Some rough concall notes I could make.

Domestic growth looks poor bcos some products had to be pulled back from the market due to implementation of NLEM guidelines.

Co had started to focus on rationalisation (discontinuation of bonus, discounts etc) of domestic biz in q2 last year and the impact of those steps would be comparable post q2 this year. Co expects to grow better than market growth in domestic front. Forecast for market growth is 8-10% for full year.

Co’s inventory is 14 days as compared to 19 days for market.

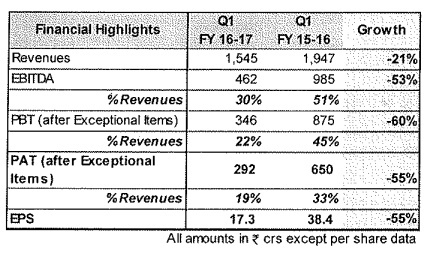

Reconciliation figures according to Indian GAP was for previous quarter.

R&d would reach 7-8% by end of year. Currently at around 6% of sales in q1 fy 17. Mainly, no of ANDA projects going up which includes some dermatology products.

Brazil approvals - 3. Approval timelines are 2 years but communication has improved with ANVISA. Price hike is taken for most of products in Brazil. Most of competitors also doing that. CNS, cardio and diabetes are focus areas in Brazil.

Glochem – Torrent has 2 API plants. Glochem adds overall API capacities by 35%. It was already approved by Torrent as a supply contractor. Objective to file 10-15 DMFs every year and Glochem will help in that.

Besides USA, Germany, Brazil and UK remain growth focus areas.

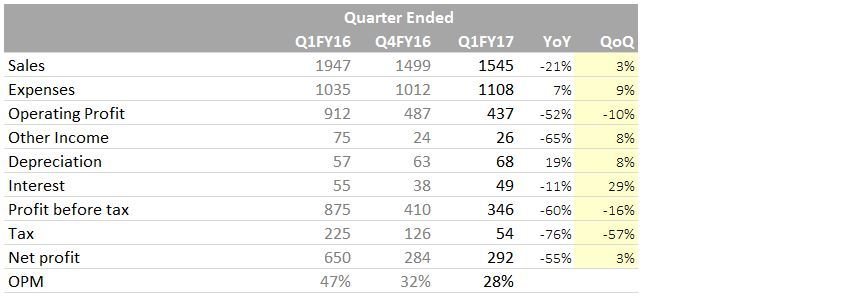

Higher Personnel cost increase is due to Dahej, increased R&D and one time leave encashments to employees . (more than 10 crores)

In US, co has a few jokers in the pack. Plus Dahej facility helps in increasing volumes. Plus there are 10 launchdes. Taken together these three will reduce the abiify price erosion impact. Abilify is far from bottom. (indicates there is some more juice left) Co doesnt discuss revenues by products, but abilify prices have gone down. But positive effects from nexium and tolteridone (detrol) . detrol is a 4 player market and prices are stable. Nexium also price has declined but not by much (2 players in Nexium play were affected by USFDA actions). No of products approvals from US expected to be 10 and expect commercialisation of all of them this year. Ex-abilify US base biz has grown y-on-y by low double digitsand q-on-q also there is some growth.

In US first new launches for the year likely to be end of August. Crestor approval likely to be in October. Crestor is not as attractive as earlier expected as market fairly competitive in that product.

Margins likely to improve going ahead in India and Brazil

.

Depreciation and amoritisation – phase I not fully capitalised so dep will increase going ahead but output also will increase. Dahej capacity utilisation by end of year should be 70-80%. Next year there will be de bottlenecking. Currently capacity utilisation during the qtr would be 50% but product approvals are coming one by one from US. 6 products approved from Dahej. Expect 10 products approvals from Dahej by year end. Some German approvals also expected.

Tax rate— This qtr exceptionally low but overall will be in range of MAT rate for full year.

Dahej capacity currently 3. 5 billion tab. To be ramped up to 6 billion tab by year end. Co plans to increase to 7.5 by de bottlenecking during phase I itself. Current volumes in US is 300 crore tablets a year. Dahej would be approved for US, Brazil and Europe. Co plans to gradually shift US products to Dahej and free up Indrad for Europe and brazil. Germany tender market likely to be targetted more due to Dahej facility.

ACQUISITION – Acquiring products, acquisition of assets etc are on the cards.