Among all SFBs/MFIs, Ujjivan has delivered the best pre-quarter update for Q4FY25 which provides confidence that it has turned around.

- QoQ, its PAR has declined significantly from 5.4% to 4.5%, GNPA from 2.7% to 2.2% &

- Collection Efficiency from 96.0% to 96.9%.

- Ujjivan was the first bank to have acknowledged the oncoming sectorial issues of overleveraging and possible disruption due to implementation of MFIN guardrails during Q4FY24 itself and thus it turned cautious ahead of others and slowed down its group loan disbursements (down 25% in FY25).

One question/observation imo :

Q Why FY 2026 is projected to have stagnant PAT growth, leading to reduced ROA and ROE. Is it the impact of decline in MFI loans?

Ans as per me : Yes, that’s definitely part of it.

-

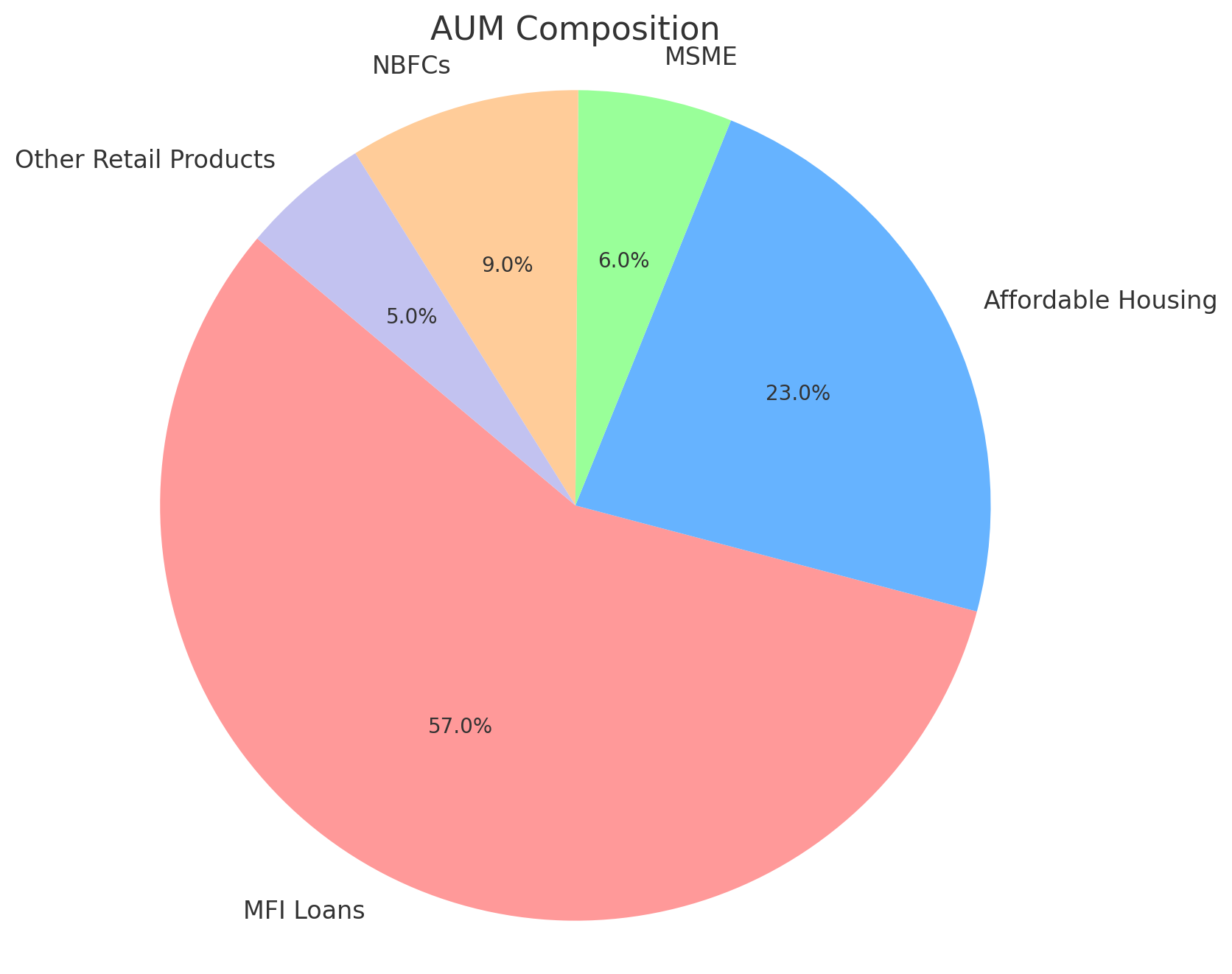

Since MFI loans are higher-yielding, their lower share does hurt margins a bit.

-

But honestly, the bigger story is that FY26 is more of a transition year for Ujjivan.

-

They’re still feeling the aftereffects of being cautious with disbursements in FY25, plus they’re shifting towards safer but slightly lower-return assets.

-

On top of that, they’re investing upfront to fuel future growth. So, it’s a mix of factors leading to a temporary dip in profits — but things should pick up sharply from FY27 onward.