TVS Supply Chain Solutions – A Business analysis, 1st April 2024

Background

TVS Supply Chain Solutions (TVSSCS) is India’s largest supply chain solutions company by sales (₹ 90 Billion). The company was incorporated in 2004 but went public in August 2023.

The business is divided into two segments and serves medium and large organizations:

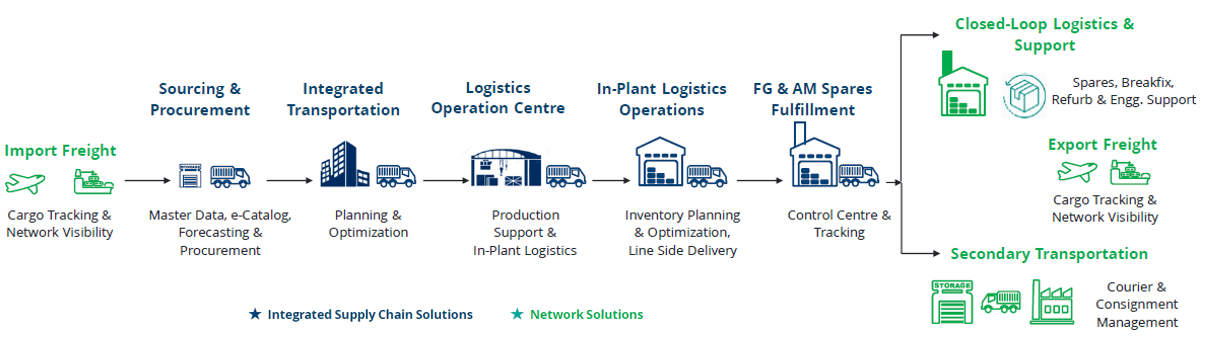

Integrated supply chain solutions (ISCS): This segment offers end to end supply chain services from Sourcing and procurement, integrated transportation, Logistics Operation Centre and In Plant Logistics, Finished Goods and After Market Fulfilment, Consultancy and Professional Services, Product Management Solutions.

Network solutions (NS): This segment provides end-to-end freight management, including last mile delivery.

Basically, a boring but essential business that keeps the world running, see Figure 1.

Figure 1: The two business segments of TVSCS.

Business drivers

While logistics as a business (think courier services) has reasonable competition and modest barriers to entry, integrated supply chain solutions is a complex business to enter and here size and scale do matter. This is primarily due to the type of services offered by players in supply chain solutions, which requires large scale service providers that have deep knowledge of complex logistics management.

A historical perspective: The Indian logistics market used to be dominated by monoline service providers who partnered with industry players and their captive logistics arms for transportation or warehousing requirements until the early 2000s when some captive logistics players like TVSSCS started using their capabilities to service other players as a third-party vendor. TVSSCS pioneered the development of the Supply Chain Solutions market in India.

In supply chain solutions the differentiator is technology and TVSSCS has had a long history of acquisitions to develop and complement its technology suite. They have made more than 20 acquisitions in the last 16 years across Europe, the United Kingdom, the United States and Asia Pacific (including India) (Prospectus, 2023).

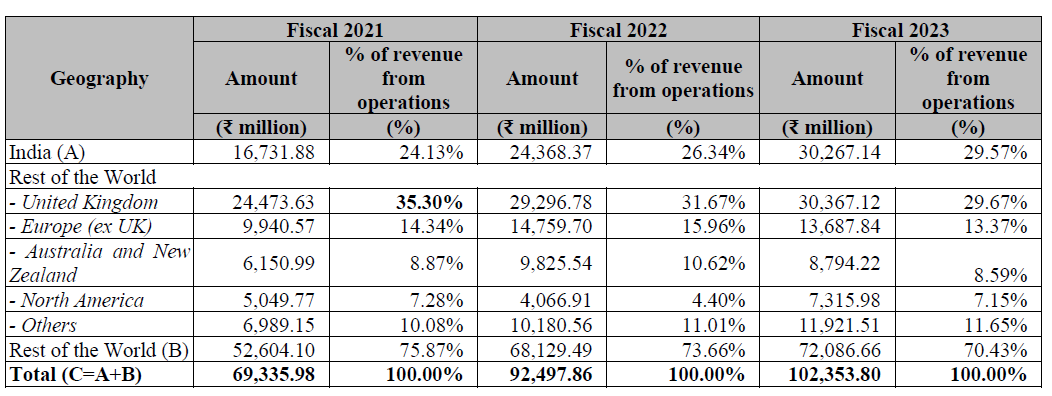

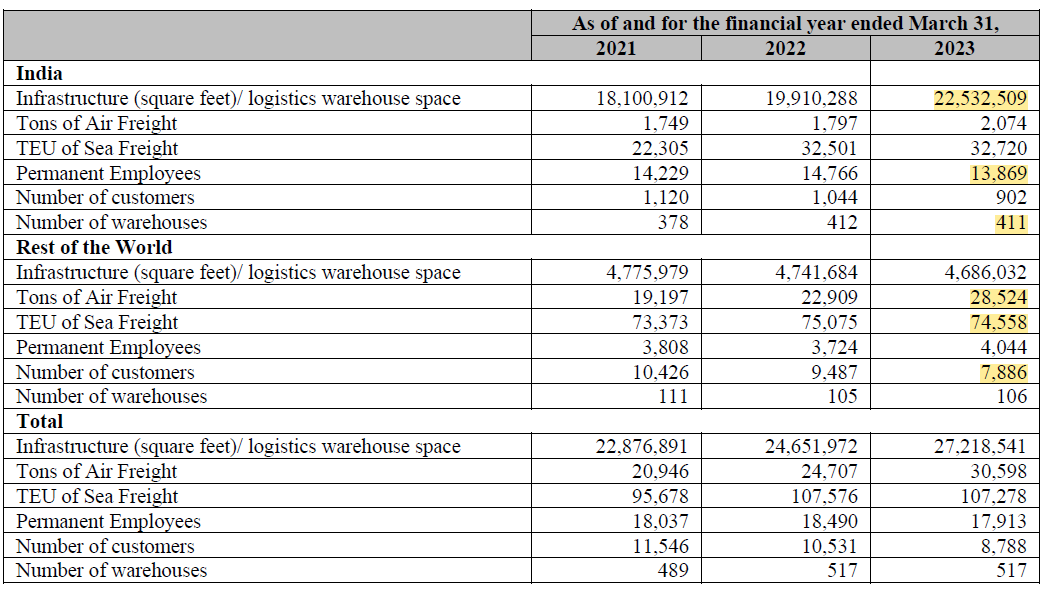

Today TVSSCS is a global player but with a rapidly increasing percentage of the total revenue coming from India Table 1. What seems to have happened is that technology was acquired and is now being used to accelerate growth in India with a lot of the back-office operations based out of India as well to make use of the low cost of labor. See the difference in operational metrics in Table 2, especially the number of permanent employees based in India in relation to the number of customers.

Table 1: The following table sets forth revenue from operations by geography for the years indicated. Note the rapid growth in the Indian revenue segment (Prospectus 2023).

Table 2*: The following table provides a snapshot of key operational indicators (Prospectus 2023).*

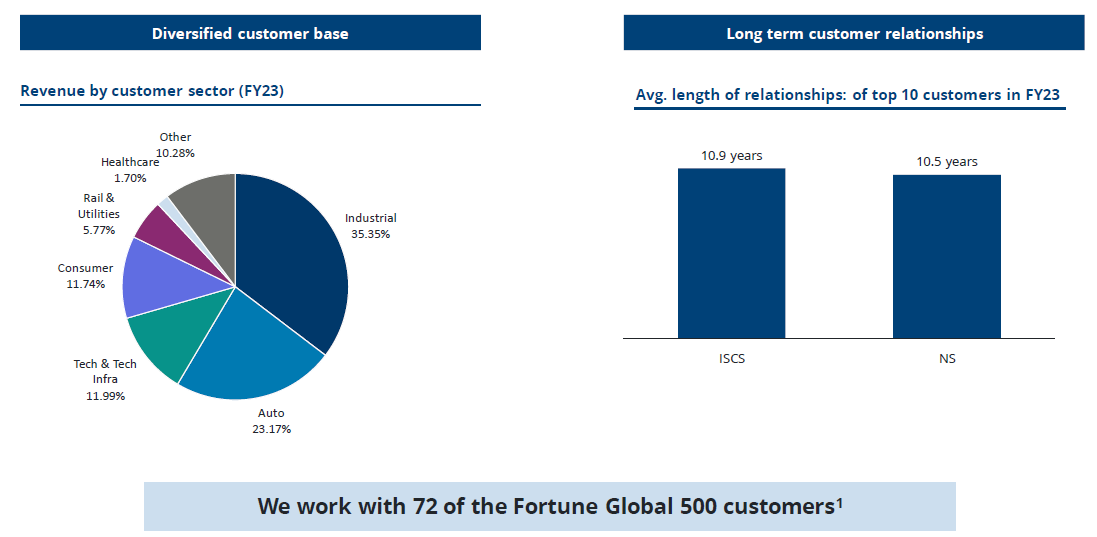

The customer base is very broad and stickiness is high given that the tenure of the relationship is around 10 years on average (Table 2 ). Further, the company serves 72 of the top 500 Fortune companies. The top 5, top 10 and top 20 customers account for 18%, 28% and 39% of the revenue respectively in 2023 (Prospectus, 2023).

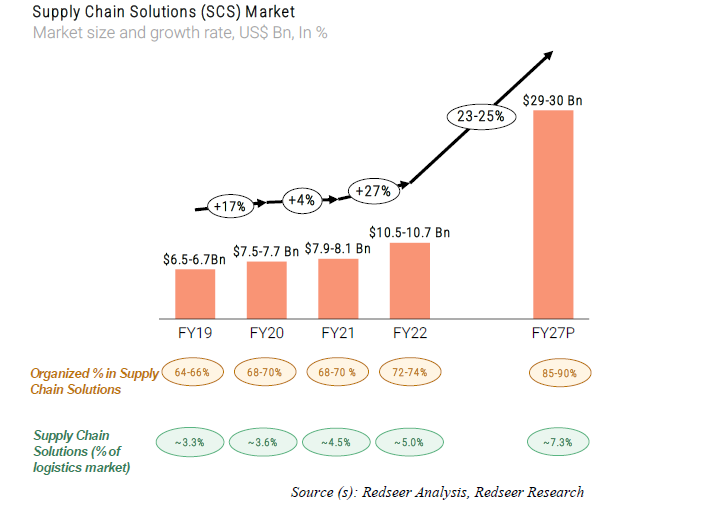

Integrated supply chain solutions business: The ISCS market in North America, the UK and Europe is likely already mature and while that might remain a decent business, growth will probably come from India. According to the prospectus, the SCC market in India is projected to outgrow overall logistics market growth (approximately 22% vs. approximately 6% CAGR between Fiscal 2022-Fiscal 2027). See also Figure 3.

The organized and unorganized market size of the supply chain solutions industry was US$10.1-10.6 billion and TVS Supply Chain Solutions Limited’s market share in the organized sector in the supply chain solutions industry in terms of revenue was approximately 7% in Fiscal 2022 with the most varied client base and one of the most diverse set of services among top organized players in India.

Figure 2: Customer base and length of relationship.

Figure 3: The SCS market is project to grow at a CAGR of 23-25%.

Network Solutions business: Again, this data relates just to India where the freight forwarding market stood at approximately US$4.7 billion in Fiscal 2022 and is expected to reach approximately US$8.5 billion by Fiscal 2027 growing at approximately 12% CAGR.

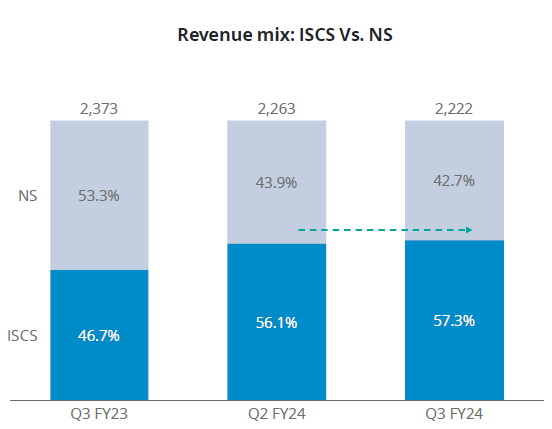

For the company overall, the revenue mix is shown in Figure 4. The mix is growing in favor of the more profitable ISCS business where margins stand at around 10-10.5% (Investor presentation Q3, 2024) while for the NS business the aim is to get the margins to 5.6% although it is around 4.8% today, partly due to the Red Sea crisis (Q3 2024, concall).

Figure 4: The revenue mix is growing in favor of the more profitable ISCS business segment (Investor presentation Q3 2023)

As the first and the largest supply chain solutions company in India, TVSSCS is the perfect position to exploit the secular tailwinds driving growth in India. For instance, the rapidly expanding network of highways, railways and air freight capacity, increase in global supply chains moving to India as part of the post-Covid China plus one rejig. Further, if plans like the India-Middle East-Europe Economic Corridor materialize, its practically a tailormade opportunity as no other Indian company has large operations abroad.

Analysis of Financial Statements

Before analyzing the financial statements, a couple of points of note:

Long-term debt repayment: Using proceeds of the IPO and internal accruals, the company paid down all its long-term debt in Q3 2024. It now has a working capital debt of ₹7500 million at an interest rate of 7.5% (Q3 2024 concall).

Capital lease: The company has an asset light model where instead of purchasing buildings, it leases them for the long-term. Under accounting principles this counts as a capital lease as opposed to short-term operating leases (< 1 year). This is relevant for a few important reasons:

- The annual costs of the lease, including interest, are expensed in cost of goods sold on the income statement. Here’s a quick reference for this topic. The lease cost is basically treated like opex instead of a financial expense, but well that’s how it is. Damodaran has a nice write-up about it here.

- The depreciation and amortization are subtracted out from the earnings on the income statement. There is higher depreciation expense in the early years so earnings of the company are low and will stay low for a while, but since depreciation is a non-cash expense, it shows up in the FCF.

- On the balance sheet the capital leases are recorded on the assets and liabilities (it works just like debt) and the depreciation value is subtracted out annually.

- At the end of the lease, depending on the jurisdiction, you get the right to buy the asset at a value much below fair market value or some other kind of preferred treatment like follow up leases at lower costs. I can’t get any precise info on this in the prospectus or any other company disclosures but good to keep this in mind as a source of unaccounted for value (it gets depreciated in the asset section of the balance sheet till it disappears but of course the warehouse would still be standing)

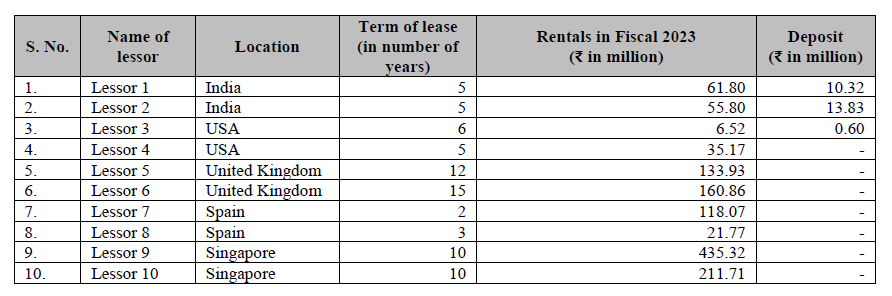

According to the prospectus, the majority of the lease agreements for their warehouses have a tenure of three and eight years. See Table 3.

Table 3: The details of leased properties with the two highest lease rentals paid in Fiscal 2023 in each of the following geographies.

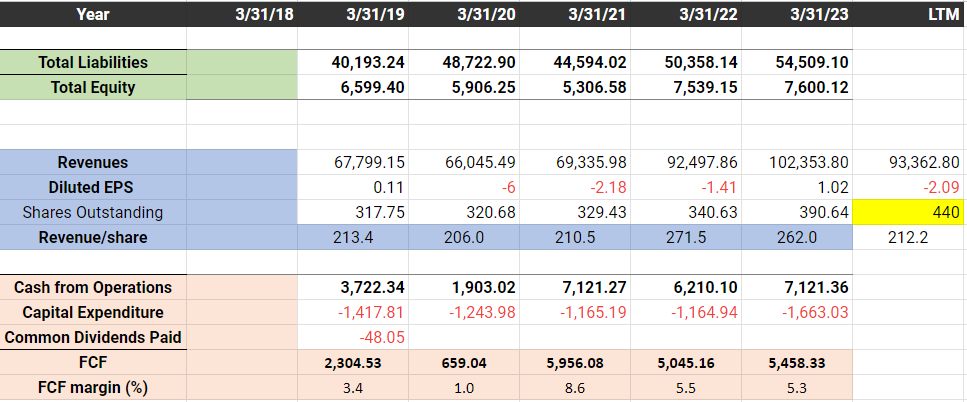

Table 4 captures the key financial metrics. Its best to focus on cash flow from operations and FCF as earnings disappear due to amortization expenses. In the concall of Q3 2024, management mentioned that capex will be 1000-1100 million annually. Debt to FCF is 10, which is high but if I subtract current assets from debt, it falls to 4, which is perfectly ok. Plus, TVS group is the promotor which means they will have no trouble accessing the debt markets, if the need arises.

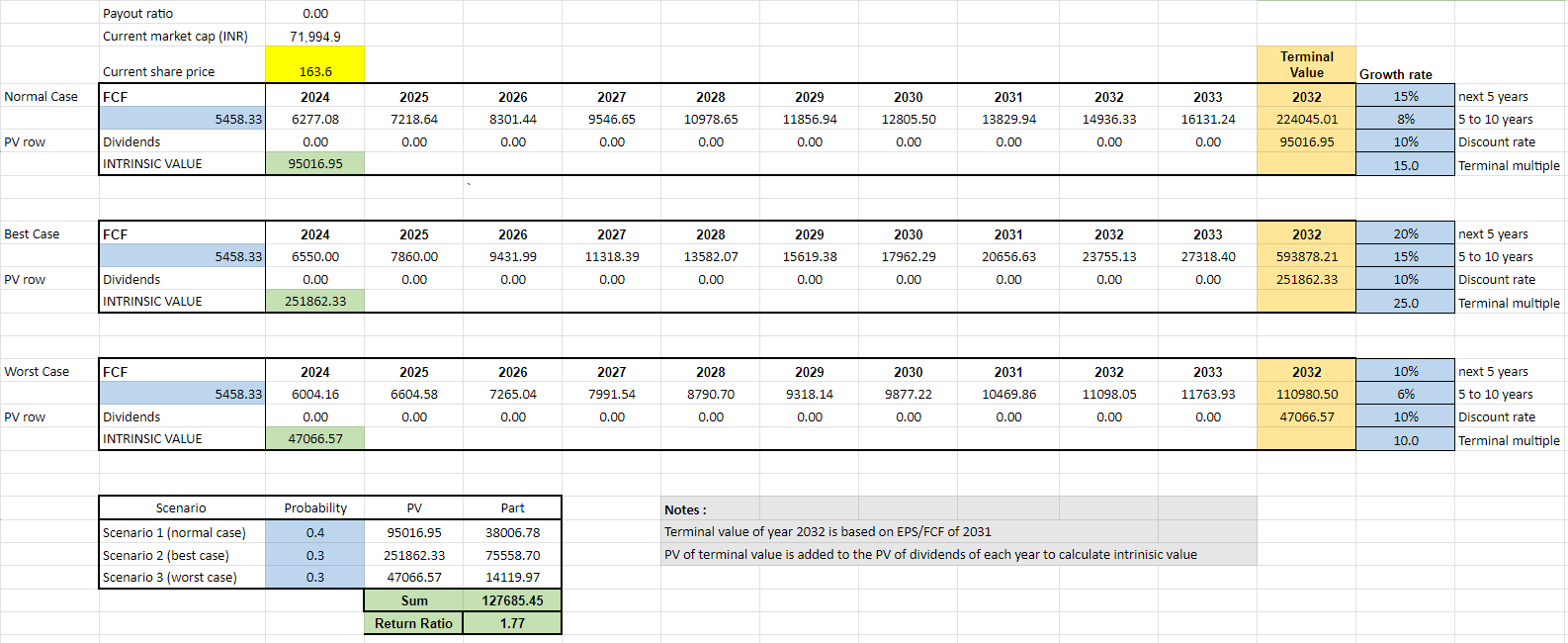

In Table 5, I carry out a DCF using FCF as input and assuming no dividends are paid out. The expected rate of return is 17.7% on average, although I think the best case is probably the most likely.

Table 4: Key metrics from financial statements in millions INR over the past five years.

Table 5: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

Investment thesis

You can pick up a business which in the normal case is at least 30% undervalued and is growing rapidly with secular tailwinds. This might be one of those growing, discounted pies. The biggest risk is that the company is exposed to global macro, so there will be some temporary downturns now and then.

A non-excel sheet valuation: Today, the revenue is ₹100 billion. Let’s say the revenue grows at 15% for 10 years, which is a 4x, so ₹400 billion. At 10% margin (which is the management’s ambition), that would be ₹40 billion in earnings or FCF. Assuming a multiple of 15 the market cap would be at ₹600 billion while today it is around ₹70 billion. So, on a 10-year horizon, it does have a 5-10x potential.

Venture cap valuation: In 2020, a VC firm Gateway Partners bought 15% of the company for $100 million, valuing the firm at about ₹60 billion. Since then, the revenue has doubled and the market cap is only at ₹70 billion.

Relative valuation : Delhivery, an integrated logistics company has revenue of ₹80 billion, negative FCF and a market cap of ₹320 billion. Comparatively, TVSSCS has revenue of ₹90 billion, FCF of ₹5 billion and a market cap of ₹70 billion.

Company news

Nothing special.

Catalyst

There seems little downside at the current price. Plenty of tailwinds, and the company is ripe for rerating while the business is likely to keep growing. Earnings getting into positive territory, not just cash flow, might be a trigger for rerating.