Trident Techlabs Limited, formerly known as Trident Techlabs Pvt Ltd, is a technology solutions provider catering to industries like aerospace, defense, automotive, telecom, medical, semiconductor, and power distribution. The company’s 24th Annual General Meeting is scheduled for September 27, 2024. In November 2024, Trident Techlabs shared an investor presentation and held an earnings call to discuss the unaudited standalone and consolidated financial results for the half-year ended September 30, 2024…

2. Five-Year Financial Highlights

Here’s a summary of Trident Techlabs’ financial performance over the past few years:

Particulars (₹ in crores)

FY21

FY22

FY23

FY24

Total Revenue

28.3

29.8

68.1

73.0

Net Profit

0.5

0.6

4.6

9.3

Equity Share Capital

2.8

2.8

2.8

17.2

Reserves

9.9

10.5

16.1

29.2

Borrowings

30.4

29.6

22.9

19.2

Other Liabilities

15.9

12.5

7.9

32.9

Additional Financial Highlights

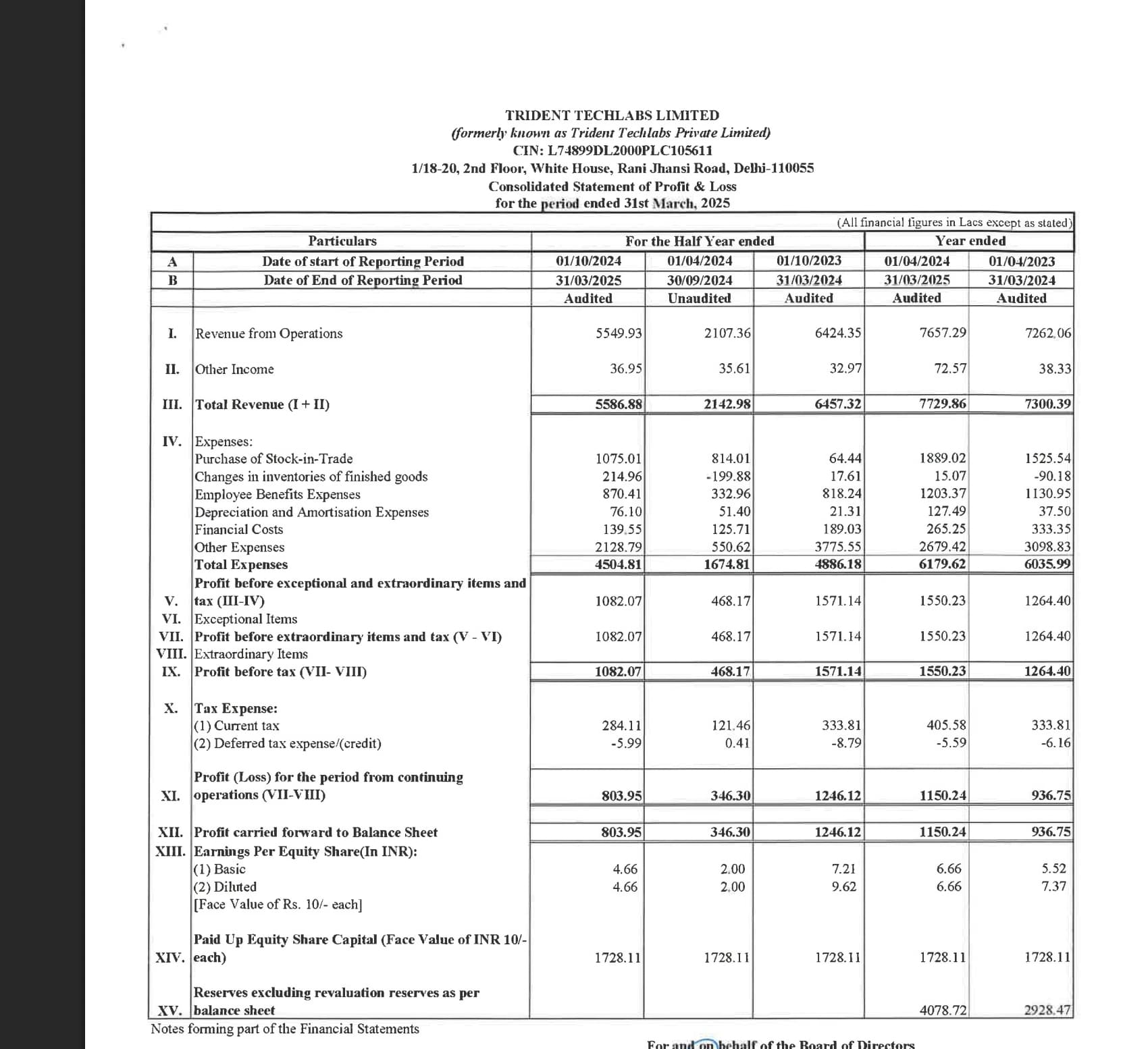

H1 FY24-25 Performance: The company reported a total revenue from operations of ₹2107.36 lakhs, a significant increase from ₹837.71 lakhs in H1 FY23-24.

EBITDA: ₹645.27 lakhs in H1 FY24-25 compared to a loss of ₹-146.22 lakhs in the corresponding period last year.

PAT: ₹346.3 lakhs in H1 FY24-25, a substantial turnaround from a loss of ₹-309.37 lakhs in H1 FY23-24.

Key Financial Ratios (as of March 31, 2024).

Ratio

Value

Trade payables turnover ratio

0.20

Net capital turnover ratio

1.71

Net profit ratio

0.13

Return on capital employed

0.24

3. Business Segments

Trident Techlabs operates in two primary segments:

Engineering Solutions: Focuses on system-level and chip-level electronics design, with increased demand from the aerospace and defense sectors.

Power System Solutions: Concentrates on integrating power electronics and smart grid technologies, benefiting from the shift towards renewable energy.

Segment Performance

The Engineering Solutions segment has shown strong performance, particularly in system-level and chip-level electronics design. Consulting and engineering services have gained traction, enabling clients to innovate across the product development lifecycle.

The Power System Solutions vertical has experienced steady growth, especially in the integration of power electronics and smart grid technologies. The shift towards renewable energy and increased focus on sustainability have further bolstered demand.

4. Competitive Advantages

Trident Techlabs has several competitive advantages:

Knowledge-Driven Company: With a 25-year legacy, the company helps clients leverage next-generation technology.

Strong Client Base: Serving over 500 clients, including Tata Power and the Indian Navy.

Global Partnerships: Collaborations with global leaders like Eaton have facilitated expansion into Southeast Asia, the Middle East, and North Africa.

Experienced Management: Led by experienced professionals like Sukesh Chandra Naithani and Praveen Kapoor.

Robust Internal Control Systems: Ensuring the integrity of financial reporting and compliance with applicable laws.

5. Growth Targets and Guidance

Revenue Target for FY25: Trident Techlabs is targeting a revenue of ₹250 crores with a PAT (Profit After Tax) of approximately ₹40 crores.

Long-Term Vision: The company aims to become a ₹1,000 crore enterprise within five years.

Expansion Plans: Trident Techlabs is expanding into new domains like cybersecurity and semiconductors. The company has incorporated a wholly-owned subsidiary in Dubai to support international expansion. They are also targeting Europe for defense and cybersecurity.

Strategies for Achieving Growth

Leveraging Government Initiatives: Taking advantage of government schemes to drive business growth.

Repeat Business: Securing repeat business from existing clients due to strong references and credentials.

Installation Base: Generating assured business from the sizable and growing installation base of software solutions through annual maintenance contracts.

Strategic Acquisitions: Considering acquisitions to enhance capabilities and market presence, particularly in the semiconductor segment.

Management Outlook

The management team, led by experienced professionals, is focused on optimizing business processes, fostering innovation, and aligning teams toward common goals.

They emphasize intelligent deal structuring to maintain healthy profit margins across all verticals.

Opportunities and Outlook

Positive Outlook: The company anticipates strong demand in the aerospace, defense, and telecom sectors.

Power Systems Market: Expected to benefit from the ongoing transition to renewable energy sources and the development of smart grid infrastructure.

Geographic Expansion: Targeting growth in Southeast Asia, the Middle East, North Africa, and Europe.

Risk:

Supply Chain Disruptions: Potential disruptions in the supply chain, especially for critical components in electronics and semiconductors, pose a risk.

Cybersecurity Risks: Increasing reliance on digital systems poses significant cybersecurity risks that need to be managed. The company intends to establish itself as an early player in the cybersecurity market segment.

Intense Competition: The technology solutions market is characterized by intense competition3.

Dependence on external funds: The company may need external funds to achieve its revenue target of ₹1,000 crores within five years.

company has projected 250 cr revenue fy 25 and 1000 cr revenue

in next few years

order book of late is in lakhs reported

It is a SME company listed in NSE emerge

in this market downturn it is coming down very sharply

due to execution concerns

kindly do own study before investing

Disclosure: went through one concall but not invested

Please post in SME general thread also if needed ,some members can give feedback who invested or tracking this

Very informative podcast. Two Hours 30 Min podcast by Mr Ameya who specializes in IT sector gives immense information about the company and its working.

order book less than 100 cr approx 69crores plus few here and there

how they will achieve 250 crores as committed

Jan 6 Raghu panicker of kaynes tech joined trident techlabs as advisor from kaynes and this stock got pumped to all time highs before falling since no big orders are coming

can some one following /invested in TT go and see in linkedin still reflecting Kaynes tech ceo in raghu panicker

is this military secret of techlabs role not reflecting in linkedin profile of panicker

or this panicker is different ?

3. Now again after this update TT again rising

disclosure: not gone through podcast/not invested since there are many questions than answers

this can also be discussed in SME portfolio where many SME stocks are getting discussed

First question has been answered in podcast stating that right now company is getting sample orders which are very small in Rupee terms but if those order fulfillment is satisfactory to the companies then it will lead to big orders. The orders may spill to next one or two quarters of FY 26 also.

thanks for revert.

Disclosure: Invested long back, then exited due to above mentioned queries

it is a high risk bet based on execution ( suitable for those with understanding of business and bet on company execution in future)

even though i donot know much of power /semi conductor( indepth )domain

what a simple check can understand that MNCs/large Indian companies

for example like Siemens have capabilities for power stability/losses and they can grab if big orders come( even unlisted MNCs/indian players can open a new vertical if TAM is so large why should Adani or Tata ignore this?)

semi conductor they announced one acquisition and Mysterious Panicker who is an expert .In social media people who push say he is Kaynes ceo and still he is kaynes ceo as per linkedin

The problem if opportunity is highly lucrative and Orders are big

MNCs like ABB/siemens donot think they leave opportunity

or Indian large corporates listed and unlisted

See paints/cables& wires for example

Iam happy to be proven wrong for the sake of TT Investors

But existing investors particularly new aspiring ones Be aware of

Concerns not just rely info from X or some means

Kindly do your homework since this ( company)is not a easy straightforward case of investing

Hope as per company::

Power TAM 10000 cr /semi conductor TAM 10000 cr

we get some share

revenue projection 1000 cr in 4/5 years

But we need to see Strong execution

Hopes/ things to Monitor

as Transmission picks up we need to see orders inflow in 10s of crores

as Semi conductor plants getting started whether they are getting any design work ( atleast few crores)

Other domains like cyber security not much traction of late

they have unfavorable terms of trades in terms of cash collection. 210-250 days of cash collection cycle(care ratings), and yet they hasn’t wrote off something from that expectations! this might be a risk. Let’s see if they fulfil 250 cr. revenue in FY25, as commented by mgmt.

Just a cautionary note, stock was close to 1000/- at the time of this video by bastion and down to 490/- now and still looks expensive for what they have delivered in last 12 months. while the business and promoters might be good, there seems to be elements which are pushing the prices higher than needed.

Management has guided for 250 cr revenue, h1 they have done 10% of this, h2 they claim to deliver rest. Last year also in h2 they have done 8x of h1. Would be interesting to watch h2 results.

Their disclosures are very discreet. Don’t usually talk explicitly in concalls also. Their OB ranges from very sensitive areas of DRDO and niche Defense catering. Not so on manufacturing of products but design and engineering which are mostly NDA’s with GOI. Maybe those exciting/subdued surprises keeps their valuation tight high!!! any thoughts?

The order book execution period is limited to 90 days, followed by a 3-year Annual Maintenance Contract (AMC). The AMC component is expected to constitute a maximum of 10–15% of the total order value.

Yeah. It’s a huge miss. FY25 guidance was 250 Cr. but they could only manage 77 Cr providing this H2 heavy business & management wanting to move away from seasonality.

"Further to our earlier communication dated December 24, 2024, we wish to inform you that the Letter of Intent (LoI) entered into by our wholly owned subsidiary, Techlabs Semiconductor Pvt. Ltd., for the proposed acquisition of the Sivaltech Group (comprising entities based in the USA and India), has been

cancelled.

Techlabs Semiconductor Pvt. Ltd. had been in advanced discussions with Sivaltech Group for the acquisition of equity, with a view to making Sivaltech group our Subsidiaries. However, during the course of final negotiations, the promoters of Sivaltech group proposed certain transactional terms that materially deviated from those outlined in the mutually agreed LoI.

After due diligence and careful evaluation, it was decided to discontinue the acquisition process.

Techlabs Semiconductor Pvt. Ltd. has since redirected its focus and is actively exploring other promising strategic opportunities. Any material developments in this regard will be duly disclosed to stakeholders in accordance with applicable regulatory requirements."

Company would obviously not say it frankly but after the cancellation of preferential allotment due to backing off by investors, they would be short of funds for aquisition which may have led to its cancellation.