Tourism Finance Corporation of India Ltd:

CMP:60.80

Recent measures such as electronic travel authorisation, Visa on Arrival and growth of new Tier II cities, are set to encourage tourism in India. Rating agencies expect 8-13% y-o-y growth in tourist arrivals over the next three-to-five years. Industry-wide occupancy rates have improved over FY13 levels. 60%+ of incremental room supply over FY14-19e is targeted at the fast emerging mid-market/budget class. This synchronises well with TFCI’s growth strategy in its next phase of transformation.

Need view from other valuable valuepickr members about this stock:

The latest quarter results (Q4FY16) show an increase in the net NPAs. The management says that 50% of the NPAs will be reversed in this quarter. However, the asset quality concerns seem to be a worry and the stock price has reacted accordingly. One good thing is that the management is being cautious and not lending just to grow the business.

I think this could be a good time to take a tracking position and increase the holding based on the future performance. Fundamentally, the company’s business is good. Tourism is growing in India. The results published by some hotel cos point to a revival in the tourism sector. The room occupancy levels are going up.

If the asset quality improves, the stock could go back to the 2015 highs of 80+ levels.

Disclosure: I have a minor tracking position in this company. My views are hence biased.

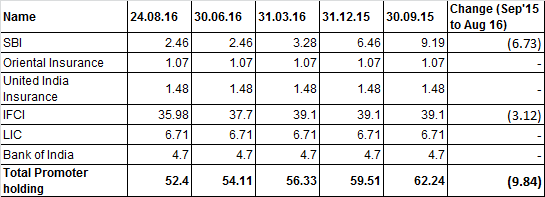

Its a PSU, 52% owned by government institutions as below:

Note that the main promoter IFCI and SBI have been reducing their stakes through open market sales. Why they are selling? Is somebody accumulating? I don’t know.

Remaining shareholding is spread among public, with 5.37% with mutual funds / banks, 8.5% among corporate bodies and remaining among individuals.

Macros:

At macro level tourism sector may see good growth ahead. The government is willing to spend on improving the sector. An eg.

Measures such as GST and Visa on arrival are likely to benefit the sector. I will not dwell too much upon macros, but generally things could start looking up with the various government initiatives taking shape.

Within tourism, why TFCI?

What got me interested in the company (being a lender myself) is that a significant majority of the loans outstanding is secured by mortgage over the property financed. Management claims that the loan cover is 2-3 times (I would take this with a grain of salt). Significant majority of loans is to hotels. Here the appraisal process becomes very important as the valuation at which LTV (loan to value) would have been determined should not have been inflated in the first place. Being a PSU, with IFCI as the main promoter doesn’t give much comfort on this front.

Details of the type of projects financed, types of funding etc. are laid out. Essentially, they fund hotels, which constitutes 73% of the total cumulative sanctions till Mar’16. This is mainly in the form of long term loans and equity/preference share investments. They also fund development of amusement parks, shopping complexes, entertainment centres, restaurants, tourist cars and coaches etc. This constitutes another 9% of the sanctions. The balance is in infrastructure projects, which includes real estate development, energy, communication, water and sanitation etc. (couldn’t find a detailed break up of this portion).

As on 31.03.16, total loans outstanding are 1300cr. Top 20 borrowers account for 60% of the loans (which works out to total of 791 cr, and average per borrower of 40 cr., not a small amount per borrower). Concentration risk is definitely there. Top 4 NPAs amount to 122 cr (average 30cr per borrower).

Capital adequacy is very high at 38%. Its been around the 38-40% mark since 2012.

Total employee cost in 2016 was 6.7 cr. Total there are 33 employees of which 4 are considered key management. These 4 have an average salary of 2.7 lakh per month (includes perks and bonus etc). Excluding these, the average pay per employee is 1.2-1.5 lakh per month. Which is decent considering it s a PSU. Top 10 employees have average employee cost of 2.4 lakh p.m. Employee aspect is important as this will reflect on the appraisal quality. The general salary levels indicates that quality of employees may not be bad inspite of being PSU.

Negative part is that financials have chequered history. There is no trend whatsoever in growth metrics of income, profit, loan sanctions, disbursements etc., which go up, go down.

NPA issues:

Fy16 net NPA is 10% of total advances (PY 1.5%; nil in earlier years). However All the new NPA additions are secured by property. Management claims that it will be reversed this year. The company has never had to write off any loans.

There are lot of interesting insights regarding the stress in the hospitality sector in this article-

Assumptions based on which loans were granted turned out to be very aggressive given the soft economic conditions. While there are reasons to believe that things may turnaround, however timelines are uncertain and the wait may test patience.

One negative that the earlier MD had said as late as Jan 16 that there will be no slippages and within 2 months they reported very high NPA numbers. Was he asked to leave due to this? Just my conjecture.

Possible Triggers:

The new MD joined in Feb 2016 who is well qualified (MBA from Rotman School of Management at University of Toronto). He has held various positions in IFCI and IDBI Bank as well as directorships in Nagarjuna Fertilizers, Stock Holding Corporation of India, Shakti Pumps, DCM Shriram Industries. I have heard that he is dynamic, but its just heresay. Bloomberg - Are you a robot?

Company has a disbursal target of 600 cr this year (compared to 380 cr in 2016 and 584 cr in 2015). Albeit they have disbursed only 127cr in 5 months till mid Aug. Looks like a tall task.

Reversal of NPA’s in FY 17. While NPA’s increased, there was no increase in provisions during FY16, which I found surprising (maybe they already held excess provisions, which were adjusted towards this). TFCI website has put out advertisements for selling mortgaged properties (presumably belonging to NPAs) and they are in the May-Aug period. Does this indicate aggressiveness in recovering dues? Looks so.

Some thoughts on valuation:

Total equity investments are 37 cr. Asset reconstruction company (ARC) security receipts are 31cr. Assume nil value - i.e. writeoff 68cr.

Other investments are in IFCI bonds and bank CDs. Hopefully no need to write these off. Also, not writing off any NPAs considering the secured nature.

Net worth is 514 cr. No of shares outstanding is 8 cr. Adjusting the above investments of 68 cr from networth, the book value works out to 55 per share.

Debt is 1000cr. D/e ratio is just 2. Which is low for a financial institution.

FY 16 eps was 6.6. Q1 2017 EPS was 2.5 (22% growth YOY). Cmp is 48 (12.09.16).

Disclosure – I don’t have any investment at the time of this post. Am evaluating the company, and may invest in future. To do that I will have to sell one of my exiting holdings, as I am fully invested. This is not a recommendation.

I thought that the recent run-up was because of anticipation of good results in this Q. However it looks like results will be subdued. NPAs, which were earlier stated to be temporary and reversible (watch earlier interviews posted above) will remain NPAs (as per latest interview) and provisions on these will eat into any improvement in revenues/profits. They had not taken provisions in June Q. They maintain their disbursement targets; but I continue to be skeptical of that.

31 March 2017 shareholding pattern shows continued divestment by IFCI during the quarter, however, I am unable to identify interested parties causing upsurge in share price over past month. No bulk deal or block deal data on BSE either.

Is Insync Capital still a buyer ? I do not find their name on the quarterly shareholder data. Any inputs?

Disclosure: Not currently holding, just interested.

TOURISM FINANCE CORPN trading in new Lifetime high. As Co declared good profit in last few quarters I am hoping this stock will do well. CMP Rs.123.30

Disclosure: Invested @ lower price.

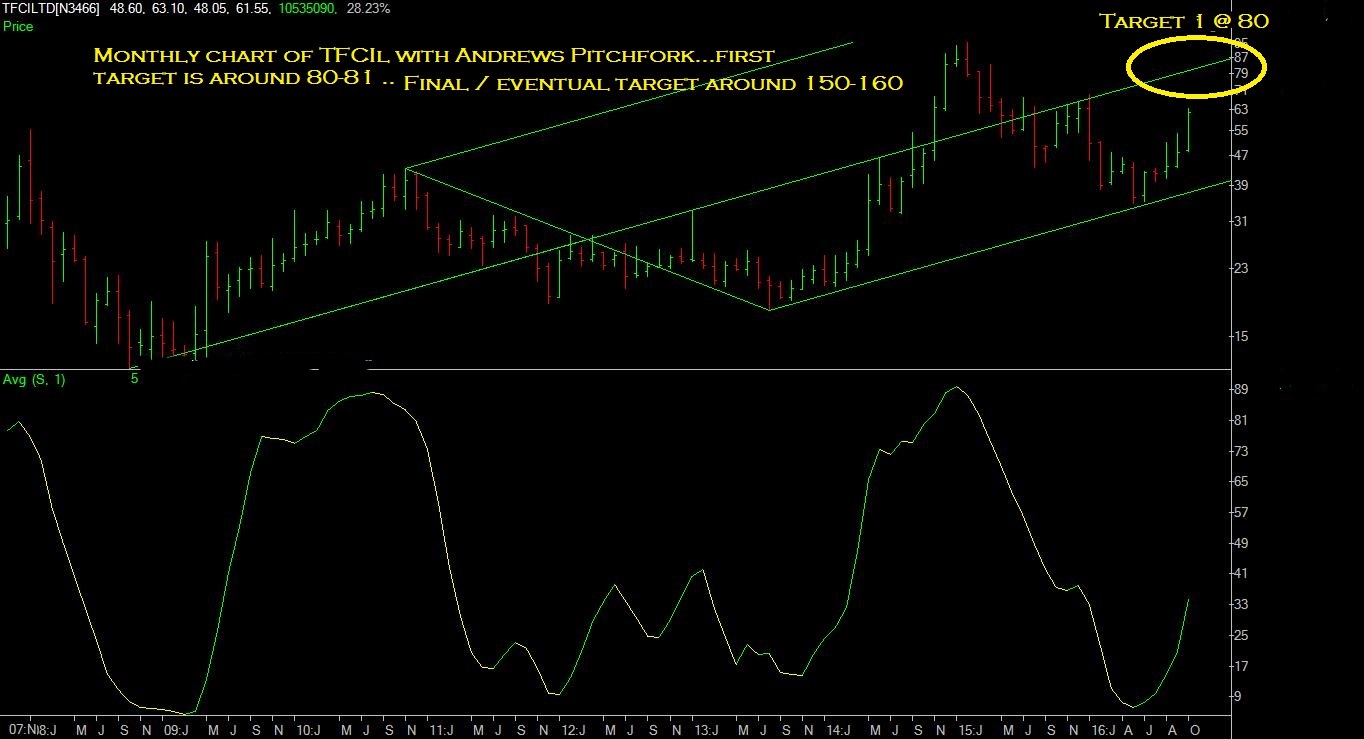

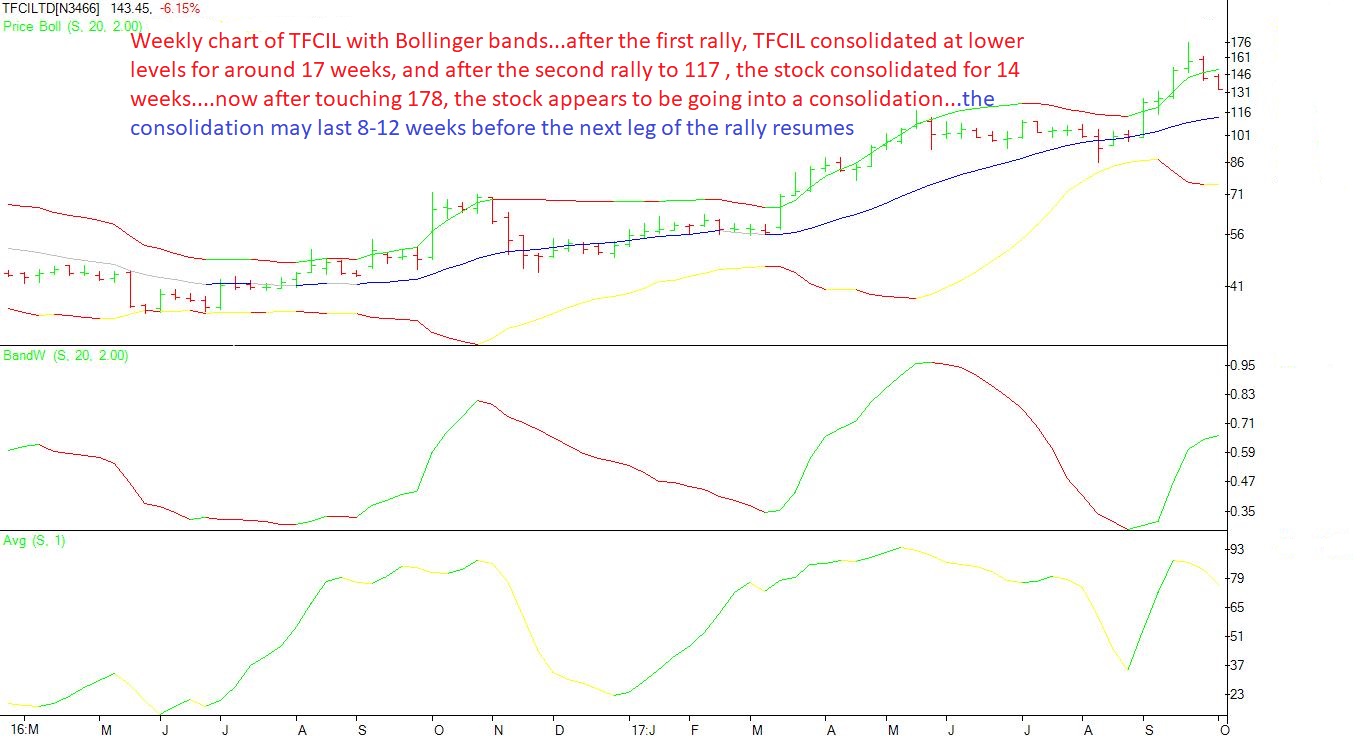

TFCIL hits multiple resistance levels @ 156.50…and the stock has corrected from that level. It is quite possible that after almost a 90% rise in price in a short period of time, TFCIL may undergo a time / price correction for a shorth period of time. I have totally exited at my TFCIL holding @ 156.50 (the resistance line)…on breakout above this resistance zone, TFCIL can then rapidly go up towards 200-250 levels…