Background: M.V. Gokarn established Triton Valves (TV) in 1975. In 1978, TV started producing valves for the inner tube and tire industries and emerged as a market leader in the segment. Triton evolved into India’s biggest tyre valve maker as the country’s automotive sector expanded. It became a Tier 2 to Tier 1 supplier to the automotive sector once it started producing tubeless tire valves with the introduction of tubeless tires.

Currently, Aditya Gokarn (son of M.V. Gokarn) is the CEO and managing director of the company.

Why the company is not able to scale up despite rich experience and heritage……?

Aditya’s father Mr M.V. Gokarn suddenly passed away in 1986 due to heart attack. Post which, the company was handled by his mother till 2012. During these 26 years (1986-2012) of consolidation, company did not take any risks or try anything innovative. In 2013, Aditya was appointed as MD and CEO of TV.

Profile of Aditya Gokarn: Aditya Maruti Gokarn graduated with honors from the University of California, Berkeley with a certificate in business excellence and a bachelor’s degree in mechanical engineering from RV College of Engineering in Bengaluru.

Milestones:

1975 – 2010 (35 years): Topline of Rs 100 crores achieved.

2010 – 2018 (8 years): Topline of Rs 200 crores achieved.

2018 – 2022 (4 years): Topline of Rs 300 crores achieved.

2022 – 2024 (2 years): Topline of Rs 400 crores achieved.

Growth accelerated now……

Triton Valve: Established in 1975, it is into Manufacturing of tyre valves, valve cores, TPMS valves and hoses for CTIS. Annual capacity of 180Mn valves. IATF 16949, ISO 14001, ISO 45001

Triton Future Tech: Established in 2020, it manufactures extruded and drawn rods and coils of brass and other copper alloys. This is basically a raw material supplier. So, this raw material is consumed both within group and is also supplied to external customers. Annual Capacity of 8400M.T. ISO 9001

Triton Climatech: Established in 2020, it manufactures valves and components for HVAC applications.

Triggers and Moats:

Triton Valves:

- Traditionally, TV used to supply valves to companies like MRF or JK or Ceat, and they would use their valves to produce tubes. Hence, they used to sell their valves through their distribution channels. Industry is now shifted to tubeless tires in India and the tire valve which is sold through their channel to produce tire tube is now consumable and critical component of tubeless tire because the valve is the tire pressure seal, which actually retains the air in the tire. So now if you have a tire puncture, you also have to change tire valve as a safety protocol. Even if the valve is not failed, it is still recommended because it’s a small cost, but it’s a very critical component.

- Company has developed their own distribution network wherein 2800 distributors have been added.

- Tire Industry: Share of replacement tire is 70% and OEM 30%. Growth in tire replacement industry is at inflection point and will remain elevated.(Tyre sector revenue to grow 7-9% in FY24 with better replacement demand: ICRA, ET Auto )|

- TV commands market share in the OEM tubeless space today in India is in excess of 90% as per the management. |

- China + 1: Company is now talking to a lot of distributors in the US market, European market since post Covid, they are looking for an alternative to China.|

Triton Future Tech (TFT):

- TFT offers several advantages to their supply chain and enables them to tide over the volatility of raw material prices.

- Easy to scale up this business since the triton valve and climatech is based on heavy engineering…

- Demand for brass coils and copper alloys remain elevated due to wide range of applications:

- Transition from IC engines to electric vehicles and hybrid vehicles, the content of copper alloys and the content of brass in these vehicles goes up very significantly because brass is basically an alloy of copper and zinc.

- Used in making watch parts, LPG valves etc.

Triton Climatech (TCT) – Hidden Moat (Long way to go….)

- TCT caters to climate control air conditioning space. Manufactures components for split air conditioners and commercial air conditioning applications.

- Its one of its kind product, not even a single competitor in the Indian market as per the management.

- Lennox a U.S. giant in air-conditioning and heating solutions with a market cap of over $17Bn is now dealing with TCT. Launched new range of products for them. Since they have already cracked a bigger U.S. brand, it’s only a matter of time that the company may onboard large players like Carrier, Bryant…

- Company has already started engaging with Trane technologies and Carrier.

- However, it will take time to accelerate……may be 3-5 years to scale up(requires stringent testing and validation to scale up)

Currently, Climatech topline is somewhere around 13cr with negligible utilization……can achieve a topline of Rs 200cr plus with optimum utilization.

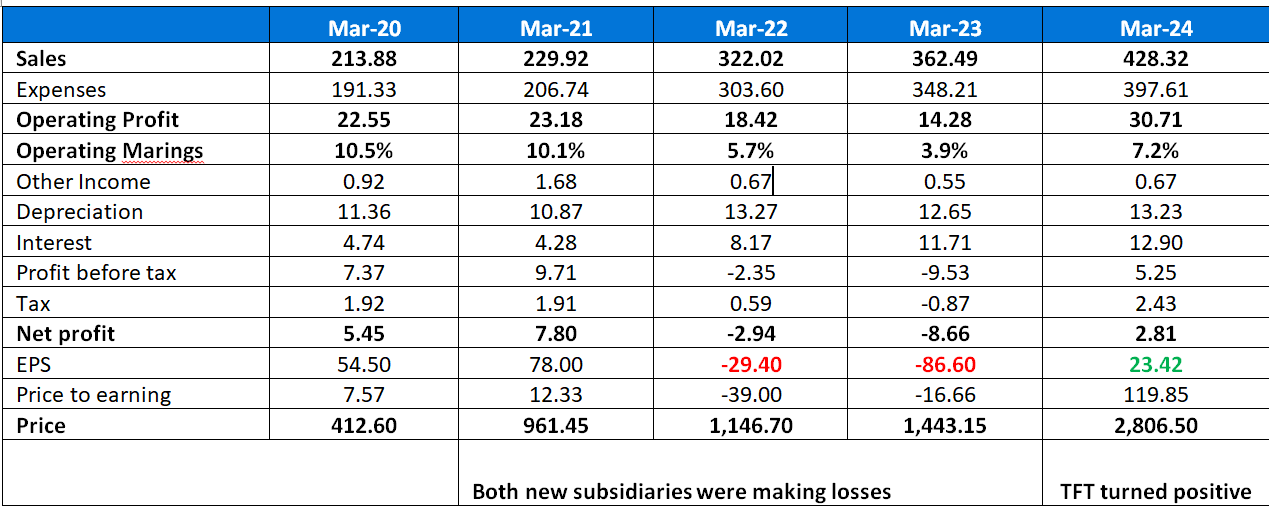

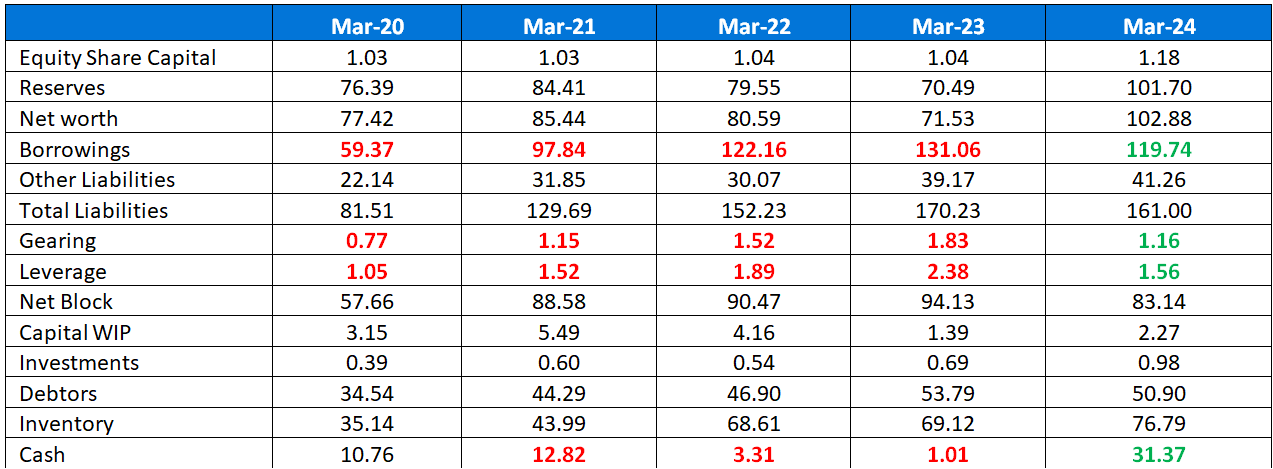

Financial Snapshot:

After a long time, improvement can be seen in the financials of the company.

Negatives:

• Thin operating margins and debt is still on a higher side

• No investor presentations and con-calls.

• Element of cyclicality in the business.

Positives:

• Being a microcap, top quality of auditor i.e. Deloitte Haskins with quality disclosures.

• Growth is coming back with improved margins

• TFT is now turned profitable in Dec’23

• Beneficiary of China plus 1

• Transition of IC to EV is beneficial for the company.

• Fund raised executed recently @Rs 1740

• Promoter Holding is consistent about 52.85 % with no pledged shares

• Market cap to sales is less than 1.

Disclaimer: Above study is for educational purpose only and not a buy sell recommendation by any means. Invested and biased.