Market always overreacts in the short term …if it were correct all the time,then we would not have any gains to make or loss to take . It does not prove anything eitherway .

Disc. I am also invested and roughly this stock is my worst performer ever since I started . ;}

5 Likes

Such over-reaction from retail investors is unwarranted and it shows what an easy target we are for sharks and institutions who snatch our long term holding shares with a bit of panic and negtive sentiment. We act like sheeps and we forget what made us invest in these companies. Our “why” should be strong enough to help us get through these short term volatility while holding our shares.

Unless we have the balls to digest a 30-50% fall in a quality stock, we may never be able to generate wealth from the share market. A great investor accumulates in a great company during a difficult time in the company; not sell and run away in panic.

10 Likes

Don’t they have to inform the exchanges? I didn’t see any such intimation.

That fire incident+bad quarter(not sure why)+WB bribery incident. Not good.

Discl: Invested.

1 Like

I listened to the concall and the managament was surprised that a 4 years old matter cropped up regarding the World Bank order for which the company already received 90% paymemnts in 2022 as well and the remaining this year in May. Also, the company said that they did not receive the notification dated July 30th from the World Bank. Which fire incident are you talking about?

1 Like

I think that tgv sraac transformer that burnt its coil and stopped production.That was mentioned here somewhere in the thread .On a lighter note ,to satisfy investors all car companies should also notify the exchanges about any accident that takes place if they built and sold the car . ;)

2 Likes

Investor Presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/41686dc2-32a5-4975-9453-8af33a72d8ff.pdf

Conference Call Audio: https://www.transformerindia.com/wp-content/uploads/2025/11/10037936.zip

- Margins were impacted because of the last batch of low-margin orders and lower capacity utilization.

- Order Book & Guidance:

₹5,472 crores in unexecuted orders, mainly from national and state utilities.

Around ₹1,600 to ₹1,700 crores of this is expected to be executed in the next two quarters.

Full-year revenue growth target of at least 25% over FY25, aiming for around ₹2,600 crores in revenue and a 16% EBITDA margin.

Expects a stronger H2 FY26 as supply conditions normalize and plant utilization improves. Capacity expansions, including new plants, are progressing (one slightly delayed due to monsoon and equipment issues).

World Bank issue:

No current or upcoming orders are funded by the World Bank. All projects for the World Bank (notably TCN Nigeria) were completed years prior, with all payments received by early FY26.

The World Bank has recently debarred the company from participating in its tenders.

Special duty transformers:

High inquiry pipeline (₹400-500 crore) for special duty transformers.

Only qualified vendor alongside one global competitor; sees strong growth opportunities.

Project Delays

Most of the revenue cut is due to raw material supply (CTC and bushings), not capacity delays.

Supply normalization and new plant production will mitigate issues next year; positive long-term outlook maintained.

FY 2028 aspiration:

Backward integration (new plants for CTC, bushings), supplier risk management, and diversification are core.

Expansion delays mainly weather-related; robust plans to meet FY28 target.

ESOP:

- ₹3.76 crores provisioned for ESOPs.

.

Disclosure: Invested, what I will do next, not sure.

3 Likes

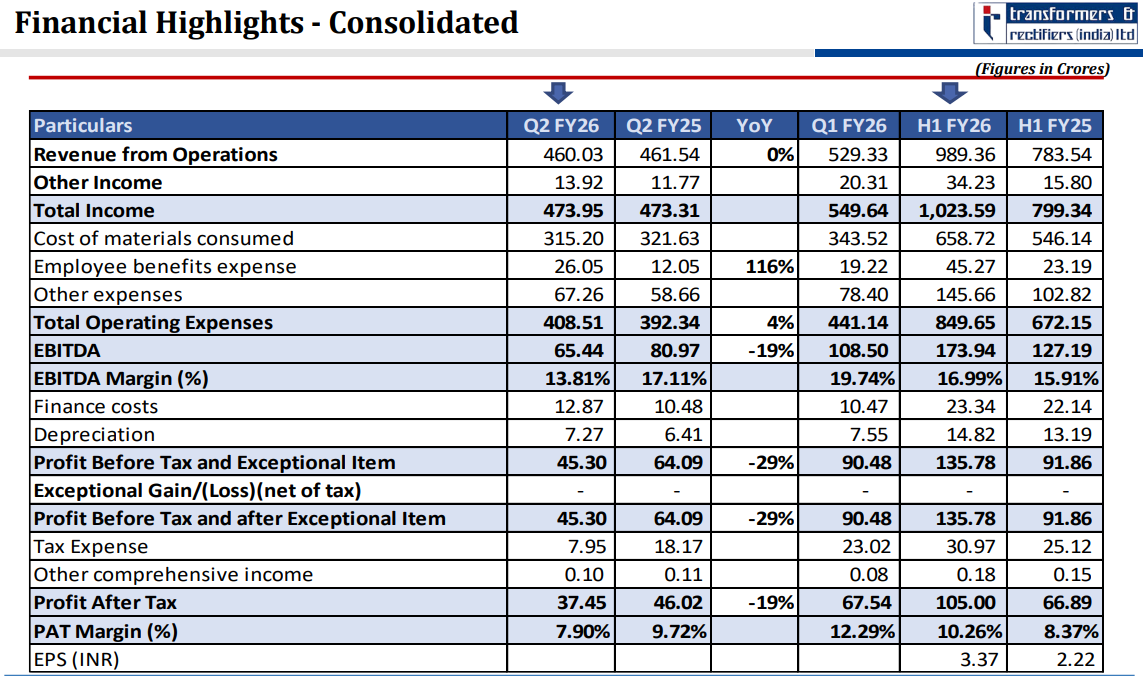

In result PDF (https://www.bseindia.com/xml-data/corpfiling/AttachHis/e225ab62-4415-4cc9-8c4c-826a1215e0a6.pdf) the cost of material consumed indicates 467 63.

Whereas in ppt it says 315.20?

Am I missing something? Thx.

1 Like

how are they supposed to reach the expected topline of 3500 Cr for FY26? First two quarters is barely 1000 Cr and long way to go from here.

Disc: Popped up in my screener growth query and tracking with no position

1 Like

They’ve reduced the guidance to 2500 Cr

1 Like

As I said earlier, wealth can’t be made from share market without conviction to hold and add shares during a difficult time in a great company.

World Bank debarred and removed TARIL within a week. This looks like an opportunity created by institutions to create panic among retail investors and snatch their shares at a cheaper price.

Unless we have the balls to fathom 40-50% decline in a share, we will continue losing money and let go off opportunities to build wealth.

Disc- Added more shares at 313 and 283 on LCs and increased my holding in TARIL to 3% of my portfolio.

8 Likes

Taril order book now at ~6,000 Cr. Q2 got affected by the monsoon – execution basically went on paid leave. Management still guiding 2500–2700 Cr for FY26 if H2 behaves. Infra veterans – roast or confirm?

Big question: topline 8,300 Cr by FY30? Grid backlog looks insane… doable or just another PPT dream?

Added in the dip. Now ~6% of PF. I’ve never had a Monday-morning hangover… but this drawdown must be what it feels like.

5 Likes

This is not a stock-specific question, but TRIL is a useful example because it has corrected quite sharply recently. The negative news has been resolved, yet the stock continues to trend down and has fallen by almost 50%, which means it now needs to double just to recoup the losses. In such a situation, what mental model do investors rely on if they decide to continue holding the stock?

Had there not been any specific negative news and, instead of a sudden 40% drop, the stock had drifted down more gradually. In that scenario, would you have chosen to exit the position at a particular level to book profits or cut your losses, rather than continuing to hold?

Disclaimer: Do not hold the stock but tracking closely.

2 Likes

Order book still sitting at ~6,000 Cr, fresh inflows continue (latest ~400 Cr just last week), enquiry pipeline north of 18-20k Cr, new Moraiya plant commissioning in next few months, management still talking 15-16% kind of margins once utilisation kicks in. Honestly, on paper nothing looks broken… feels more like sentiment doing all the heavy lifting on the downside or something is broken off the paper which we dont know !!

Adding a little more this week, average was already decent.

(Still ~6% of PF, no complaints)

4 Likes

There is no fundamental issue with the company at all.Only thing is the market sentiment is totally negative on any company having anything to do with government capex and the theory is being peddled that because gov has reduced GST,they will have less revenue and hence less money to spend on capex. Delays in JJM,and Kusum etc. has given some support to this theory. On top of that , all good things are painted as bad with ingenious tricks of selective nitpicking.

One may or may not believe in it but the sentiment is presently very bad and its difficult to be sure what will turn it around( rate cut, tariff reversal ?) .Plus there is also an argument in favour of smallcap to largecap rotation. IMHO, its nothing but retail individual throwing in the hat after 1.5 years of non performance and perhaps loss of capital since a very large percentage of small and microcaps are down more than 50% from top .

In my case, Taril goes on my record books as the highest loser of all since I decided to get out of it today .Its likely that it will not fall further but its also likely that it will drag the depths for a while and since I would need it to more than double to make any profits in it,I thought its better to look elsewhere . Green looks and feels good even if it grows on bloody soil .

6 Likes

Its the growth which has tappered off for current year. If they are not able to cross revenue of 2000 Cr (possible scenario) then it will be flat growth or maybe even de-growth. I am tempted to enter at current price but since the QIP was done at 700 rs (discount actual price 30-50%)and bonus share was issued later. I will wait for further correction which may or may not come.

Disc: tracking with no position

3 Likes

I exited from this stock as soon as world bank news came out. But that was not the only problem with TARIL. Governance lapses, disproportionate remuneration hikes, and alarming financial irregularities.

Key findings include:

• 161% MD salary surge without justification

• Entire board controlled by one family

• Employee costs up 116% despite flat revenues

• Order book potentially down 47%

• Negative operating cash flow of ₹34.71 crore

Detailed report covering these aspects attached.

1762943365185.pdf (441.7 KB)

What a worthless report ! Whoever wrote it deserves 161% salary reduction.

.

- EPS went from 1.6 to 7.5 rupee..and he writes no justification for salary hike!

- there are independent directors in the board from outside family .So no one can have a family run business ?

- Revenue went from 1291 to 2017 crores and he asks why employee costs increased. Who will make the transformers ? Are transformers von neumann machines ?

- With one quarters orderbook,he assumes next quarters will be same and hence 47% down.wah!

- same for operating cash flow! One quarter is enough to say anything !

Best of luck to anyone taking investing decisions based on this kind of analysis .He will need it.

20 Likes

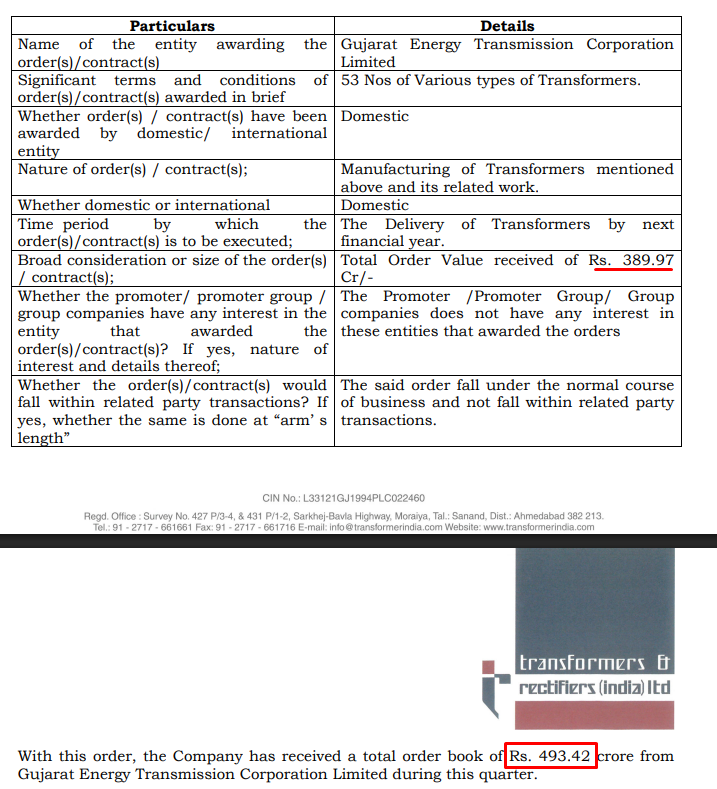

Transformers and Rectifiers (India) Limited has secured Order of Rs. 53.33 Cr from Power Grid Corporation of India Limited. It is an HVDC Converter Transformer order, and TARIL is the first Indian Origin Private Sector Company to receive such an order.

dffeca72-86b6-4d96-8b2c-53f60fe6948f.pdf (242.0 KB)

3 Likes

TARIL has fallen 50% in the last two months.

Sharing my understanding so far. Would love to hear views from anyone who has studied the company in depth.

What went wrong recently:

#1. A weak quarter because of temporary operational issues

a) Raw material delays due to customs confusion

- TARIL uses a specific copper conductor called CTC.

- A new BIS rule required certain types of copper imports to have certification.

- Customs officers mistakenly thought TARIL’s imported CTC also required this.

- The material got stuck.

- Transformers that needed that material could not be completed or dispatched.

- By the time the misunderstanding was cleared, the quarter was almost over.

Impact

- Revenue was lost (actually only delayed)

- Margins fell because fixed costs stayed the same.

b) Heavy rains delaying customer sites

- In this industry, you can bill only when the customer’s site is ready.

- That means even if you have produced the transformer, you cannot recognise revenue until installation conditions are met.

- This quarter, many customer sites were flooded or had damaged access roads.

- Finished transformers were lying ready but could not be billed.

- Management said almost one hundred crore of finished or near finished transformers were stuck.

Impact

- Manufacturing happened

- Billing did not

- So revenue looked low but inventory looked high.

c) Old low margin orders impacted margins

- Some very old orders taken at weaker pricing were delivered this quarter.

- Normally this is fine.

- But this quarter had low revenue, so fixed costs like salaries, plant expenses and power got spread across fewer transformers.

- Result: even weaker margins this quarter.

d) ESOP scheme added a new expense

- TARIL issued a large ESOP program to employees (around 26.3 lakh options).

- As per accounting rules, companies must record ESOP expenses every quarter as if they are employee costs.

- Because ESOPs dilute shareholders in the future, they appear as an expense in the P&L.

- This has nothing to do with cash outflow, but it reduces reported profit.

- This quarter’s ESOP expense alone was roughly 3.6 crore.

- Similar expenses will come every quarter until the options vest.

- The company has not disclosed the exact vesting schedule.

- However, standard SEBI and industry practice is that most ESOPs vest over three to four years.

- So ESOP expense will keep hitting P&L until FY29 or FY30.

- With that assumption, annual ESOP cost would be around fifteen crore per year.

- Over four years, total impact would be around sixty crore.

- Based on my quick calculations, ESOPs were being valued at about two hundred twenty to two hundred forty rupees per option.

So the quarter looked bad because of

- lower temporary billing

- lower temporary margins

- higher expenses (temporary, except ESOPs)

- and a temporary working capital spike.

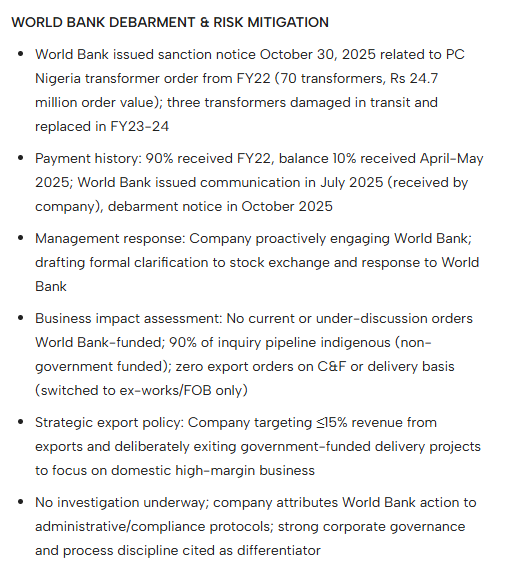

#2. Then the World Bank matter added fuel to the fire.

A news report came out that TARIL was debarred from participating in World Bank projects due to charges of corruption. My understanding so far:

What happened

-

A few years ago, in 2020, TARIL took up a World Bank funded project in Nigeria.

-

Their role was to supply seventy transformers to a local utility.

-

This was only one part of a much larger project with many other contractors and local entities.

-

The total project size was around USD four hundred eighty six million.

-

TARIL’s portion of the contract was worth USD twenty four point seven million, and all seventy transformers were supplied.

-

Around ninety percent of the payment was received in FY22.

-

The balance ten percent was received in Q1 FY25.

-

In 2023, the World Bank reached out to TARIL with a set of queries regarding this project.

-

TARIL cooperated and submitted all clarifications.

-

After that, the World Bank did not revert with further questions or concerns.

-

Now, many years later, the World Bank’s Integrity Unit has put TARIL on a “debarred” list for this project along with some others.

-

The stated reason is broadly “corrupt practices” in the project ecosystem.

-

TARIL was one vendor inside that larger project.

-

This is not “TARIL stole money” but rather “the overall project had irregularities in how contracts were awarded and handled.”

-

TARIL is barred from participating in future World Bank financed tenders for a certain period.

-

They do not have to return money from that old project.

-

This Nigerian project is the only World Bank funded project TARIL has ever executed.

-

Management says there are no World Bank funded orders in the current order book or inquiry pipeline.

-

More than eighty to eighty five percent of the company’s current inquiries and order book come from Indian central and state utilities.

So in terms of pure business:

- There is no revenue loss from current orders, because there were no World Bank funded orders anyway.

- There is no impact on the current pipeline.

- The Nigerian project is done, delivered and fully paid.

Impact

- Being on a World Bank debarment list is not a small matter.

- Some institutional investors have internal rules against owning such stocks.

- Lenders, rating agencies and even some customers may ask questions.

- Markets punish any hint of governance issues heavily, especially after a sharp rally.

- We only know TARIL’s side from the concall and press interactions. The full World Bank document is not yet public.

- TARIL says they will challenge this and have already started the process. It may take around eighteen months to get the debarment removed, if at all.

After the weak Q2 results and the debarment news, the stock has fallen by around fifty percent.

Is this an opportunity?

- Management has maintained guidance of 25% year on year top line growth.

- The current stock PE is around 29. It was above 75 in the bull market of 2024 and around 25 in the bear market of 2022 when the company was not growing.

- Due to the reasons mentioned earlier, EBITDA margins fell to 11% last quarter, but management has guided for 16 to 18% margins.

- Due to ESOPs, PAT and EPS may be impacted by around 5%, which would still mean roughly 20% PAT growth.

- A business growing PAT at 20%, available at a PE of around 30, fits the Peter Lynch idea of a PEG ratio near 1.5 for a reasonably valued compounder.

- When EBITDA normalizes, ESOP impact is absorbed over time, and if growth continues, the PE can re-rate to 50+ in the next bull market.

- This seems like a lower risk, higher upside bet.

Look forward to hearing what you all think.

References:

Media appearances:

- https://youtu.be/9XGsxY4m90U?si=HCvgnyJBL9m8h4r6

- https://youtu.be/sorJ7z0fgTE?si=HOQwdEG4F8-IRPn-

- https://youtu.be/mfN63W2sLRA?si=l-T5Zi8t0r6BFdDf

Most recent ConCall:

Disclosure: Invested, thinking of topping up.

21 Likes

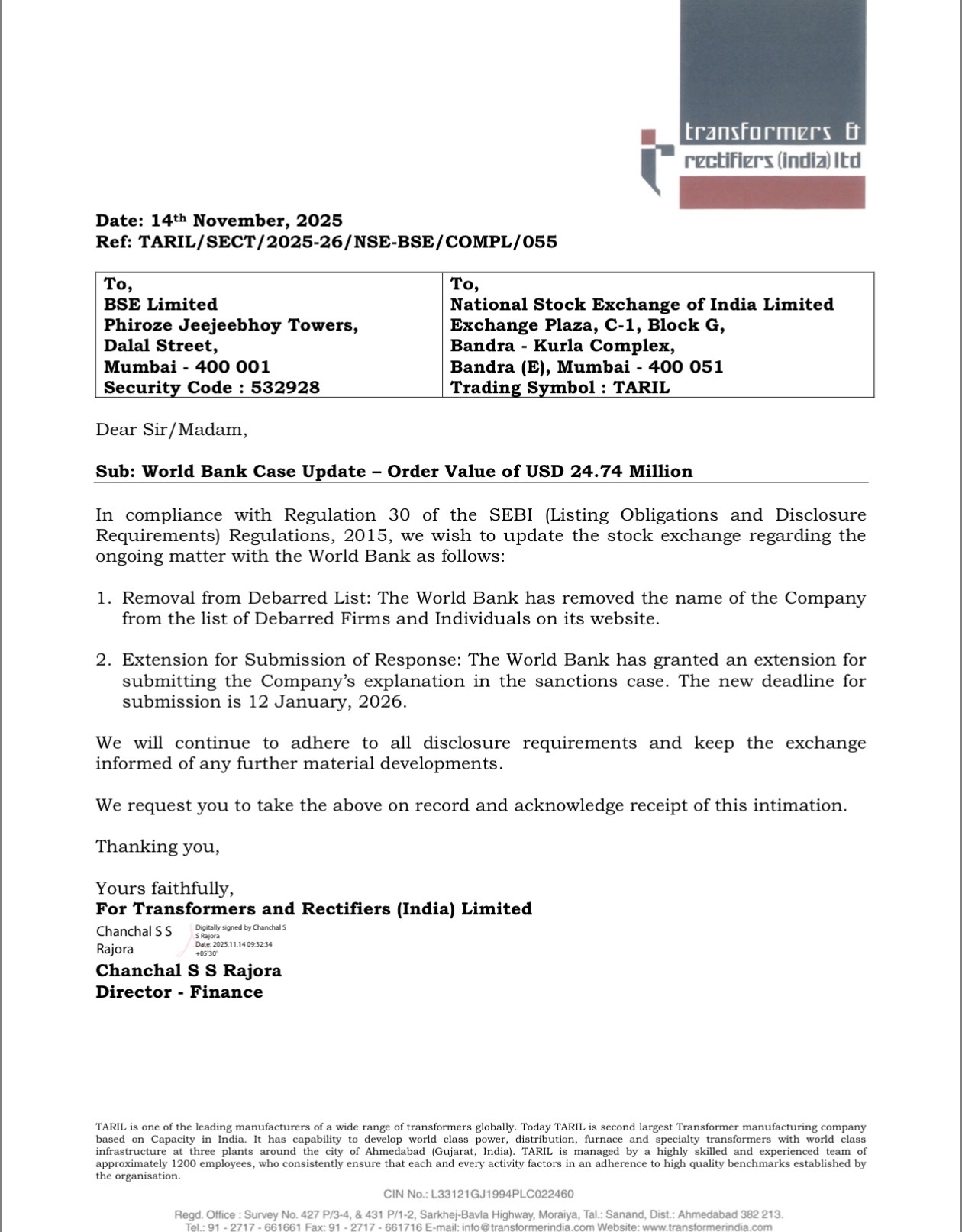

Just to add on World Bank

- Removal from Debarred List: The World Bank officially removed TRIL from its list of debarred firms and individuals on November 14, 2025. This interim relief potentially allows the company to participate in World Bank-funded projects again.

- Extension Granted: TRIL has been given an extended deadline of January 12, 2026, to submit its explanation regarding the allegations of corrupt practices in a past Nigerian power project.

4 Likes