UFO has been sharing advertising revenue with the exhibitors for a while now…In some quarters it is as high as 40% of the advt revenue(calculated by dividing advt rev share in operating cost/advt revenue). 40% is quite significant in my opinion. What good is a duopoly if they cant take advantage of it. They dont hike their VPF too often. I find that difficult to understand since the distributors dont have many options other than UFO and Real Image.

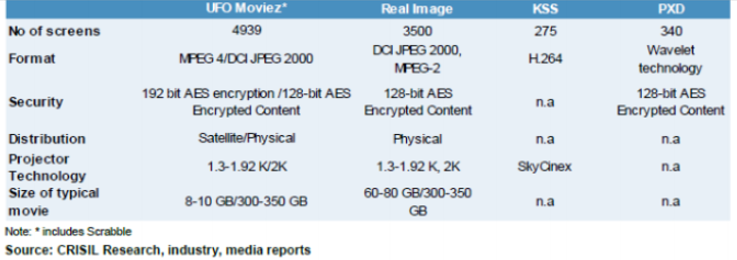

UFO does not do physical delivery of the content. It encrypts and encodes the content, uplink the file using the services of HCIL in Hyderabad, installs ‘Cine Blaster’ servers at exhibitors that receive the file through the satellite and it is then projected on the screen using projectors which in most cases are leased out by UFO(Panasonic brand and not owned by the company). As far as I know, physical distribution is only done for DCI JPEG 2000.

Advertising is the key growth driver for the company now. VPF from D-Cinema is expected to decline. VPF-E Cinema depends on the number of movie releases. Leasing of equipments will give them stable revenues. Since Indian theaters are nor 100% digitized, I wouldnt expect much growth from VPF and Equipment. Not sure if the company can replicate its past growth only from advertising. Lets not forget that distributor revenue grew by 64% CAGR since 2010 and now its declining/slowing down.

-Capex cycle is over. The company is expected to generate fcf going forward. The company used to buy equipment which was expensive. Also acquisitions of stakes in their subsidiaries led to high capex.

-Caravan Cinema, Club Cinema and UFO framez are some initiatives taken by the company to grow its advertising business.

Corporate Governance issues

Case against the promoters for illegal acquisition of land through Valuable Technologies

There have also been instances of misappropriation of funds by employees in the past.

UTV Movies filed a case against the company due to issues related to piracy.

80 group companies out of which 64 are loss making and 24 have negative net worth.

There are significant related party transactions in the case of UFO Limited.

The company also completely wrote off investment worth 8.4 cr in of its subsidiaries right before the IPO.

Majority cash in current account

Patent infringement case (Real Image)

The company has not been paying full tax. There was also a tax raid at UFO movies and Valuable group.

Acquiring subsidiary companies at a premium and Goodwill forms a significant part of the book value.

There is a high probability that this is the patent under dispute. It is essentially the whole technology of satellite distribution and the tracking system.

Also. one should not refer to their gross revenue numbers for growth- something that the company is doing in their presentations too. Net revenues is the measure to use since the revenue sharing agreements can change significantly year on year. For example, gross revenue growth in VPF-D cinema was 13.4% while after sharing advt share with the exhibitors the actual increase in revenue is just 6%. Clever accounting in my opinion.

Also sale of equipment is recorded when dispatched. In many cases such companies would print an invoice before the quarter or year end to meet targets and later take back the equipment. Again something we should be aware of.

Although, in cinema advertising is growing fast, I would not want to invest in this company due to many issues.

Does anyone have any idea on which multiplexes have UFO as their content distributor? Also any conclusive data on whether multiplexes are really moving to independent sourcing model by bypassing the distributor.

UFO Moviez Announces Q4 & FY17 Results

Q4 Advertisement Revenue stood at ₹449 Mn & EBITDA stood at ₹490 Mn

PAT grew by 9.9% to ₹195 Mn during the quarter

Advertisement Revenue for FY17 grew 13.4% to ₹1,790 Mn

Board Recommends Dividend of ₹10 per share in FY17 compared to ₹8 per share in FY16

Mumbai, May 17, 2017: UFO Moviez India Limited, India’s largest digital cinema distribution network

and in-cinema advertising platform in terms of number of screens, today, announced its financial

results for the quarter and year ended March 31, 2017.

Financial Highlights:

Quarter ended March 31, 2017

Consolidated revenues grew by 6.0% to ₹1,556 (Q4FY16 - ₹1,467) million. EBITDA stood at ₹490

(Q4FY16 - ₹531) million and PBT stood at ₹270 (Q4FY16 - ₹322) million. PAT was higher 9.9% to

₹195 (Q4FY16 - ₹177) million.

Excluding new businesses (VDSPL), the consolidated Theatrical and In-Cinema Advertisement

business delivered Revenue growth of 6.7% to ₹1,548 (Q4FY16 - ₹1,451) million, EBITDA stood at

₹504 (Q4FY16 - ₹559) million, PBT stood at ₹307 (Q4FY16 - ₹360) million and PAT grew 7.5% to

₹232 (Q4FY16 - ₹216) million.

Advertisements revenues stood at ₹449 (Q4FY16 - ₹466) million.

Year ended March 31, 2017

Consolidated revenues grew by 4.7% to ₹5,989 (FY16 - ₹5,721) million. EBITDA stood at ₹1,845

(FY16 - ₹1,848) million, PBT stood at ₹959 (FY16 - ₹981) million and PAT stood at ₹632 (FY16 -

₹635) million.

Excluding new businesses (VDSPL), the consolidated Theatrical and In-Cinema Advertisement

business delivered Revenue growth of 4.9% to ₹5,949 (FY16 - ₹5,671) million, EBITDA grew by 0.5%

to ₹1,927 (FY16 - ₹1,918) million, PBT grew 4.4% to ₹1,130 (FY16 - ₹1,082) million and PAT was

higher 9.0% to ₹803 (FY16 - ₹736) million.

Advertisement revenue grew 13.4% to ₹1,790 (FY16 - ₹1,578) million. Average advertisement

minutes sold per show per screen increased to 4.34 (FY16 - 4.15) minutes during the year.

If we exclude the impact of 3rd Qtr due t Demonitisation, I think it should give good FY18results Q-Q and Y-Y…Near 52 low of 400…Its a good buy…Invested with minimal qty, ill look to increase post price reaction stabalisation

Yes as of now market is pricing in less than 7% yoy gworth. Potential for 25% + yoy growth. Great moat buisness available at minimum downside and great upside. Also dividend is icing on th cake.

@Alphin - Could you throw some light on the growth levers for this company in the future to achieve the 25% growth rate?

Based on my readings,their current revenue generators like Virtual Print fees,equipment rentals are more or less stabilized and not going to contribute much in the future. In fact,the company has stated their revenues from VPF is on the decline.

The other area where the growth could materialize is in in-cinema advertisements by increasing the rates and the number of minutes.

There are 2 other new businesses like Caravan talkies is a seasonal business with only 9 months per year and it is in very nascent stage.Not sure how this model could be scaled up.

They are also working on franchise model called UFO framez which is asset light model in brownfield projects to convert the single screen into multi-screen theatres.Again this is still a model that is evolving and they are expecting to add more screens through this model.

All these put together does not give a clarity on 20%+ growth.

I have been looking at this company for a while now. I have few questions that I hope some of the guys here can answer

What is the sustainability of its business model? Does it have any competitive advantage? Given that it makes money by enabling the transmission of the movie through satellite (3rd party uplink facility in Hyderabad / Projectors are Panasonic and servers are also bought from 3rd party sources) , what is the proprietary technology that UFO has that can sustain its business when a disrupter comes along?

I have been reading some reports on the growth prospects of DCDC and Cinedigm (both are the US equivalents of UFO) and one of the major challenges that was mentioned is the sustainability of the satellite model. At present a normal E-Cinema movie which is compressed and transmitted through satellite takes 4-5 hours to get downloaded at the exhibitor server. With technology improving and wider color gamuts emerging and frame rates improving, file sizes are only going to grow. But satellite bandwidths wont grow and it would be taking even longer hours to download. You need to setup more satellites which is expensive. Hard drives continue to grow in capacity for a particular cost and at some point in time, transporting through hard disks will again make sense for distributors and exhibitors. In that case, how will UFO be able to position itself given that it gets substantial revenue in the form of VPF E-Cinema?

As I have mentioned above DCDC is a US equivalent of UFO and is formed by collaboration through some of the largest players in the value chain like AMC Theatres, CInemark, Regal Entertainment (Exhibitors) , Universal Pictures and Warner Bros. (Distributors/Studios/Content Creators) . With this, currently DCDC has a network of 30,000 screens in the US out of 40,000. DCDC continues to collect VPF from all its clients (distributors/producers) until it breaks even on its cost of installing the equipment at the exhibitor level. Post achieving the break even, it will no longer receive the VPF from the studios after which its revenue model becomes highly uncertain. What stops the same thing to happen in India? What if the big players like PVR, Inox and big production houses collaborate to create something similar in India and offer better terms to the exhibitors (better revenue sharing as they can afford to lose money and gain scale)? Also, the same DCDC or others can expand as well. So how will then UFO be able to sustain its revenue streams?

While it is too early to comment on Caravan Talkies as it has not yet achieved the scale that UFO desires, even that business doesn’t seem to have any inherent advantages. Any one who sees an EBITDA margin of 50% (that is what UFO expects from Caravan post achieving the desired scale) would be attracted to the business thereby increasing the competition. However, the advantage that I feel that Caravan has is that it now an extension to the In-Cinema advertising system post changing its business model and UFO can now offer a bundling package to advertisers.

While the company is generating FCF and is trading at an attractive valuations, the uncertainty in the revenue model is the deterrent. 5 years down the line what stops the exhibitor to not terminate the contract with UFO and go for something better?

Hope somebody can clear these doubts.

The main advantage with UFO moviez is the network effect. It has aggregated distributors, advertisers and cinema owners through a single platform.

As you said the technology might improve significantly but a new entrant in the field will not find it easy to convert all three distributors, advertisers and cinema owners to the platform…

Also a US entrant will not bother with the hassle with doing buisness in India with so many stakeholders involved. Even govt decides pricing of govt ads.

Because of this I think that things are more likely to remain same.

Excerpts from the PVR 2017 AR on the growth of in-cinema advertising

“In-cinema advertising Currently, it constitutes 1 per cent of the total advertising revenue pie but has huge growth potential. This growth can be attributed to expansion of multiplexes in metro/ non metro cities and nearly 100 per cent digitisation of screens. Digitisation has resulted in an increase in the volume of ad inventory and the ability to geographically target advertisements with multi lingual support. At the same time, the exhibition industry has become more organized, technologically advanced, and ensures a high level of transparency by providing real time campaign tracking to advertisers. The number of in-cinema advertisers has grown from 50-100 in 2010 to over 2,500 in 2016. Sponsorship revenues for PVR Cinemas increased by almost 19 per cent in 2016 over previous year.”

UFO’s right to collect D-Cinema VPF is set to expire by June 2018 . Total revenue from D-Cinema

(sale of services) is close to 32% of the total revenue (FY17) i.e 162 Crs .

Now 162 Crs has to be compensated by NOVA Cinemas , UFO Framez , Caravan cinemas and other new innovative models . Please correct me if i am wrong !

Check latest results, revenue loss from d cinemas approx 111 crs but increase in advertozing revenue which has been increasing at 25% cagr is 96crs . This gap will widen and d cinema revenue will become insignificant…

Went for Newton movie yesterday… don’t know details of whether UFO operates there or not… but only add shown during break were that of Google 2-3 ads and justdial 2-3 ads.

Just struck me that world’s largest advertising company has to seek in cinema advertising also…

Ads were showing features of android google in Hindi…