Q1 FY25 Highlights (Consolidated, YoY)

- Revenue down 0.9% to Rs 903 crore versus Rs 911 crore

- Ebitda down 4% to Rs 102 crore versus Rs 106 crore

- Ebitda margin narrows to 11.3% versus 11.6%

- Net profit up 8.4% to Rs 67 crore versus Rs 62 crore

Revenue growth was primarily led by the company’s larger segment i.e. freight rail systems, which recorded 12.9% growth to Rs 842.19 crore. However, the passenger rail systems segment declined 63.04% to Rs 60.86 crore.

2 Likes

Titagarh Rail Systems Q1 FY25 Analysis: Key takeaways!!

Titagarh Rail Systems Limited remains optimistic about its growth prospects, backed by India’s robust infrastructure push. The company expects to achieve double-digit wagon production numbers in FY25, up from 8,400 wagons in FY24. In the Passenger Rail Systems (PRS) segment, TRSL aims to ramp up production to 10-15 cars per month by Q3/Q4 FY25, with a target of reaching 70 cars per month in 3-4 years.

Strategic Initiatives:

-

Technological Upgradation: TRSL is transitioning from a pure manufacturing company to a technology-driven product company. The company has established design centers in Kolkata and Bangalore, focusing on R&D and engineering capabilities.

-

Propulsion Systems: TRSL has begun exporting traction converters to Europe, marking a significant technological milestone.

-

Joint Ventures and Partnerships: The company is leveraging strategic partnerships with ABB for metro TCMS and propulsion systems, and a joint venture with Ramkrishna Forgings for wheel manufacturing.

Trends and Themes:

-

Shift towards higher-value products: TRSL is moving up the value chain by developing propulsion systems and other high-tech components.

-

Localization of critical components: In line with the government’s ‘Atmanirbhar Bharat’ initiative, TRSL is focusing on indigenous production of critical rail components like wheels.

-

Export orientation: The company is exploring opportunities to export rail components and technology to international markets.

Industry Tailwinds:

- Government focus on rail infrastructure: Increased budgetary allocation for railways and urban mobility projects.

- Expansion of metro rail networks across Indian cities.

- Push for Vande Bharat trains and other modern rolling stock.

Industry Headwinds:

- Supply chain disruptions and raw material price volatility.

- Skilled labor shortages in the manufacturing sector.

- Potential delays in project execution due to various factors including elections and weather conditions.

Analyst Concerns and Management Response:

-

Concern: Muted Q1 performance in the Freight segment.

Response: Management attributed this to seasonal factors and expects a strong rebound in subsequent quarters. -

Concern: Decline in PRS segment revenue.

Response: This was due to the completion of the Pune Metro project. The company expects growth to resume with the Bangalore Metro project ramping up. -

Concern: Execution challenges for new orders.

Response: Management assured that they are addressing supply chain issues and building necessary capabilities to meet delivery timelines.

Competitive Landscape:

TRSL faces competition from both domestic and international players in the rail manufacturing space. However, its focus on technological upgradation and strategic partnerships is expected to enhance its competitive position. In the wheel manufacturing segment, TRSL’s joint venture with Ramkrishna Forgings positions it as a key player in a market currently dominated by public sector units.

Guidance and Outlook:

Specific numerical guidance was not provided, but management expressed confidence in achieving strong growth in FY25. The company aims to maintain EBITDA margins of 12-12.5% in the Freight segment and targets 14-15% margins in the PRS segment with propulsion integration.

Capital Allocation Strategy:

TRSL plans to invest INR 700-1000 crores in capex over the next 18 months, primarily for expanding PRS capacities and setting up new production lines for Vande Bharat trains.

Opportunities & Risks:

Opportunities:

- Potential orders for aluminum Vande Bharat trains.

- Expansion into international markets with high-tech rail components.

- Diversification into new product lines like propulsion systems and wheels.

Risks:

- Execution delays in large projects.

- Fluctuations in raw material prices affecting margins.

- Dependency on government orders and policy changes.

Regulatory Environment:

The Indian government’s push for rail infrastructure modernization and indigenization of components provides a favorable regulatory environment for TRSL. However, the company needs to navigate complex tender processes and quality standards set by Indian Railways and metro authorities.

Customer Sentiment:

With Indian Railways and various metro corporations as primary customers, the sentiment remains positive due to ongoing and planned expansion of rail networks. Private sector demand for freight wagons also shows an upward trend.

Top 3 Takeaways:

- TRSL is undergoing a significant transformation from a pure manufacturer to a technology-driven product company in the rail systems space.

- The company’s focus on high-value components like propulsion systems and wheels positions it well for future growth.

- While short-term challenges exist, TRSL’s order book and capacity expansion plans indicate strong long-term growth potential in line with India’s infrastructure development goals.

5 Likes

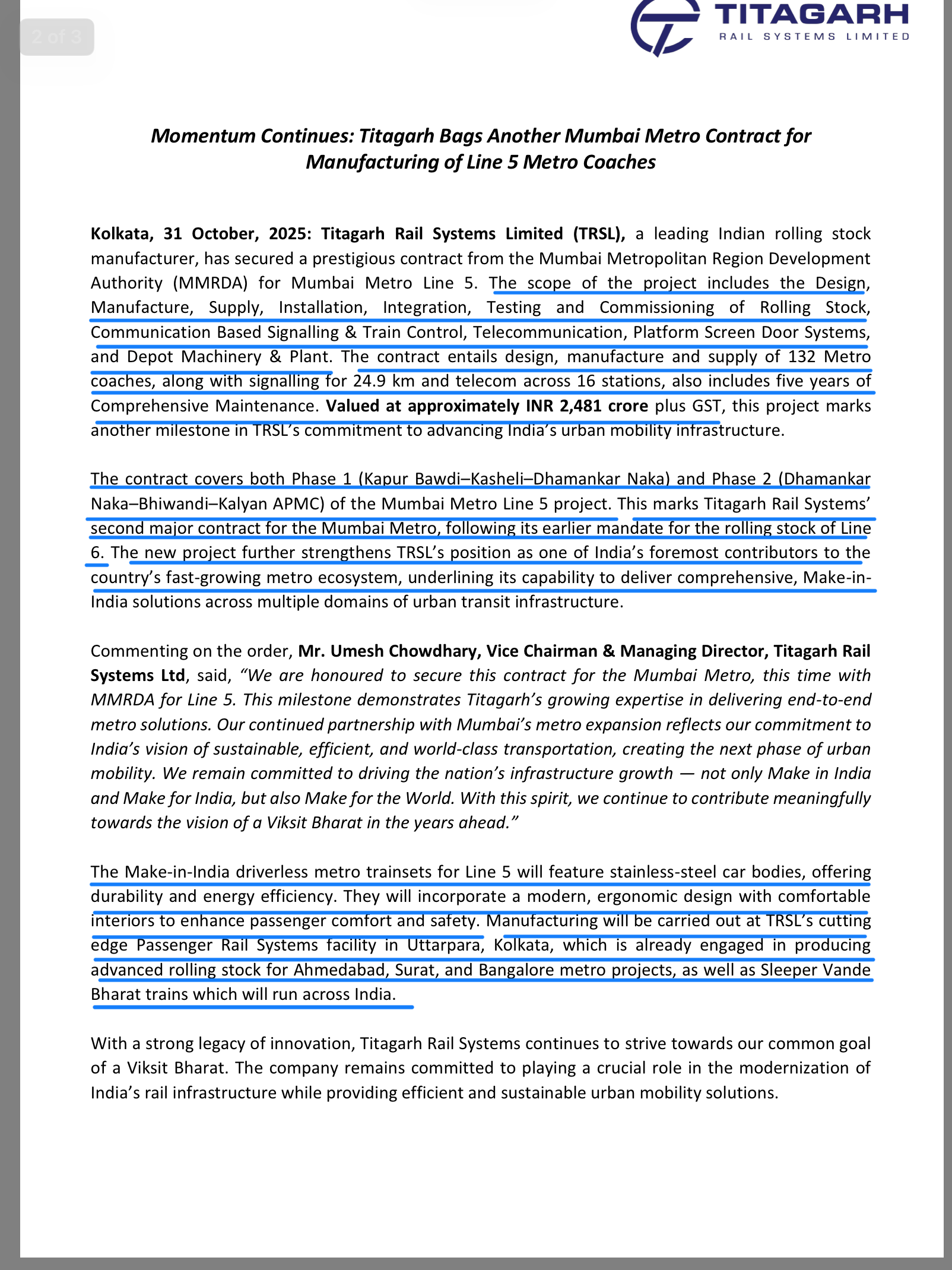

Titagarh Rail Systems Ltd handed over its first driverless Made in India trainset to the Bengaluru Metro Rail Corporation (BMRCL).

4 Likes

Great news for Titagarh

1 Like

Titagarh Rail Systems | New Business Verticals

The company has introduced two new business segments:

a. Shipbuilding and Maritime Systems: This will focus on shipbuilding, ship repair, and other maritime-related businesses.

b. Signaling and Safety Systems: This vertical will handle railway signaling, train control, condition monitoring, and safety solutions for railway operations.

6 Likes

Did they provide any explanation on foraying to new verticals? Is their core segment not seeing good growth?

1 Like

https://nsearchives.nseindia.com/corporate/TWL_13022025205947_Integratedfilingfinancials13022025.pdf

result out for Q3 FY2025, Poor QoQ and YoY. I would wait for management commentary tomorrow however expecting a major cut tomorrow.

1 Like

Titagarh Rails | Numbers

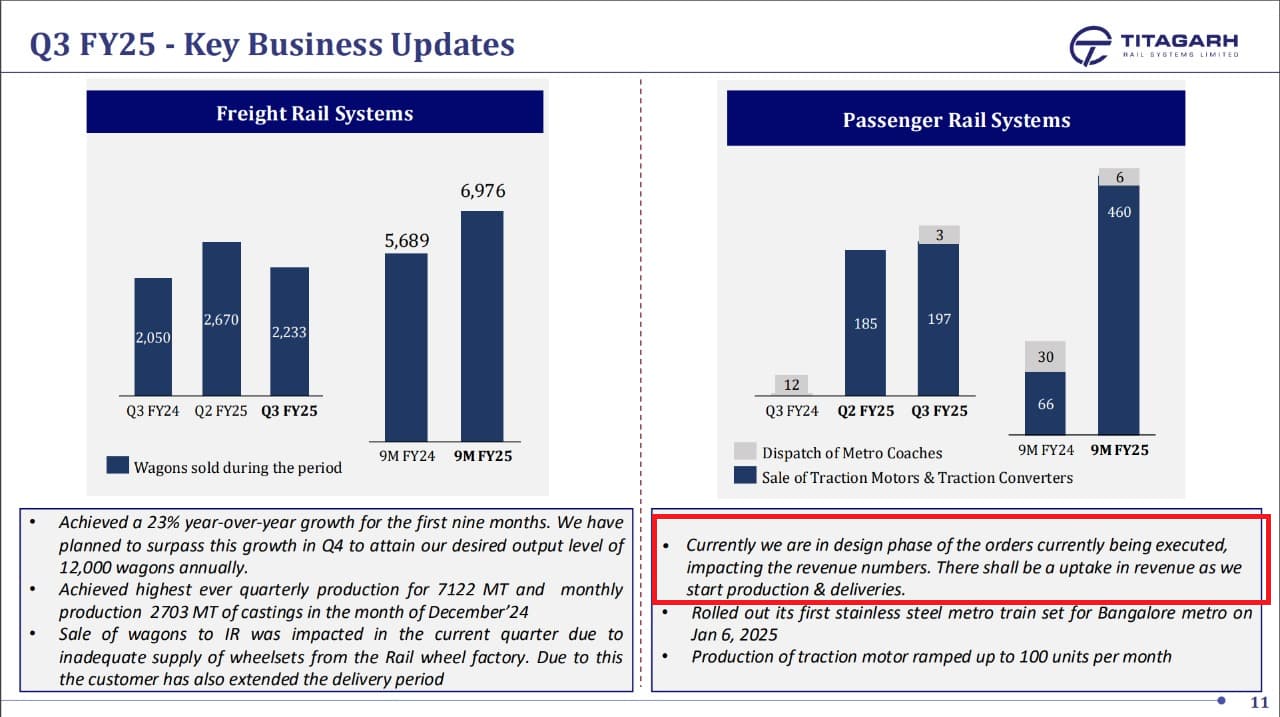

a. Currently company is in design phase of the orders currently being executed, impacting the revenue numbers.

b. There shall be a uptake in revenue as company will start production & deliveries.

3 Likes

Titagarh Rail Systems | Management Interview

- Looking at shipbuilding & maritime biz as the next engine of growth for the company

- Current order for shipbuilding & maritime is approximately ₹300 cr, involving the construction of 10-11 vessels for the Indian Navy

Watch the interview here

2 Likes

new update.

1 Like

Titagarh Rail Systems | Management Interview

- Wagon execution has improved in Q4 vs Q3FY25

- Company will stop wheelset imports from China from next year after the JV with RK Forgings commercialises

Watch here

1 Like

Titagarh Rail Systems | Know Your Company + Management Interview

1 Like

Three concerns come out wrt to KYC video:

-

Constantly decreasing promoters’ shareholding

-

Everything related to future comes in FY 27

-

Very ambiguous answers to critical questions.

4 Likes