borrowers, cross-selling and opacity of terms, unjustified/usurious rates of interest, multiple loan facilities and coercive methods of recovery etc. had lead to suicides and public outrage.

- The government of Karnataka has come up with an Ordinance to protect borrowers against such practices.

- Even though RBI - licensed banks and NBFC-MFI are exempted, this has lead to lower collection efficiency in the state and increase in delinquencies

- Borrowers cite the law and lack of clarity to delay repayments

- Further disbursal has been reduced due to lack of clarity related to registrations and other requirements of the ordinance

More Readings:

- Microfinance Crackdown: Key Features of Karnataka’s New Ordinance - Lexology

- Karnataka Micro Loan, and Small Loan Ordinance, 2025 – Vinod Kothari Consultants

Tamil Nadu has recently passed a similar ordinance:

Analysts warn Tamil Nadu MFI lenders may face strain, cite Karnataka fallout

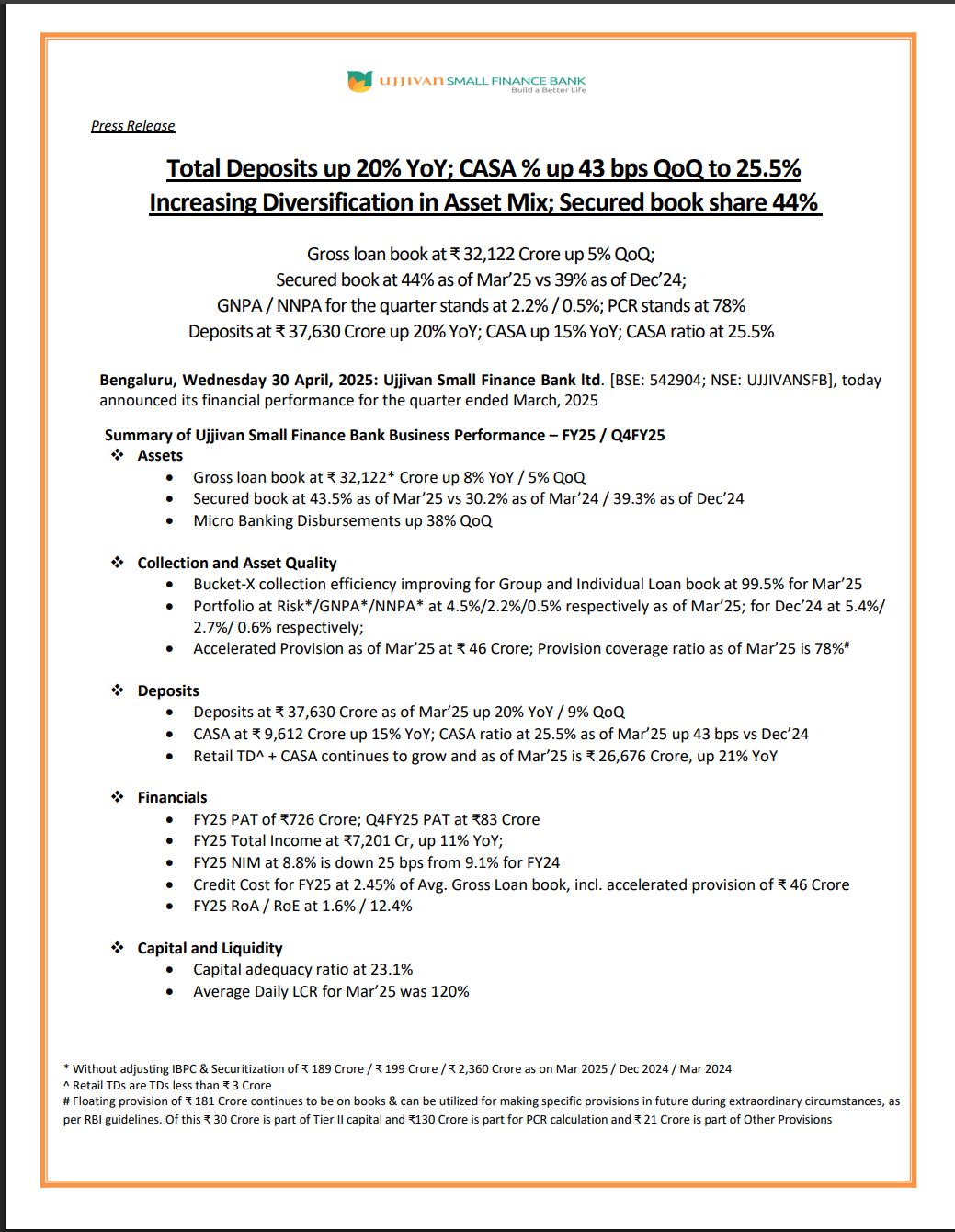

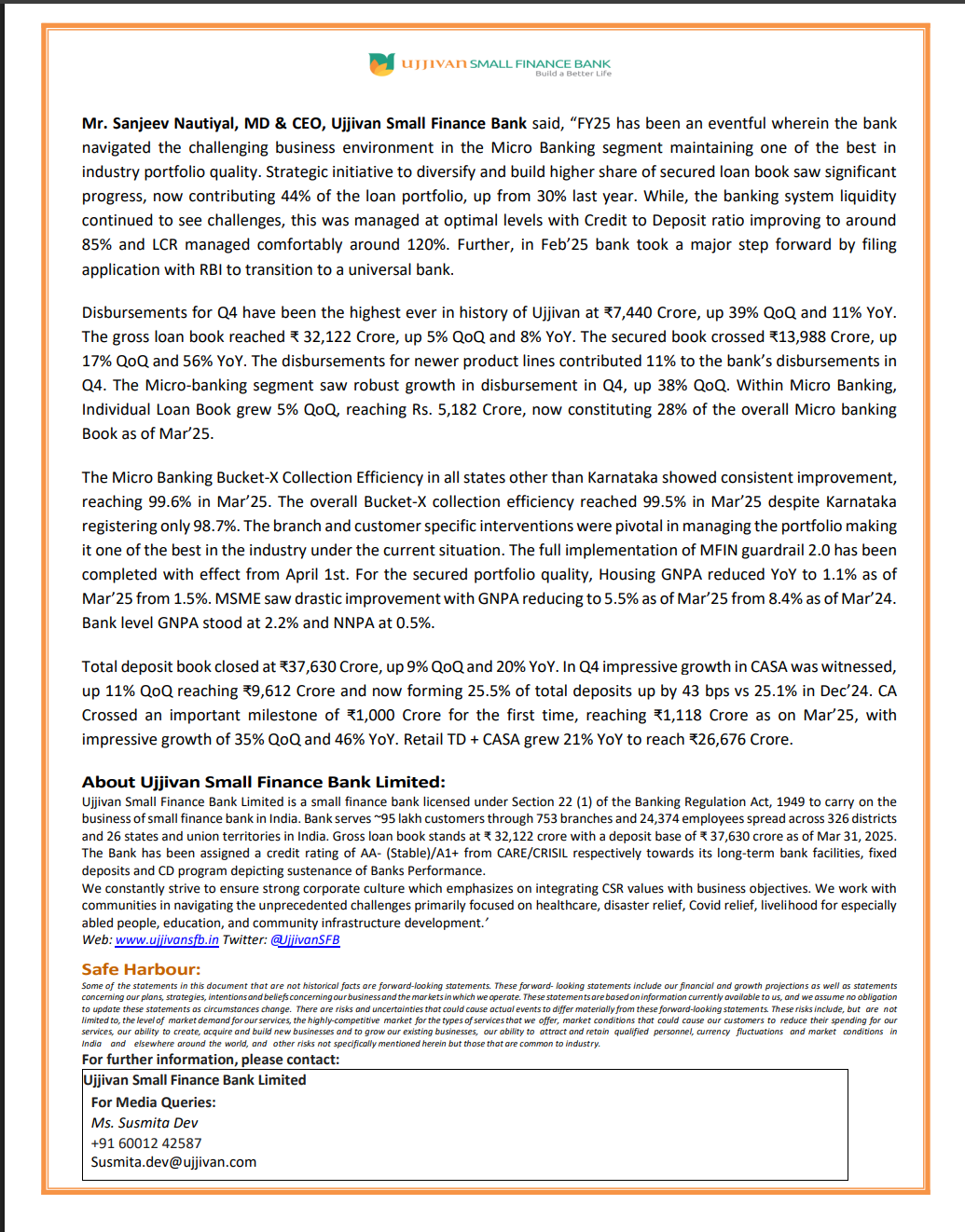

Q4 FY25 Results

Concal Summary

- Newer products (micro‑mortgages, vehicle finance, agri banking, gold loans, etc.) together contributed 11% of total Q4 disbursements

- ARC transaction amounting to 365 crore in Q4, 295 crore transferred from the provision portfolio and 70 crore transferred from the written‑off portfolio, utilizing 69 crore from its floating provision pool for the transaction

- Due to the change in asset mix towards secured, NIMs for FY25 came in at 8.88%.

- Yields might soften marginally however, they are moving into higher yield secured lending products like Vehicle Finance (yields: ~20+%), micro mortgages (~19+%), gold (~14+%) which will offset the softening.

- Also, they are increasing the proportion of Individual loans (IL) which are 100 bp higher than Group Loans (GL).

- Cost of funds will also decrease going forward due to RBI repo rate cuts.

- The small pricing concession given in Q4 was reinstated on April 1, supporting lending yields moving into FY26.

- Guidance for FY26 will be provided along with the Q1 FY26 results to allow the situation to stabilize and offer a clearer perspective.

- Had elevated opex in Q4 due to:

- Investments in secured book and liability business, increased hiring.

- Also, hired manpower in collection-teams to improve efficiency

- Green shoots in eastern parts of the country, places apart from Karnataka are performing well, it’ll take time to normalize in Karnataka

- By FY26 end, aim for the gold‑loan portfolio to represent 2.5–3% of total AUM, with the loan book expected to take around 18 to 24 months to come to a good profitability level. They aim for a 2% ROA for new products like gold loan going forward.

- The large disbursement in Q4 was due to repeat customers, reflects early signs of demand revival among at least repeat borrowers.

- The bank expects to start acquiring new customers this year as the collection efficiency has improved and they can focus their manpower in bringing new business.

- Geographic Diversification, Higher Individual Loan Contribution,

Strategic Branch Categorization (green, amber, red) helped them have a good disbursement compared to their peers.- Normal business happened in green categorized branches while red had restrictions placed for the last 2-3 quarters

- The impact of the industry’s Guardrail 1.0 was largely on Group Loans, so the higher share of IL, which had a lesser impact, helped maintain asset quality and potentially disbursements compared to GL-heavy peer.

- The TN situation is very recent and the bill was passed smoothly, and their haven’t been any field disturbance yet. Expectation is that there won’t be same kind of effect as they saw in Karnataka.

- Management expects lesser impact of Guardrails 2.0 than 1.0 as many parameters overlap and they have lowest exposure to customers with loans from three or four lenders (3L/4L overlap) in the industry.

- Bank has well-defined customer graduation path like from GL to IL or MLAP; retaining eligible customers by shifting them to appropriate products as per their income and credit profile.

- Guardrail 2.0 will make the customer to choose the best 3 lenders and this open opportunities for lenders with a larger suite, interest rates and processing.

- Some companies might face liquidity issues due to the current environment which can open additional market for the bank

- Applied for Universal Bank License in February and are waiting for communication from RBI

Disc: Closely tracking