Is anyone tracking tyre companies? I see a lot of confusion in markets; while tyre companies are crying foul on increasing tyre imports/dumping by China and making presentations to government to impose strict penalties on imports and on the other hand rubber prices are down, tyre companies declaring all time high profits and dealers are disputing claims of tyre companies that imports are hurting them.

The cry is because of huge China dumping. Chinese tyres are almost 30% cheap than the Indian counterparts. The year on year growth of Chinese tyres imports to India has been 57% in bus and truck wheels and 20% + in passenger segment (last fiscal). To tackle this when the Indian counterparts went with a price cut, the rubber prices started increasing. This led to increase in input prices and reduction in output prices. What we have witnessed for last year, the profits going up like anything due to rubber prices going down, (90% profit growth), will be reversed this year. Assuming that the conditions remain the same (Govt. does nothing to protect the industry), the margins of these companies will shrink with even lower top line growth year on year.

Imagine with this scenario, JK tyre is coming up with capacity expansion. Let the first quarter go, and you will find these stocks even more cheap. I feel one should start buying out then, looking at the broad macro industry scenario.

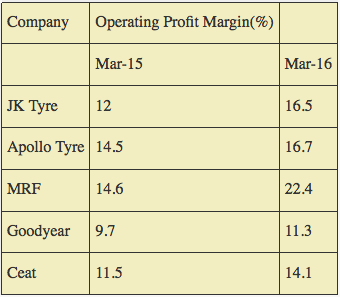

Inspite of decreasing revenue and increasing competition from Chinese import all tyre companies have improved margins. Increased competition should lead to decrease in margin to keep the lost market!

Why is JK tyre increasing capacity despite knowing that Chinese are dumping tyres in India and GoI is not taking any anti-dumping measures?

What we have witnessed for last year, the profits going up like anything due to rubber prices going down, (90% profit growth), will be reversed this year.

Are you expecting natural rubber price to go up this year?

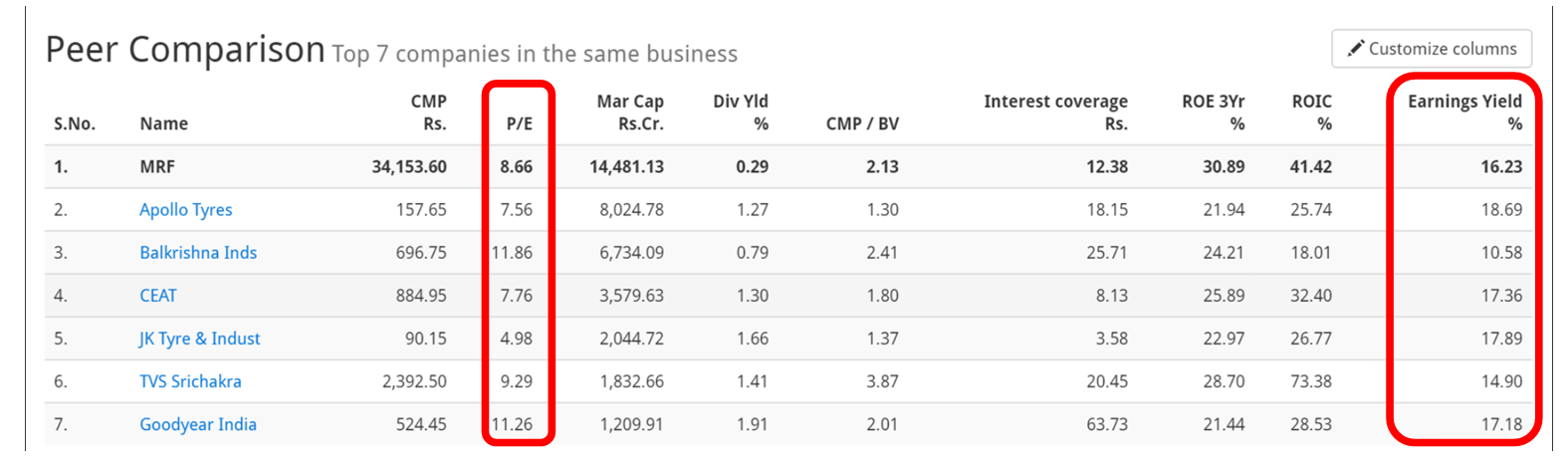

These sector companies are having very low PE and high earning yield as compared to other sectors.

Is this due to the economic slowdown in this sector like Tech companies are facing right now Or anything else?

Reason for this is low rubber prices because of which companies are getting inflated profits for short term. Any increase in rubber price would lead to reduced profits. Even if rubber prices stay low for long time companies need to pass on the benefits to OEMs and end customers in the long run.

Main reason is crude…and not rubber…70% of raw material used is synthetic rubber and the rest is natural rubber…synthetic rubber is made from crude…so since crude and rubber both are down…these companies are enjoying huge margins from the after market segment…anti dumping duty o tyres has been kept low because of high profits pocketed by domestic tyre companies…the market is flooded with Chinese tyres…top line de growth can be witnessed in some of the companies…especially companies dealing in truck and bus radial tyres…40% of the market in T&B radial tyres is flooded with Chinese tyres…it was 15% two years back…check ceat…they have top line de growth…and now they have reduced their margins to 12.50% from 14% to bring top line growth…if crude and rubber price go up…back to their original prices…one can short these stocks…

Just wanted to revive this thread as all the leading stocks in the tyre sectors are currently going through some heavy corrections (which I think was due for sometime now) post bad Q1 results, so we might get some good prices here.

I recently read import duties was established on imports from China… Does anyone have data how much we import from China… And impact on our manufacturers I. E likely volume growth and capacity utilization…

Very strange…i had bought ceat in 2015… At 675rs per share… The earnings were around 110rs per share that financial year… Then stories floated about anti dumping duties imposed and so on and tyre stocks got re rated… From single digit p/e multiple of 7 to now 27😨… But ceat earnings witnessed a de growth due demonetization,increase crude price etc… At present the earning per share( standalone is around 66)… And cmp of around 1800… Sales growth for past 5years is < 5%…market must be discounting growth of how many years?? … However debt to equity decreased from1.33 to 0.3…

Ignore the noise …and see the story so far…

So much for efficient market theory…

Disc: sold all my holding at 1800…

Market never ceases to amaze me…

Counter views welcome

ya, trucks manufacturers can be benefited if there is any such anti dumping duty on chinese companies. They have highest market share (in terms of sales) in trucks. 2 wheelers and car tyre manufacturers are least effected.

Does any one track tyre companies. Which among the tyre stories would be a good investment?

Outlook for the next nine months looks good as demand for 4QFY21 is very

strong and as the low base effect kicks in. Demand in the last two years has

been muted. Replacement demand has been particularly strong due to:

a)rising personal mobility,

b) strong rural demand,

c) robust CV demand, and

d) import restrictions (PVs and CVs – 3-5% of market vacated by imports).

Demand was the strongest for CVs (over 30% in TBR and TBB), followed by PVs and 2W/3Ws. OTR segment grew 42% YoY led by strength in the domestic farm sector and exports. For 9MFY21, volumes grew 2-3%, led by strength in replacement as the same for OEMs and exports have declined.

RM cost: The management expects a further 10% QoQ increase in average RM basket. The same would be 10% higher by the end of Mar’21.

Finished goods inventories are uncomfortably low, leading to a loss in volumes. Utilization is at very high levels and all new capacities are

ramping-up well.

Capex: The management expects capex for the entire year at INR6.5b(INR3.5b already spent during 9MFY21). Over the next couple of years, it would be investing INR8.5b per annum for completion of projects

Q4FY21 earnings conference call: highlights and key takeaways

JKT said (1) it expects the demand situation to normalise from Q2FY22E onwards; (2) it added >1,400 dealers in FY21; (3) raw material prices are set to steepen by 10-12% QoQ in Q1FY22E. The company is looking to mitigate the same via calibrated price hikes, premiumisation of products, operating leverage gains and capacity debottlenecking; (4) debottlenecking exercise is set to expand capacity by ~10% over the next 2-2.5 years at a cost of ~| 150-200 crore; (5) net debt as of FY21 was at ~| 4,500 crore and JKT is looking to retire ~| 1,500 crore in the next three years; (6) Tornel revenue decline in FY21 was restricted to ~5% YoY despite only functioning for ~8.5 months in the year – with FY22E utilisation levels seen at ~95%; (7) consolidated capex spends, going forward, would be in range of ~| 200 crore per annum; and (8) import content in natural rubber is at ~40%.

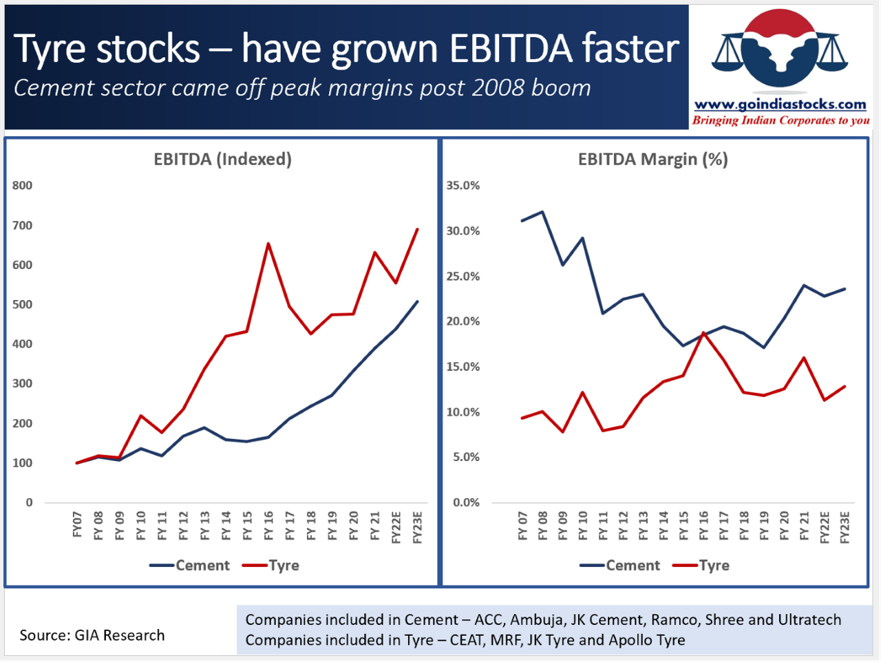

After peaking out in FY16 EBITDA margin of tyre companies have been on a decline. In the recent past, decline in sales of cars and two wheelers have added to the misery. Quite possible that this correction of 5years might be coming to an end. Rubber prices seems to have peaked out at the same time car sales have bottomed out.