I have been trying to dig around Tree House and the fall of its stock price to abyss, but have not been able to touch on something concrete. However, I can infer the following few things that might be ailing this stock (but maybe not the business). A few of them might be already obvious, but still putting them in writing.

Cooked Books:

I am starting to be concerned about the possibility that THEAL has greately manipulated its numbers and heavy investors are finding out about it. This can be the worst case since all the analysis performed on this company goes for a toss if the numbers were misreported. However,if this true, then how come major shareholders have not been aggressively selling inspite of the price plummeting? Imagine what will happen if they start off loading their shares! :-o

Poor Promoter Quality:

Based on the trail of events, it is almost assured that Rajesh Bhatia hardly belongs to the league of Quality management. All events since mid 2015 reek of fabrication and RB has hardly provided any explanation, other than some appeasing statements. The market has been severely punishing a stock even if it gets a hint of mediocrity in the management quality (eg Kitex) and THEAL has spared no stone unturned in providing those reasons. Also, if the merger does go through, is the Zee management capable enough to take this blemish off THEAL? Hardly, because RB is still going to be the CEO of merged entity!

This being said, I recollect words of Peter Lynch, “Go for a business that any idiot can run – because sooner or later, any idiot is probably going to run it.” and Pat Dorsey using the adage “Bet on the horse, not the jockey.”

In all this fire and smoke around THEAL, its fundamental business still seems intact (I doubt if most of the parents whose kids go to TH have even heard of the merger and pledging and swap ratio. All they care is if their children are going to a good school!)

3)Pledging:

I do not understand the intricacies of how pledging works and how it can severely affect a stock. If a call margin is stuck, (lets say at Rs200) and lenders sold their shares, shouldn’t all their stake be already taken care off by now? How come price is at Rs73 and still the pledged shares are being sold? If someone can shed light on how the pledging has affected THEAL, than it will be a great insight into its predicament.

4)Merger/Valuation:

The merger was not welcomed by most of the THEAL shareholders when it was declared in Dec, 2015 because of the unfair swap ratio. I can understand investors selling their stake in the company once this decision was made. But at current prices of THEAL = Rs73 and ZL = Rs30, the swap ratio of 53:10 shows that THEAL shareholders will get Rs1590 and ZL shareholders will get Rs730! This is clear arbitrage opportunity! Since the tables have turned, ZL shareholders might now oppose this merger or ask for a new swap ratio.

Those are my few pennies. Hoping to get more insights from the rest.

I agree. I find Tree House promoters constantly selling their shares in open market and buying back. They themselves are shorting their stock and buying back at lower prices. They seem to be making more profits that way than running the business. I have limited money, why invest it in dubious companies management which is known openly. Invest only in sound management and even then there is a 10% probability that we may go wrong…

@cool_aksh - Let me try to explain the process of pledging and de-pledging in a simpler manner. Pledging & de-pledging happens at depository participant level (DP) where the person is maintaining his/her Demat account. Pledging happens when a person wants to keep his shares as collateral, usually against a loan taken or a guarantee.

Pledger is the owner of shares who gives shares as collateral. Pledgee is the person in whose favor pledging is done.

Process - The person holding shares in his demat account gives an instruction to his DP initiate a pledge in favor of pledgee. This instruction slip contains all the details including the name, number of shares to be pledged etc. Also the details of Pledgee, his DP & account number is also mentioned in that slip. Based on this instruction, DP mark the shares as Pledged at its back office system. Once the shares are pledged, it will remain in the account of account holder only but will be marked as pledged. This means that the owner cannot sell the shares unless the same is released by pledgee. All corporate action coming during the tenure of this pledge period will go to the owner as in normal situation.

De-pledging - Now at a later stage, If the pledger replay his debt, pledgee will give a request to his DP for releasing those shares. After such release, the share will be free and this completes the whole pledging – depledging process.

In any exceptional situation where pledger defaults on loan/commitment, pledgee can invoke the shares. Once the shares are invoked, the pledged shares will move from pledger’s account to pledgee’s account as free shares available.

Date Company Client Tran Qty Traded Price

22-Feb-2016 Tree House (BSE) MATRIX PARTNERS INDIA INVESTMENT HOLDINGS LLC SELL 2125000 80.04

22-Feb-2016 Tree House (NSE) POLUS GLOBAL FUND BUY 1726403 80.00

22-Feb-2016 Tree House (NSE) MATRIX PARTNERS INDIA INVESTMENT HOLDINGS LLC SELL 2172526 80.30

I am a beginner. I have done the following calculation and want to ask the experts here if these calculations are right. Today’s CMP of Treehouse is ~86 and Zee learn is ~31. The agreed merger terms is that for every 10 tree house shares you get 53 Zee shares. if I buy10 Treehouse (850 cost price), I get Zee shares 53*31=1643. Assuming that I can swap today I can make a cool 93%. But I have to wait.

The key risks

Dont know if the merger will go through. (what is probability that it may not go through 10% or 90%)? I have no clue.

Lets assume that the merger will go through. Will it happen next month, next qtr or next year

Here on Zee learn keeps going south rapidly and out of sync with THEAL

Original tree house investors trying to exit immediately after the merger

The first two are the key risks in my opinion.Assume that everything went through as is, the original THEAL shareholders would like to sell and get out and hence there will be big sell orders on the immediate first /second day after merger. and say I somehow still get to sell Zee learn shares @ 25 (-20% of 31), I still make a profit of (25*53-850)/850=55%

As long as the two companies share prices move in lock step up or down, people should still make the same kind of gain right? Is this kind of arbitrage/special situation that Graham talks about?

The calculation seems alright. But even at 31 rs Zee Learn seems hugely over valued.

Before trying to take the advantage of the arbitrage one has to evaluate the valuation of zee.

Question is. Forget about the merger.

If you have to buy Zee Learn today. What will be the fair price.

I have not studied Zee Learn but looking at track record low roe debt etc looks like the share price should be less than 10 rs.

I can be wrong off course.

What about the networth of Tree House? Post merger it will become Zee Learn’s and hence the Book Value of Zee will be ~30 Rs. Correct me if I am wrong.

Theoretically arbitrage opportunity exists if we are sure the merger goes through. But we got to remember that Zee stock is essentially getting diluted and if the books aren’t good or some write-off happens stock will fall.

If we know to certain degree good information that merger goes through, then the best way I think this can be played is to do pair trading

For every 1 stock of tree house buy, short 5 shares of Zee learn. if the merger goes through, then you can always cover the 5 stocks of Zee Learn you receive from Tree house. Essentially, you are covered here because, any upside in Tree house will be benefited. Any downside of Zee Learn after the merge is shorted already

Hi Jeswin

Imo we should not go merely by book value as there may be corporate governance issue in Tree house or maybe even in Zee learn. For safety sake you may like to discount the intangibles and a percentage of receivables from Tree house balance sheet to arrive at book value.

After the merger Zee learn book value will increase but the equity will also increase.

At present prices and assuming the merger goes thru it doesn’t make sense to buy Zee learn when you can buy Tree house at 86.

But if the price of Zee learn falls to 15rs or below then the arbitrage advantage will disappear.

My question remains same. What makes us believe that Zee learn price will not fall below 15. Prima facie it looks very expensive to me. However if someone has tracked the stock. Knows about the products expansion plans. Likely revenue and profitability going forward then he can make an educated guess and decision.

Deciding purely in stock price or screener may lead to opportunity cost.

hey @inxs_22in thanks for explaining the process. I have one doubt here.

"All corporate action coming during the tenure of this pledge period will go to the owner as in normal situation."

If this is the case then there is a chance of gaming the system. Say I pledge my shares and then issue dividends to myself on the pledged shares, which will come in my account even though the shares are pledged in the name of the lender. this will lead in reduction of the share price but i hardly care because I am making money on the dividends of the pledged shares.

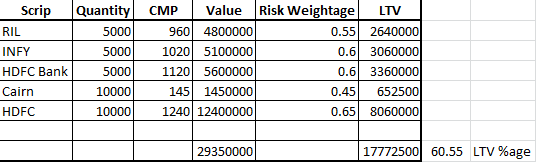

In case of Security based lending, lender usually give a loan value after deducting a haircut of 40-60% depending on shares. If the shares provided as collateral are big blue chip shares, the haircut is around 40% and in case of small caps, its 60% or even more (It varies from company to company).

For example – If the value of collateral is 100 and the shares provided are blue chip stocks like infy, RIL etc., A loan of around Rs. 60 will provided against it. The LTV of individual scrip is determined by Risk management team on the basis of various risk parameters like liquidity in that share, diversification of collateral portfolio provided etc. and the whole process is system driven and executed automatically using Risk management applications.

Example

Pledger → Collateral Portfolio → Pledgee

Collateral Portfolio

Now coming back to your question – Payment of dividend usually impact the value of a share upto an extent of the amount of dividend paid, which is usually very insignificant i.e. not more than 2-3% in large caps. So this haircut on shares usually takes care of this volatility. On a day of exceptionally high volatility (Like Budget day or on the day when scam of Harshad Mehta/Parekh/Lehman was unearthed) and the value of overall portfolio tanks drastically, The lender uploads intraday bhav copy in his system to ascertain the latest LTV and in case it dips below 80% a margin call is issued to Borrower wherein he is required to replenish the shortfall. In case, borrower fails to do so within stipulated time, Lender invokes the share and sells it in open market.

This is the usual process followed by companies which are into Security Based Lending. The process may slightly vary from company to company depending on their internal policies and risk appetite.

Thanks Mukesh @inxs_22in for explaining the pledging/de-pledging process in detail but I’ve more doubts and need to understand it in more detail to take advantage of the special situation of distress buying it offers incase of trigger of margin calls sell off by the lender to recover their loans. I’m not sure though if this is the right thread for detail discussion or Shall I start a new separte thread for the benefit of all?

You won’t be able to take advantage of such special situations legitimately for the following reasons-

Everything happens so quickly (in less thn 12-24 hours) that as an outsider it’s next to impossible for you to get information about it and consequently act upon it.

Even if you are insider or have access to the information pertaining to it, any trade executed in your own account prior to such action would tantamount to “Insider Trading” which is not legitimate.

The information gets public post the crash in share price has already happened and in such cases, “The art of valuation”, as explained in a separate thread by @Donald sir and other experts, comes into play. While most of people stay away from that scrip as it has fallen steeply, only a handful of investors who actually know the worth of shares and can manage their “fear” part can take positions and take advantage of such special situations.

Although I have tried to answer all your queries in my posts but still if you think that this can be explored further, you may start a separate thread.

does this mean 100% of rajiv and geetas shares are pledged? and who is this hamlet media ? what a fall from grace. my biggest lesson learnt : corporate governance cant be blindly trusted. check and verify at all times.

100% shares pledged by Bhatia’s might be the last nail in the coffin for this stock.

Hardly any information is available on Hamlet Media Pvt Ltd. Below are few links, but they don’t provide much information other than it is Delhi based.

Based on some rough calculations, the Bhatia couple has taken loans worth around Rs 26 crore!

Below is the math for all the pledged shares. I have assumed a CMP of Rs 75 and haircut of 60% as explained by Mukesh earlier.

(3683136 + 356500 + 1390833) x (Rs 75/share) x (40%) = Rs 25,91,69,070

Hamlet Media has disclosed about Bhatia’s shares being pledged with them…

Really Murky, why would the Bhatia’s again pledge 100% of their shares? Not sure if the money raised from pledge is used for THEAL and most likely they are running parallel business…

Consider the merged entity.

After merger zee learn will have 2070 play schools and 111 k-12 schools.

After merger there will be about 54cr shares.

At current price of treehouse of Rs.75 and conversion ratio of 5.3

Average price of the entity will be 75/5.3 = 14.15

The nominal value for a treehouse shareholder will be 14.15 X 54 = 764cr.

Now combined entity is debt free. Revenue of 350cr and two strong brand names of Kidzee anx Treehouse.

The price seems to be a good time to enter the stock.