Along with above, i think, we need to consider present and expected future growth of the business , which are also very important.

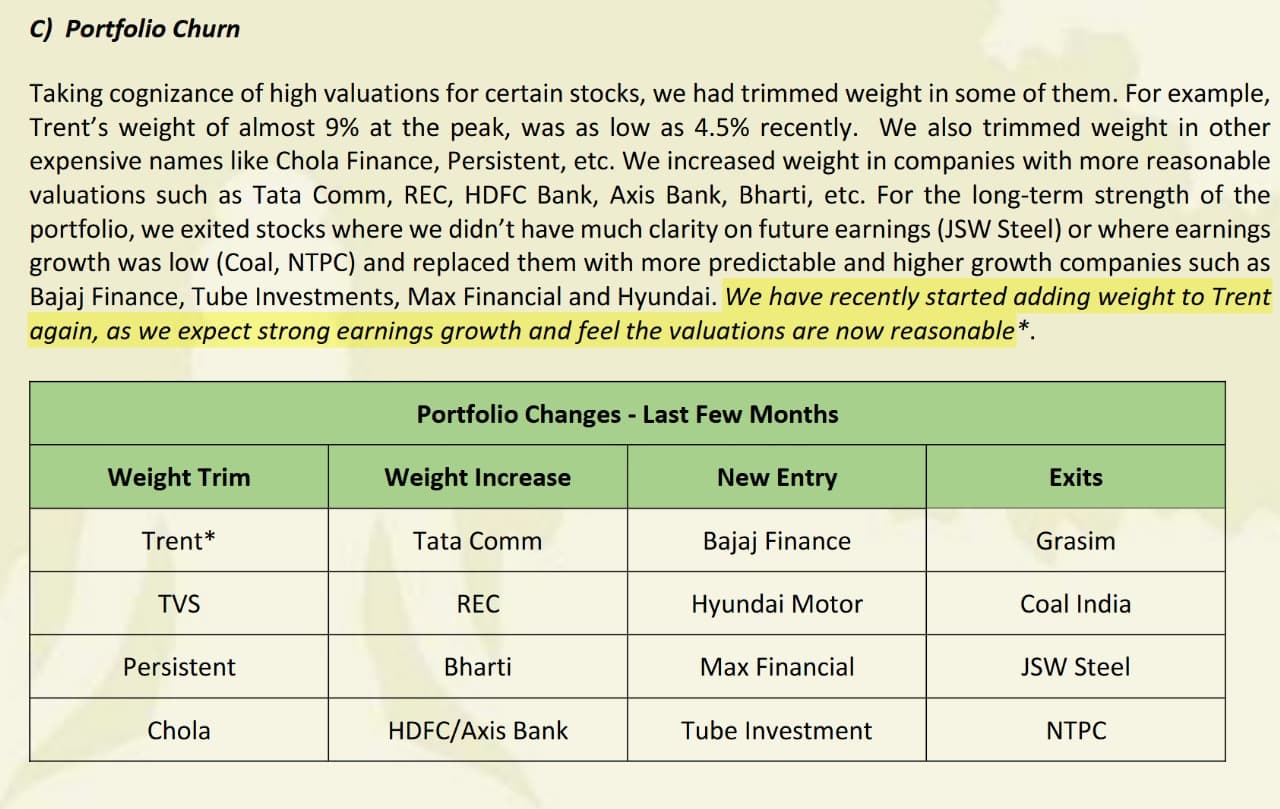

Yes, The present consolidated growth is now reduced to 27%. Noel Tata’s comment in recent Q4 results announcement- “Both Westside and Zudio now have the scale & reach and enjoy significant consumer awareness & love” gives a subtle feeling that future stores additions will be slow in fashion space. However his comment on Star -"The opportunity in the food space for the Star proposition is exciting while being competitive. We remain convinced that this business is well poised to deliver much consumer value and growth in the years ahead.” indicates that the growth driver might be Star. Let us wait for annual report to assess the management commentary, future growth plans etc. before adding further in the position. The market cap of Trent has multiplied 10x in just 5 year, hence one should not have very high return expectations. Trent still is a good long term bet, provided we choose the entry point(valuation) carefully.

2 Likes

Bet would be in Beauty space, I think. Z Beauty they have started expanding. And beauty space as a segment of retail is fastest growing sector of maket.

Star is at inflection point. Sort of like Zudio was in 2018. Rapid growth is possible

1 Like

@Devsuman I think that was to talk about the sheer profitable scale it has achieved & now it is about just expanding.

With “awareness & love”, they need to

i) replicate the playbook city by city, town by town

&

ii) expand into different categories. As @hardik_shah1 highlighted, one of them is Zudio Beauty.

There are many uncharted categories where Trent can do wonders & market actually needs that.

I visited flagship Westside store (SoBo Kala Ghoda) a couple of days ago & they are able to sell Jewellery (imitation & POME both), blazer, Home Decor, Small categories (but in good numbers) like scented candles, keychains, towels, bags/wallets etc.

Apart from that, with “awareness & love”, they now can scale brands in categories (& maybe standalone stores for some) like footwear, Fashion Jewelley, Men’s fashion (see what Snitch has done), athleisure, etc.

Do keep in mind that they have plans for innerwear as well. They have a JV with “MAS holdings” for this segment.

With “awareness & love”, they kind of have ZERO marketing costs & significant advantage compared to all other players.

The Kala Ghoda store has a Starbucks inside it.

May be they can come back of “premium food”. We know they are interested in this because they have tried this before with “GourmetWest”.

This is going to be a big business. Reliance is in this segment with “Freshpik”, Spencers with “Nature’s basket”, “Magson”. All of them are finding it difficult to bring customers to pull customers & achieve scale. Westside with its stores can do that.

With Star, seems like they are becoming Aldi of India. (Here, maybe I am think too much, too fast)

They are creating brands in categories where now other retailer has tried before.

Brands like Smartle (Amazon Solimo of Star), Shubh Anand can be a great win, given scale is achieved.

(They have launched a new app for STAR. A good improvement finally, signals confidence of management)

Apart from these, they have Samoh, Utsa.

Please do share your thoughts on this.

3 Likes

When Zudio growth started, Westside was already a well established model in fashion for Trent. In Grocery, Trent is yet to prove itself since years. I read this Q, Star SSSG also slowed down.

So cannot say when Star growth will be possible. Zudio was an open arena opportunity segment while Grocery at different price points is already crowded.

Westside and Zara partnership were excellent precedents and learning refining business model engines for Zudio.

Considering all this, beauty and accessories look better growth engines for now than Star….but hey who are we to even judge decide let alone understand it. Who knows what story lies for Star ahead….

Disc: Invested hence biased/Critical. Transactions recently. Not a buy sell recommendation & not eligible for any advice. I can be wrong in all my assessments.

2 Likes

SSSG is down for most retailers in F&B. Reliance Retail also shows that.

But yes, Beauty and Imitation will be bigger at a profitability standpoint if they get the format right.

2 Likes

Well agree, As a believer in Tata’s strategy, as a best case scenario, I think what they are doing with Star currently is building a base model and ecosystem right in grocery…just like how they did with Westside in fashion.

The Zudio of Grocery might look very different from the Star of today. But for the Zudio of Star to emerge (that is if at all it does), the Westside of Star must be formed first…and that in itself looks like a herculian task so far because of intense competetion amd hardly any sweet spots…the sweet spot of premium consumers is partly (or maybe even largely) taken over by the rise of convinience from QC.

In a way it maybe good that Trent did not over expand Star in last few years as they would have got bigger QC impacts then. Thats what I like about this management.

So, in short, we do not know when and in what form the business model ripe for stupendous expansion would emerge in grocery for Trent…but what I know, that sooner or later it must (may not be as high growth as fashion)…that is if they want to continue in Grocery.

Disc: Invested hence biased/Critical. Transactions recently. Not a buy sell recommendation & not eligible for any advice. I can be wrong in all my assessments.

1 Like

As of now, Trent Ltd has not publicly disclosed an exact number of Zudio Beauty stores planned for the next fiscal year. However, multiple reports confirm that after launching the first Zudio Beauty store in Bengaluru in late 2024, the company is planning to expand into major cities such as Gurugram, Pune, and Hyderabad. Zudio Beauty is positioned in the mass-priced (affordable) beauty segment and will primarily compete with the following brands:

- Elle18 (Hindustan Unilever)

- Sugar Cosmetics

- Health & Glow

- Colorbar

The overall India Fast Fashion market is valued at USD 13.5 billion in 2025 The total Beauty & Personal Care market in India is projected at USD 33.08 billion in 2025 The cosmetics market (makeup, skincare, haircare, fragrances) is valued at USD 14.6 billion in 2024 Industry sources and market trends indicate that 60–70% of beauty sales are in the affordable/mass segment , given India’s price-sensitive consumer base. * Affordable fast fashion apparel is currently bigger than the affordable beauty segment in terms of revenue in India (2025). - Both markets are expanding, but fast fashion is growing at a faster rate, driven by youth demographics, urbanization, and rising disposable incomes.

- The beauty market overall is larger, but when focusing only on the affordable/mass segment, apparel edges ahead in 2025.

Let us wait for the annual report to understand the company’s future plans in these segments.

1 Like

So they have five stores currently. I imagine they are currently in the launch and fine-tuning phase. The website currently does not have any options nor can you shop. It looks like a holding webpage.

We need to figure out whether they compete with Nykaa of the world. Does Elle have any stores, or is it just an FMCG-like brand selling at local outlets?

Health and Glow stores are extremely cluttered. They worked for 20 years, but it’s unclear whether they will work now. From the outside, the Zudio Beauty store looked cleaner and functional, sort of like a Nykaa Luxe store. (All husbands need to accompany their wives, right?). So once they figure out the format size, set up, and merchandising right, it should be easily expandable.

Also, does anyone know why Nykaa has such low OPM when BPC is supposed to be a high-volume and high-margin business?

2 Likes

Hi @Devsuman

My wife visited one of two Zudio beauty “Shop in Shop” outlets in Bangalore on a Saturday.

-

She bought a bunch of lipsticks for our niece, because they are sharply priced. (At 150 Rs I could only find local products, not branded on Amazon)

-

There was no other product.

-

No people. [Feedback was that the customers find the lipsticks elsewhere too.]

The rest of the store was active.

-

Any idea on the LGD business? Have to visit that store still.

-

Are you increasing your holdings given that the price seems to have stabilised at 5K levels?

Where was this Zudio Beauty store located?

My wife was told they are still in the Shop in Shop stage.

I hope they don’t make separate stores, because I think margins on the assortment can be better managed rather than on a single product line.

[Unlike you I am still stuck in the Wodehousian era where I sweat in the women’s section!]

1 Like

I can only echo @Investor_No_1 views on Star.

In D Mart filings the margins on grocery was pathetic. They were making money selling apparel & footwear.

Godrej offers something on the premium end & there is a chain - Namdhari, in Bengaluru where I saw a surfeit of Korean stuff (Kia factory, not near mind you)

Big Basket is unfortunately held by Tata Sons!

I fear it is becoming like Fastrack watches & belts. Visible but not seen

1 Like

In Ahmedabad they are at Shahibaug. Banaglore i have no idea.

Well the thing is whether u sweat or not, you have to accompany to hold the bags. Closing the joking portion here as it does not add anything to forum.

it was not a shop in shop, but a dedicated stand alone Zudio Beauty store?

What other products besides lipsticks?

Yes, it was an stand alone format store. Please do not ask me details of what was available. I cannot differentiate between a lipstick and a kajal, but major categories were covered. I think it was around 600-800 sqft and had the entire range like Nykaa.

There is one standalone opened in Virar Mumbai as well.

@SwamiR for store & product details, easiest way is to search on youtube. Gives you rough idea about product, asthetics, experience, products & prices.

The limited collection you was might be because of SIS set up.

One I could find is: Zudio Beauty Virar

The standalone store covered here has a wide collections of products.

1 Like

Zudio Beauty is simply a rebranded version of Trent’s old Misbu stores, which they shut down in mid-2024. The same five Misbu stores had pretty average ratings on Google Maps (between 3.1 and 4.0).

Unlike clothing, this is a difficult market to crack, so they are trying to piggyback on the Zudio brand name to attract customers.

3 Likes

u r saying they only had lipstick category in the entire store?

also please explain “No People” … are you suggesting there were no other customers?

Hi Swami,

I do not decide on price movements as I do not understand technical charts etc. I am waiting for the annual reports to understand the management’s future plans and how they are looking at future prospects. After reading the report if I feel that this is still a 30% growth engine I will start adding slowly some thing like SIP and with a minimum 5 year horizon. If story does not appeal me I will start cutting my current position and start adding to better growth engines available at good valuations. In my opinion Trent is still expensive looking at current growth dynamics. I am conservative in terms of valuations and I keep a good margin of safety.

Disclosure: This should not be considered as buy or sell recommendation. I am invested in Trent. My views are biased and my knowledge is limited. I am not an expert nor a SEBI registered advisor. I can be completely wrong in my assessment, I have been wrong many times

2 Likes