I got a few personal messages to share my opinion on right issue and on Ugro in general, so here are my two cents.

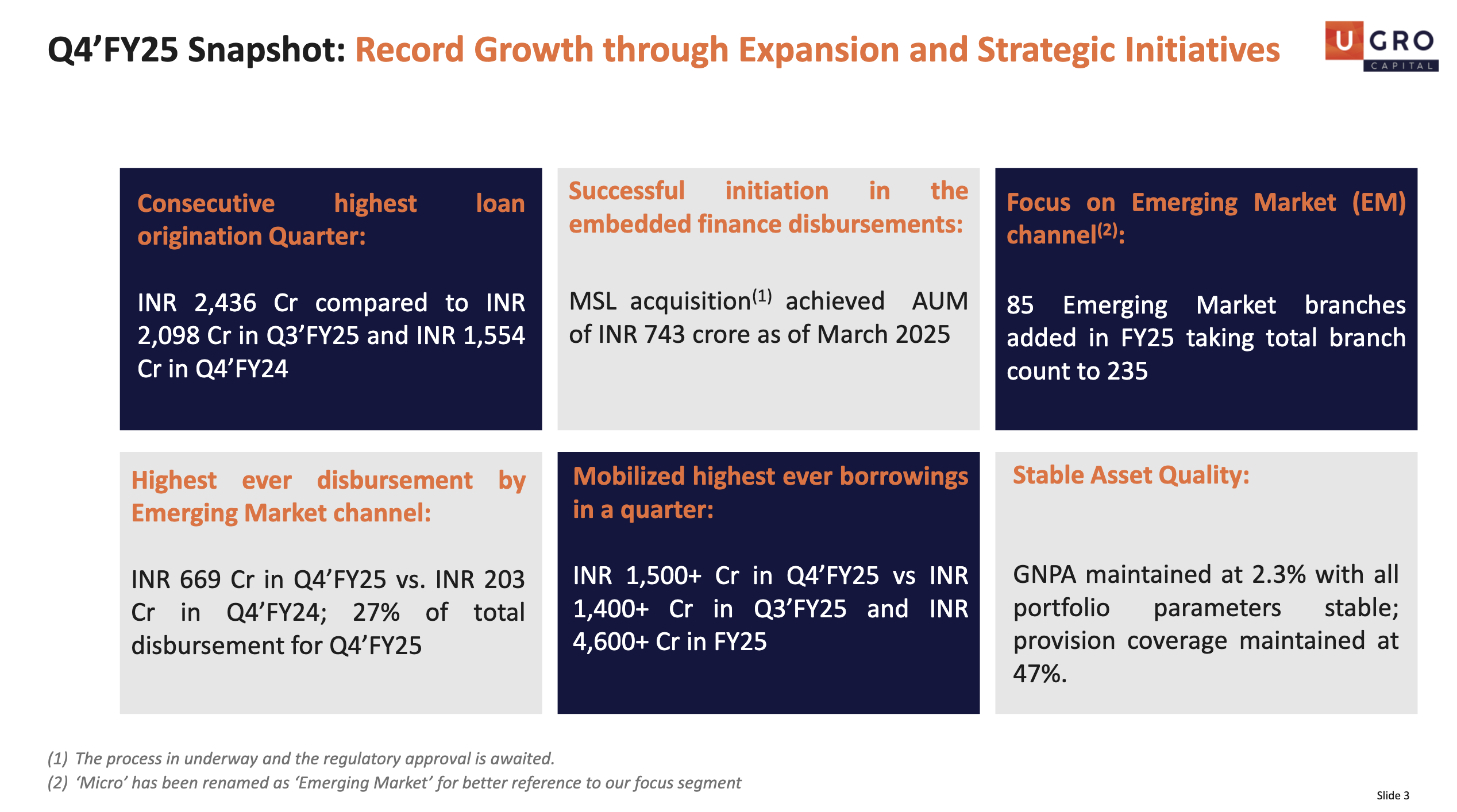

Highest ever borrowing:

They are very satisfactory, highest ever borrowing i.e, 4600+ Cr in FY25. This is too good to be true; I mean when there were significant market concerns around NBFC sector growth and sustainability, Ugro was able to mobilize this huge amount. This shows the trust and reputation Ugro has among its creditors. Be mindful of the fact that lending from Bank to smaller NBFCs (not the established ones i.e, likes of Ugro) is way more stringent than general lending to bigger well established NBFCs. If there had been some ballooning for NPAs or impending deterioration in the asset quality, way before market, lenders would have already tightened the tap for Ugro.

Emerging market engine:

One of the growth areas I am out-rightly banking on is the Emerging market. They have already opened 85 Emerging market branches in FY25 and around 65 would be opened by the end of CY2025. The green shouts are already visible as of Q3 2025. This will further improve when the opened branches get stabilized and break even, should be visible in or before the result of Q32026.

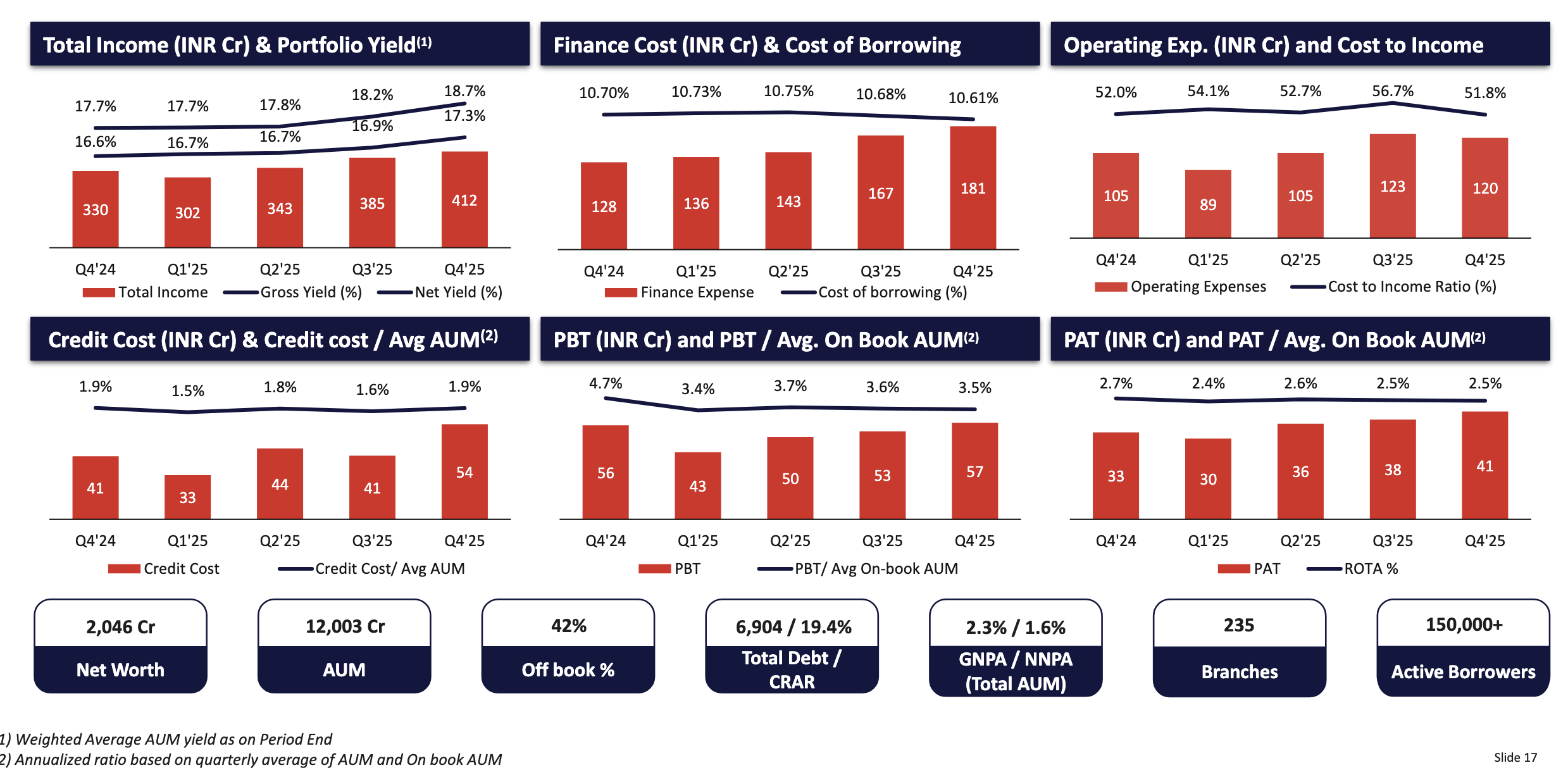

Cost of borrowing

When the cost of borrowing of most of the AA- or AA NBFCs saw a significant spike, Ugro demonstrated a rather stable number and you can even see it dipping downwards as of Q32025. After 3 consecutive RBI rate cuts, the recent one even was 50bps, Ugro is, in my opinion, heading towards 10% within the next 4 quarters.

Major Issue with the slow pace of reduction in cost of borrowing : One of the major issues that Ugro is facing, and would always face until it scale past some 50k AUM, is the un-availablity of a strong parent on the top. This leads to a risk premium whenever Ugro either ask for a rating upgrade or credit from lenders. Ugro is one of the very unique NBFC which is non-promoter driven from the day 1. What ever they have achieved is the reflection of their governance and business model (good or bad, I leave this on the readers to decide).

Stable asset quality:

When the entire NBFC sector is struggling with maintaining asset quality and elevated credit cost, Ugro has demonstrated rather stable asset quality; nothing that is out of order. Only caveat is with rapid expansion in AUM, the NPA/GNPA numbers look artificially depressed. So, I will take the reported number with a pinch of salt and would rather also trust the management commentary where they said that the credit cost will be stabilized at 2%.

In a nut shell:

Ugro is a long term bet for me, I have invested significantly in the past 1 year with my average price at 220INR. I might apply for 50% of the rights issued to me and sell the rest if get good premium. That’s the plan as of now and it may change at any time. Company is doing very good and I do not see any red flags. If I were to invest basis market sentiments, I wouldn’t have invested in any of my portfolio companies. At this valuation; considering the growth; IMHO; there is nothing to loose in Ugro. I will take a pause here.

Disc.

Invested and biased, please do your own due diligence before taking any investment decision.