I am late but here are my highlights from Annual report of FY16.

ANDAs filed=77, 62 approved including 6 tentative

US DMFs=27

Europe dossiers=59

Europe DMFs=28

-

Advanced clinical trials for 2 programs- cardio metabolic risk reduction and heart failure. far.

The most advanced discovery program of the Company is Advanced Glycation End-Products (AGE) Breaker, of which the Phase II clinical trials for the indication of diabetes associated heart failure in India and Europe is completed. During the year, clinical development plans have been finalized and we expect to file for the continuing clinical development later in the current year.

During the financial year 2012-13, the Company initiated Phase-II clinical trial in India with its second NCE for the reduction of cardio metabolic risk. The results have been encouraging and preparations have been initiated to start the next phase of development. The Company believes that this program is uniquely positioned to address the consequences of relative chronic over-nutrition which is assuming alarming proportions of health hazard in India, other emerging economies besides developed countries. Phase Ib study for its third NCE being developed for inflammatory bowel disease has also been initiated and is expected to be completed by Q1 of financial year 2016-17. Further characterization is progressing well for this indication. -

Working on NDDS projects such as long acting injectable, nasal sprays, oral dispersible films and foams in order to improve efficacy and therapeutic outcome.

-

Initiated investment in the areas of Oncology, Dermatology, Opthalmic, Biosimilars and Respiratory. Planning to invest 6-8% of sales in R&D activities in order to develop diversified dosage forms with high level of complexity.

-

The company has initiated work on a green field integrated manufacturing facility for drug substances and drug products (API & formulations) in Oncology. The Phase I has installed capacity of 20 mn tablets, 7 mn capsules and 3 mn lyophilized vials. The facility shall conform to latest international regulatory requirements of USFDA, EU-Germany.

-

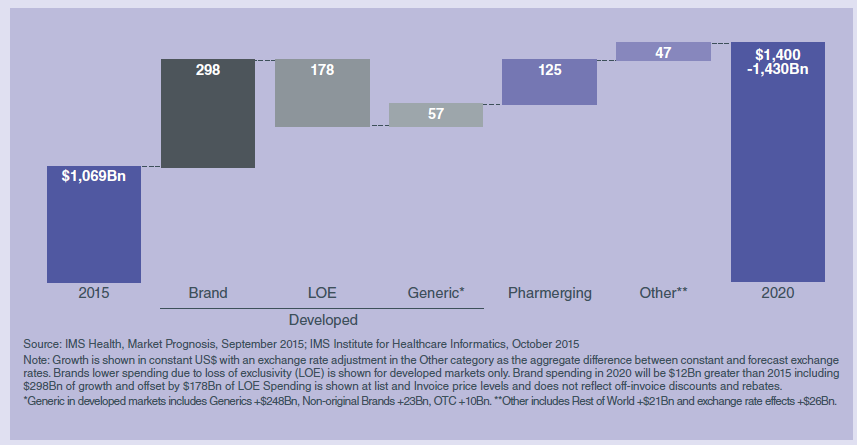

US market is experiencing a shift in balance of “innovation cycle”- fewer patent expiries and launches of more innovative medicines

-

Higher growth in pharmerging markets (10-13% till 2020) compared to US 5-8%

-

The key drivers of the growth for pharma market over the next five years will be: Access expansion in Pharmerging countries, greater use of more expensive branded medicines in developed markets, and greater use of cheaper alternatives when loss of patent exclusivity occurs.

-

Specialty therapies continue to be more significant in developed markets than in Pharmerging. Oncology continues to be the largest category in developed countries. Leading classes in Pharmerging markets are dominated by pain, antibiotics and hypertension, while in developed markets specialty categories such as oncology and auto immune diseases are more prominent

-

The Indian pharmaceuticals market is valued at Rs 98,414 crores in March 16 MAT (Moving Annual Total) by AIOCD with growth of 13% over the same period in 2015.

-

India business- The Company is ranked 17th in the IPM with significant presence in Cardiac, CNS, GI and Antidiabetic therapies. Our 11 brands are in Top 500 brands of Indian Pharmaceuticals market. Brands like Shelcal, Chymoral, Nikoran, Dilzem, Nebicard, Nexpro etc have been contributing significantly to the India sales

-

Brazil- Economic pressure is also expected to keep a check on the government spending on healthcare impacting its public access for free medicines (select drugs), program “Farmacia Popular”. Federal and State government buying through tenders are also expected to take a hit, thus retail demand for more and cheaper drugs would continue at the forecasted levels, in the private market

-

During the year, S&P downgraded Brazil’s long term sovereign credit rating to BB (2 notches below the investment grade), citing concern about weakening of the country’s credit profile and expectation of a longer adjustment process, slower correction of fiscal policy and another year of recession. In the recent months, the Brazilian Real has appreciated and moved from a low level of 4.16 to a US$ to 3.59 levels presently. However, the macro economic backdrop warrants depreciation pressure in the currency not only on account of weaker economic outlook but also on account of volatile external environment.

-

Brazil- Among the Indian Companies, in terms of market share, Torrent ranks No. 1 with the second largest less than half of the size of Torrent (IMS dataset). The Company has 19 products under approval out of which 3 products are expected to be approved during the coming year. The Company has a development basket of 49 products with 16 products in the Cardio Vascular (CV) segment, 21 products in the Central Nervous System (CNS) segment, 10 products in the Oral Anti Diabetic / obesity (OAD) segment and 2 products in other segments.

-

In Brazil where the Company sells branded generics, the pure generic competition could adversely affect development of branded business. The Company has been building its product portfolio in the generic segment with parallel filings of the Company’s products in the CV, CNS, OAD & Other therapies. The Company has approvals of 18 products whereas 15 products are under approval.

-

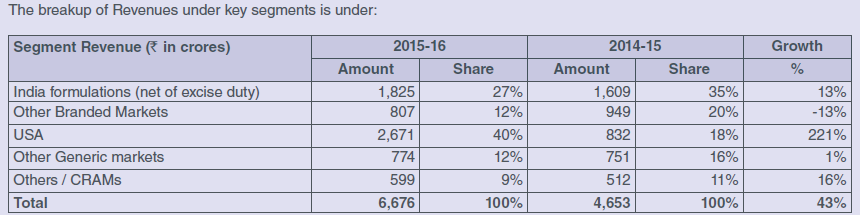

USA- The Company received 7 ANDA approvals in financial year 2015-16. The Company has 62 ANDA approvals (including 6 tentative approvals) and its pipeline consists of 14 pending approvals and 119 products under development. The US business is expected to contribute to the growth of international business in a significant way.

-

In the US, there is a continuing trend towards consolidation of certain customers groups such as wholesale drug distribution and retail pharmacies, as well as emergence of large buying groups. The consolidation may result into these groups gaining additional purchasing leverage and consequently increasing the product pricing pressures. Additionally the emergence of large buying groups representing independent retail pharmacies and prevalence and influence of managed care organizations and similar institutions potentially enable those groups to attempt to extract price discounts on our products. The result of such developments could affect the sales volumes and price realizations of our products on an overall basis.

-

Europe- The Company’s European business mainly includes Germany, United Kingdom and Romania where the Company has its direct presence. Germany is the fourth-largest pharmaceutical market in the world and the largest in Western Europe. It is valued around Euro 28 Bn and is expected to grow at a CAGR of 3-4% till 2020. Majority of the market is tender driven and it is expected to continue for foreseeable future which is putting pressure on the margins of the industry. Among the Generic players, Torrent holds 6th position with a market share of around 4% and is ranked No. 1 among Indian players in the Market.

-

Price erosions continue in the German generic market leading to shrinking operating margins. The insurance companies have been empowered to enter into rebate contracts and float tenders. Aggressive bidding by competitors could lead to unsuccessful bids in tenders exposing the Company to loss of existing sales. Likewise in other European markets, regulatory changes could

affect price realizations. -

The Company has commenced commercial production of its formulation manufacturing facility at Dahej SEZ in Gujarat during April 2016.The Company has received regulatory approvals from various regulatory authorities viz. USFDA, EU-Germany etc. Phase I of the Dahej facility has an installed capacity of about 600 crore tablets / capsules. Construction of Phase II will commence soon and once commissioned, the total capacity will increase to about 1100 crore tablets / capsules and 80 MT API per year.