IMHO, presenting of the facts in press release (saying that…adding incremental profit of 150 cr through this acquisition) is a case of conveniently being miser-on-truth. This along with inexplicable manner of compensating warrant holders through CCDs, raises serious questions on corporate governance.

4 Likes

Now see the changes in management, frankly think all is not well here. No quarterly update till date

1 Like

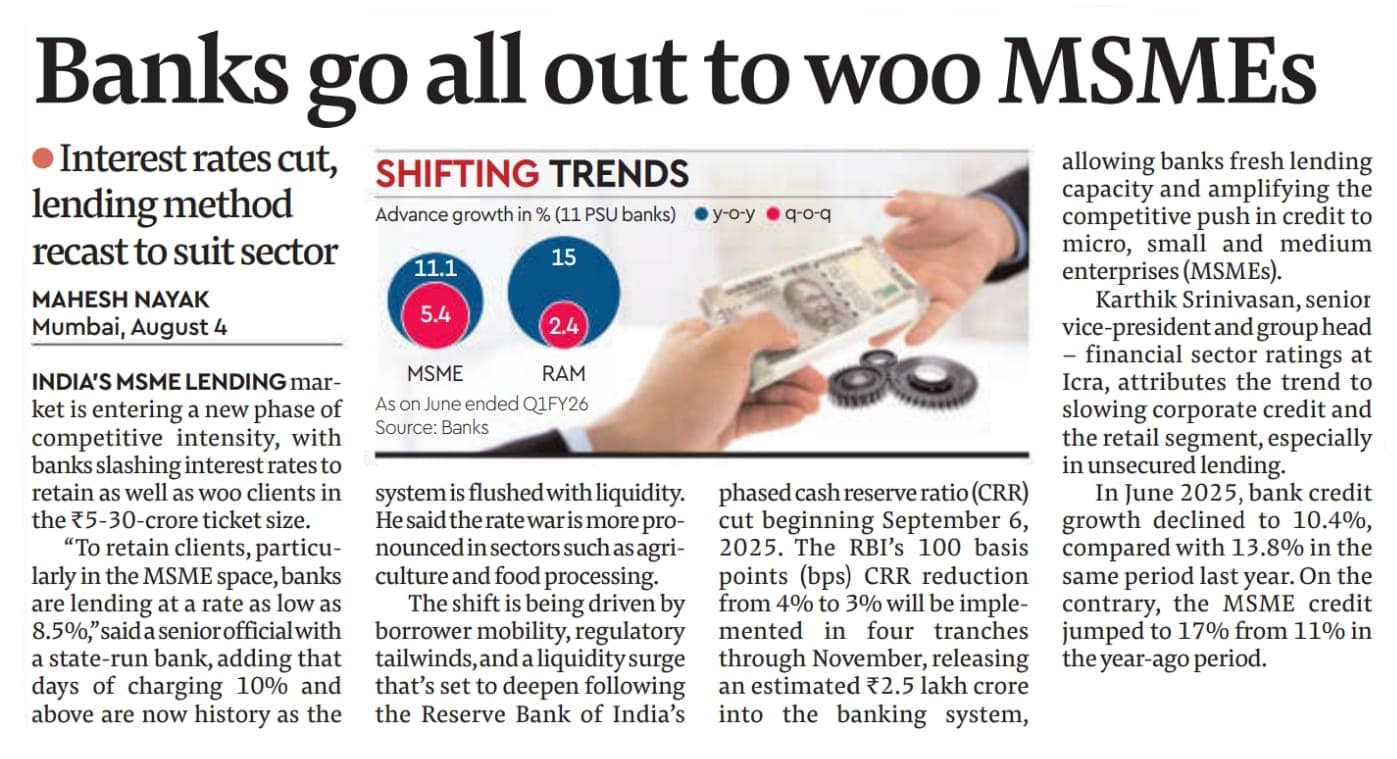

Will this translate to lower cost of funds for Ugro Capital, remains to be seen. The article mentions loan ticket sizes between 5-30 cr, I think most of Ugro’s loans are smaller than 5 cr, but still, the ample liquidity in the system should help them bring down CoF. If they are still not able to lower it then it is a red flag. Awaiting eagerly for the quarterly result, may get an indication on why 2 senior execs were let go/resigned.

1 Like

CFO Kishore Lodha resgined and has moved to Capri Global

1 Like

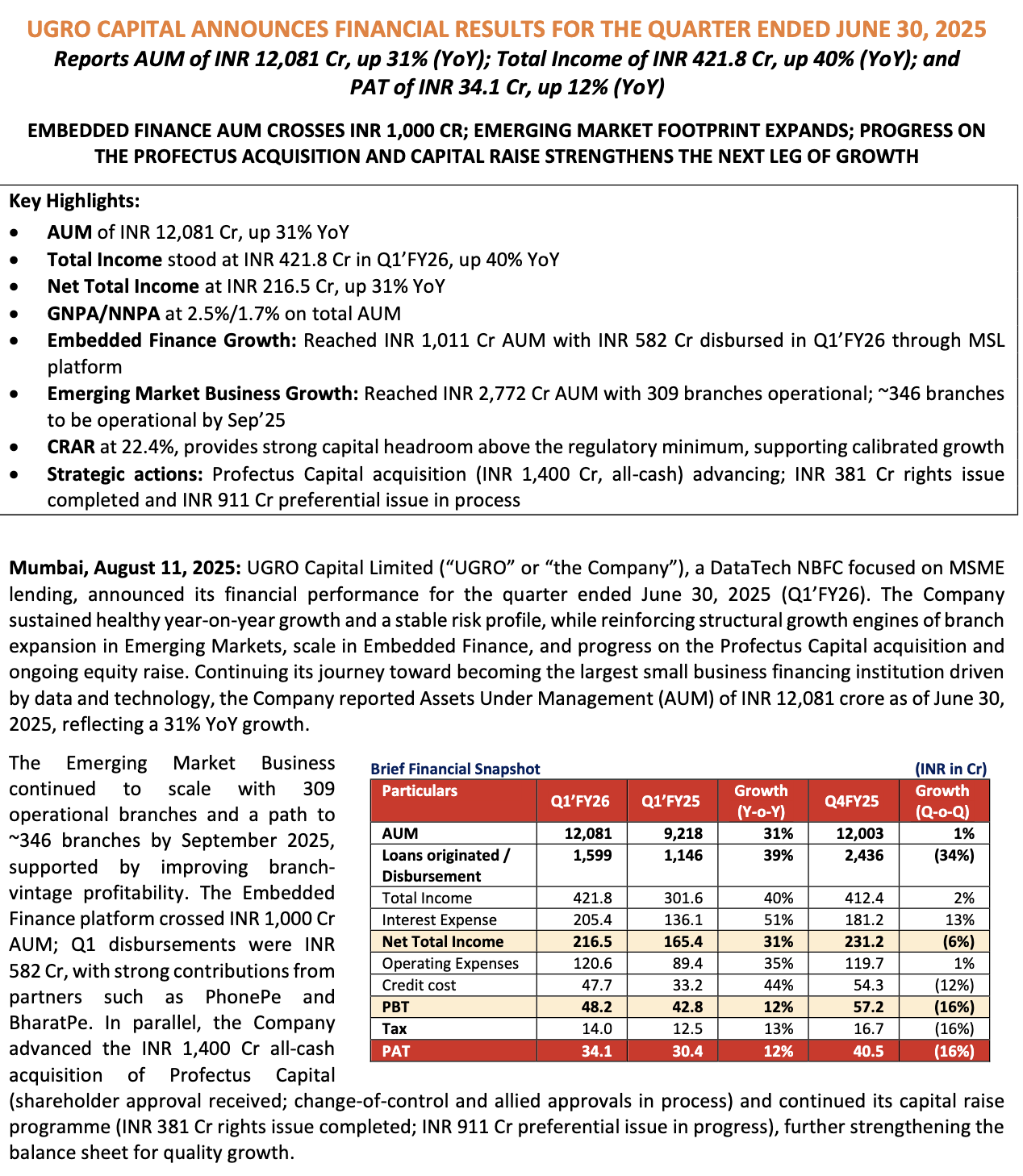

Result is out!

Much was said regarding the asset quality and it comes out quite stable with slight increase, that’s too when the AUM is quite flat qoq.

4 Likes

I think it will reflect in next quarter, i was also surprised by interest expended not coming down qoq, but then it appeared to me that actually they have taken extra loan this quarter and hence interest paid increased. Further, the article shared by you also says something on the same lines - that CRR reduced by RBI will come through November.

Results are out and i am not that much happy about NPA numbers. Although CoB coming down in future will increase profitability and as per latest data p/b is .75 only. So, i hope slippages numbers will stabilize here and even a little bit of growth will be enough to push share price higher.

Forgot to add one thing here, net NPA for MAS financial services, another respected lender in msme space is hovering around 2, compared to that ugro is doing better. Although slippages have increased, but it is still under control, hope it will improve, nothing better i can expect. If it is delivered, more than enough.

3 Likes

Mix is improving, gross yield is also improving, if asset quality remains at 2.5 percent, then valuations are cheap.

MSL has also been contributing to AUM sufficiently for its price.

Net yield will improve now once they slow down their NCD rollout speed and price for the extra capital on book.

Markets worry should and could be the execution of the Profectus acquisition i.e. achieving cost synergies, which is easier said than done.

4 Likes

Investor presentation is out:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/06ec7238-b935-45f8-b0d5-47c0c7e9c248.pdf

CoB is decreasing and should be around 10.25% at the end of this Fiscal. (my guess by checking the trend the fact that RBI gave 75bps cut).

Net yield is increasing, it has increased by 80bps from the q1 2025.

Opex to AUM is quite high at 55.7%. Management guided that they would be finishing with the EM branch expansion by q2 2026 and after that it should steadily come down and that would be the time when PAT would increase significantly due to operating leverage.

So, Risk profile is stable unlike the results I seen from other NBFCs. Management is diligently adding branches, operating, raising equity, acquisition, I could find any red flag.

What you all thing?

3 Likes

What should be the new bvps after these results? And p/b now?

If AI is not wrong then it is currently trading at .75 times book value as per latest quarterly results

One more thing to note is that although posts above are underplaying asset quality deterioration, i feel like it a sign of worry, but on the other hand from the presentation it can be seen that company’s new branches has worse asset quality than old ones, so as the branches mature i assume that it should improve and it is not stretched imagination. Why this happens, i have very less idea but sounds reasonable. Regarding people leaving, the new guy is also from same company, and it seems that ugro has systems in place, so it is a bit worrisome that some left, but i feel like it is like fast food restaurants, if an employee leaves, because of underlying systems, the taste doesn’t change much. Integration of profectus we will have to see how it goes.

Bottom line i am tracking is branches maturity and asset quality improvement. Profectus Integration.

Positive for me is less than .75 p/b. Company didn’t post any losses even during covid. Systems as per presentation are robust, to be precise no over reliance on any single data point mitigates risks to a huge extent.

Rest is hope, that nothing goes really really wrong and company starts posting losses.

4 Likes

Need to be mindful of US tariffs second order effects on MSMEs

RBI has approved acquisition of profectus capital.

2 Likes

Seems like a lot of people stuck at higher valuation are selling the moment stock tries to move upwards. And it might persist for some more time.

My 2 cents on Ugro Capital; Disclosure - Invested at around 200.

At around 0.7x FY27 BVPS, there isn’t much risk to buy at these levels IMO. While the RoA has trailed extra bullish / amateurish management guidance in the past, there is clear potential to reduce the cost of borrowings by at least 100 bps over the next 4-5 quarters, with ratings improvements, seasoning of the loan book.

The tampered down growth outlook from the management is prudent, considering that Ugro needs to improve its unit economics (NIM / RoA) first.

In any case, reduced growth guidance does not justify 30% discount to BVPS since the credit quality has largely been consistent (QoQ improvement in Collection Efficiency reported in this quarter)

4 Likes

Collection efficiency reaching 100 % from 96 % is good sign. This will definitely curtain future GNPA. Cost to income ratio is increased due to expansion of branches which is over now, so it can decrease in future where operating leverage kicks in. Rest all depends on Management Execution and God. Do not see much downside from here.

Disclosure: Holding and biased

1 Like

One thing I am unable to understand is when they have raised so much capital, and are saying they won’t need any more for next few years, why do they keep issuing NCDs and CCDs almost on daily basis? Is there any issue with it? I mean this is now feels like the main issue with the company to me.

I have a lot of money in my piggy bank is what they keep repeating, and I will deposit it in bank or use it and earn money on it but all they do is going again to relatives and touching their feet to get 2 or 3 rupees and putting it in piggy bank. I am unable to understand it, someone please explain it to me.

2 Likes

As some NCDs mature, they repay that amount and issue new NCDs. This is normal for all NBFCs. Simply put, they repay their debt and take new one to maintain the capital base. New NCDs are at lower interest rate comapred to older one considering the interest rate and credit rating.

CCDs dilute the equity shareholding.

4 Likes

Have been following the company for quite some time now, i think there are huge skeletons hiding in the closet in the books. The company first said they wanted less money and hence asked their investor to invest less; however, it does not seem like it. They have been getting funding from all the avenues to purchase Profectus; however, the deal does not seem very lucrative for ugro as overall, even after the deal, although there would be some growth in the books, having synergies won’t be possible in the teams for such smaller companies, and most of the management and staff of Profectus would surely not stay.

1 Like