I only focus on the music business…

Far from superb for me at least!

Music streaming business - the last 4 quarters revenues have been very flat at 29-30 cr revenues.

I don’t think there can be much seasonality in consumption of music, so this is concerning as a shareholder that there is no growth.

Will be quizzing the management on the concall.

12 Likes

I am a bit surprised to see lumpiness in a business which should have a continuous revenue cycle. I am actually confused by the result  eagerly waiting for the con-call.!

eagerly waiting for the con-call.!

2 Likes

As i interpret the results, the margin in streaming business is down as they have acquired music rights, could be the songs of “Bhoot Police” that have released last qrt, as the music and movie business are separating i believe they would have paid the fees to the other division so that there is no ambiguity when the diversification happens.

2 Likes

Their music not there on Gaana & Wynk is really hurting them, as both the apps control significant market share.

The closing of these deals (with Gaana & Wynk) & the demerger can lead to re-rating / PE expansion, & possibly bring it at par with Saregama.

9 Likes

2 Likes

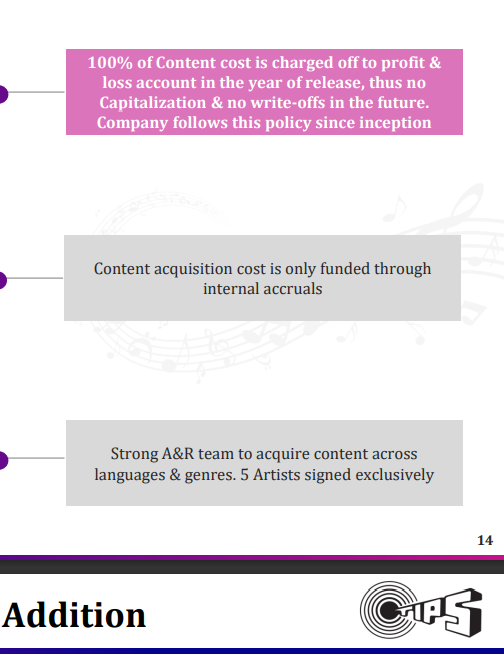

Unlike Saregama, Tips charges content cost to p&l, and go forward if the music is hit it only brings disproportionate retained earnings to balance sheet.

Also this exactly is the reason why thrre is difference in saregama mergin numbers vs Tips and will be there always.

Also in last Concall management guided that they arenin talks with either Wynk or gaana. So let’s ask on updates on that.

Astronomical margins on film division will repeat? Too early to bet, what we have to ask on Concall is if there has been any structural change in the way Tips manages that business, this is the only way we can have some sense of odds for films business.

Disc - invested in both. Tips for special situation (DEMERGER) and Saregama for 4x the content Asset (more content brings more cash flow that brings more content and the cycle goes on till some external force kills it which I can think does not exist as of today), also both have mutually exclusive content so this gives me exposure to India wide content base to leverage this theme. Unless Management does something really stupid - these business have very strong tailwind, here to stay.

8 Likes

Cant agree more here, my investment rationale is very much like yours. I keep a music only P/L and value/judge performance purely on basis of that, it helps ignore lumpy business of films and keeps focus on the reason for buying TIPS. If there is anything remarkably positive from films it is a plus. Like others’ my top of the mind question is also on QoQ music growth, let us listen to reasons from management tomorrow.

1 Like

Few updates from the management concall -

- Gaana/Wynk deal - Discussions are still on, however management feels that these streaming platforms are trying to squeeze players such as Tips which are not in the top 3. If they agree to their T&C, it can potentially reduce Tips’ bargaining power with other platforms as well. Hence, they are happy to wait till whenever these guys offer the same deals as the top music labels.

My take - I do not expect this deal to be cracked in a hurry. I think if Tips acquires enough high quality content (big artists / big releases, etc.) in the next 6-12 months, the streaming platforms would be forced to offer them the same deals. They’ve acquired film music for 3 of the biggest Punjabi superstars (Diljit Dosanjh, Ammy Virk and Sidhu Moosewala) with all 3 films already released in the past couple of month. All 3 of them have a huge fan base in the North. So it’s not a bad strategy from the management, however they need to demonstrate this content acquisition in Bollywood as well which will tilt the bargaining power with these streaming platforms in their favor.

- Business Growth - Management is extremely confident of maintaining 15-20%+ topline growth in FY23 as well even without Gaana/Wynk deals being cracked. They mentioned that the new content acquisition, growing streams on platforms such as Youtube, etc. should be enough to give them this kind of growth with slightly lower bottom line growth as content acquisition costs need to be written off upfront.

My take - I’m not completely convinced as yet how they will deliver this growth. However, I firmly believe in the phrase “innocent till proven guilty”, so I will give it 4-6 quarters to see if management is walking the talk. They’ve confidently stuck their neck out promising that growth will continue, I would like to give them some time to deliver before coming to any conclusions.

- Demerger and Films - Promised not to do any ICDs post demerger between the 2 businesses and cash flows of each company will be separate at all times i.e. music streaming business free cash flows will not be used to fund any film business related activities, that is the whole point of the demerger isn’t it. On films business, I just recall one thing - they’d be doing 2-3 film releases every year.

Note - I dropped off from the concall after my questions, hence this would not be the complete summary.

16 Likes

Notes from Q2FY22

-

“TIPS rewind” project:

- Every week 1 song. Total 12 songs. Jagjit Singh Ghazals

- All songs will be released in next 3 months.

- Sponsored by Skoda so no downside.

-

25-30% Topline. 15-20/25% bottomline (this is less than sales growth because of new content cost).

-

Releasing 300-400 songs in year is the target.

-

Status on Gaana deal: Talking to them but not finalized.

- Management not in hurry for the deal.

- If one doesn’t have the song on Gaana they would listen to the song on another platform.

- Management says they have to maintain market share and if they agree to the terms it will affect their image and other players will also start negotiating and corner them as they are not the top 3 players of the industry.

- Gaana and Wynk represent 40% market.

- Management says that TIPS is able to grow without them also which shows that they would be needing us more and it will hurt them in long term.

- If we start focusing on stock market and give in for the lower deals then it will bite in the future.

- I recommend listening to the last question: at 1:04:35

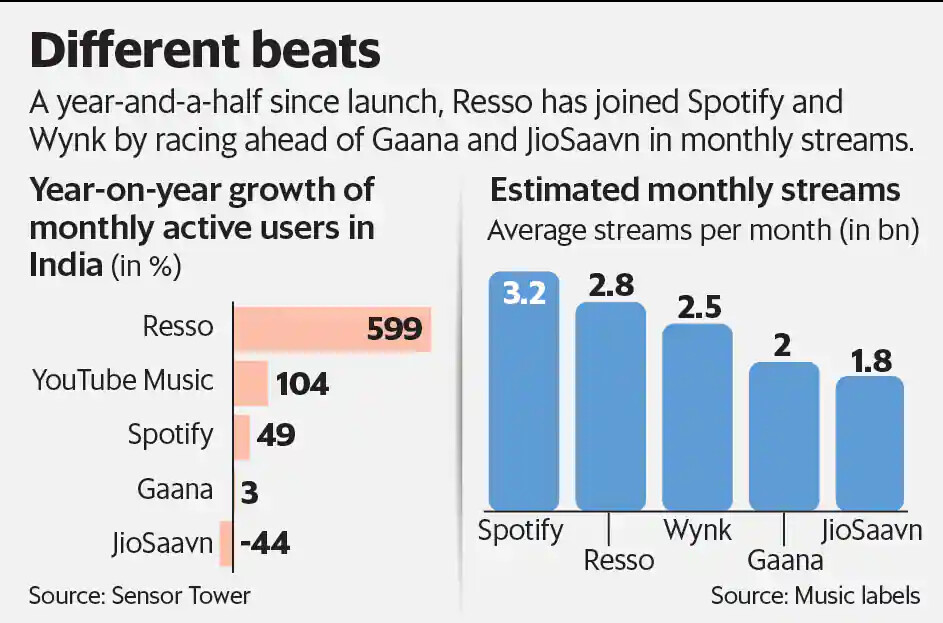

- https://www.livemint.com/industry/media/bytedances-music-streaming-app-resso-quietly-climbs-to-top-of-popularity-charts-11635359505380.html

- Management not in hurry for the deal.

-

They are not in a competitive state and not hunger for content at any cost.

- They expect to recover content cost within 2-3 years.

- Accounting policy is to write of content cost 100% at the time of release itself.

-

Demerger:

- By January 2022 Demerger should happen.

- What are the plans of Free cash flow generated from music business?

- Invest in content acquisition but not aggressively and entering into competition

- Buyback or Dividend is also an option.

- Management assures that they would not use cash of music business for film business.

-

Spotify deal is limited to Hindi catalogue!!

- Warner deal last year was limited to Hindi songs.

- Each music label is not there in some other app.

-

In 2001-2002 they had acquired 12 labels one of which was TIME music

- 2-3 years ago they acquired 2 small Punjabi labels.

- Acquiring small players is a part of business and they will keep looking for this opportunity.

-

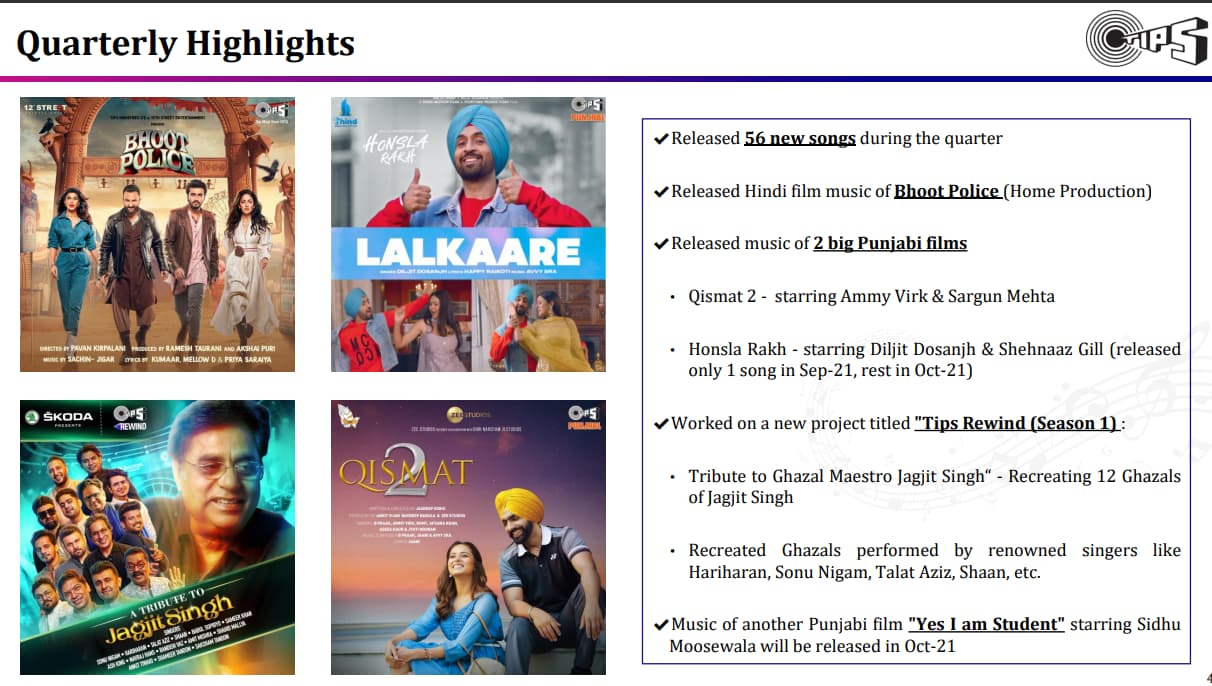

Sold Bhoot Police license for 10 years.

- Outright worldwide deals except China.

- Whole industry is doing like this.

- So, technically one can’t make lose here.

- Whole industry is doing like this.

- Outright worldwide deals except China.

-

Target is to achieve no.3 position.

-

Q: Why music revenue are flat?

- Price is flat but stream is increasing

- They have to rethink about their market share strategy

- They have to get in with Gaana and Wynk.

- If these things happen growth would be much higher than guidance

-

Management says don’t measure them on QoQ basis because it depends on which deal is maturity or renewing. YoY is a better indicator.

-

They have 500 songs which they can recreate and monetize.

-

Comment on Saregama raising money: “Relationship also matters. Competition was their earlier also. let’s what happens.”

-

They are looking for professional to increase their business.

- Promoter would not leave the business they just want a bigger team.

- Management says they love their business and not going anywhere

- This clearly hints that Saregama is not acquiring TIPS (For those who were curious).

20 Likes

Good coverage from @gurjota and @arjunbadola. Not much to add on call, sharing some insights n learnings on how we as investors expect vs biz model and therefore disconnect in some areas.

- QoQ vs YoY - Music deals with some platforms are lumpsump blocks and renewed every 1-2 years. The kicker or upside doesn’t reflect in numbers till revised deal happens. Tips have been guiding 25% + top line at YoY even though flat QoQ for past 3 qtrs.

- Youtube should be flowing regularly, though Tips didn’t share many details, we know that Subscribers are growing MoM.

- Enough covered in notes above for Gaana and Wynk pending deals - Tips clearly sees value on hard bargain for now. Catalogue valuations seems to be issue where both parties see different value.

- While everyone is focused on music, Tips sees value in Films as well and plan to get into web series as well.( Saregama is highly valued despite having Yodlee films, Carvaan, Open magazine biz) - Narrative changes fast if numbers are delivered in film biz as well.

- Content acquisition and refresh focus is visible.

Lot hinges on Mr Taurani assurances for now, as numbers aren’t speaking for themselves.

Valuations:(Music) FY 21 was 91 cr revenue and PBIT of 73 cr. FY22 per mgmt claims could be 110 cr revenue 85 cr PBIT , at 30 PE, the music biz could be closer to 2000 Cr mkt cap ( another way to look at Saregama has 3.5 times content library so 1/3rd of Saregama music biz valuations).

Invested

8 Likes

Even the to-be demerged film business can be interesting ahead.

-

Like music even the Film business is transitioning, if you see in the past few years Tips films division has only caused losses as it was hugely dependent on the box office collection.

-

This has changed now with OTT, that too so many players have entered in it ( Netflix, Amazon, Hotstar, Zee, Sony, Voot & many more ) who have to churn out high no. of content on a regular basis.

-

Which leads to getting huge prices for the digital rights.

-

Even in the concall Mr.Taurani said that it’s very unlikely you’ll make a loss in any film now, & from now on they’ll aim to make atleast 3-4 films every year.

-

& with latest films you get latest music starring famous actors for the Tips music catalogue too.

-

Another Interesting thing from concall was :- Tips has even bought Rights of some books & scripts to make web series too.

I definitely wouldn’t buy Tips films more , but might hold onto the the shares I will get due to the demerger.

5 Likes

Management comments on not wanting to undersell to music platforms makes a lot of sense. Clearly, Gaana and Saavn are losing market share rapidly and may be under pressure to start talking to Tips once again.

6 Likes

Pursuant to the Order of the Hon’ble National Company Law Tribunal, Mumbai Bench (“NCLT”),

dated September 22, 2021 (“Order”), the meeting of equity shareholders of Tips Industries Limited

(“Meeting”) was duly convened and held on Thursday, December 2, 2021, at 11:00 a.m. (IST)

through VC/OAVM, for the purpose of considering and approving the Scheme of Arrangement and

Demerger between Tips Industries Limited (“Demerged Company”) and Tips Films Limited

(“Resulting Company”) and their respective shareholders under section 230 to 232 and other

applicable provisions, if any, of the Companies, Act, 2013 and rules made thereunder (“Scheme”).

All the requirements and procedures to be followed pursuant to the Order(s), circular(s) issued by

the Ministry of Corporate Affairs (“MCA”) and Securities and Exchange Board of India (“SEBI”)

towards conduct of the Hon’ble NCLT convened meeting through VC/ OAVM were observed and

followed.

The Chairman announced that the e‐voting results along with the consolidated Scrutiniser’s Report

will be informed to Stock Exchanges and also be placed on the website of the Company and CDSL

within 48 hours from the conclusion of the meeting.

From Negen PMS newsletter which is freely available

First, lets talk about Katrina and Vicky’s wedding.

*No, I do not have any gossip to share!

*No, they have not paid me to write about them. (They should have!)

Seriously now, there is an important and relevant thing for us to learn from this wedding.

Amazon Prime paid the couple a whopping INR 80 crore for the ‘Rights’ of their wedding.

We had been learning about the dramatic ‘Battle Royale’ ongoing in the OTT space between Netflix, Disney Hotstar, Amazon Prime and many other smaller players.

(Data was the old ‘Oil’. Now, ‘Content’ is the new ‘everything’).

For Gods sake, our Tips Industries made Bhoot Police for 40 crore and sold just the Digital rights for 60-65 crore.

Music rights or licensing fees will bring extra over many years.

So Bhaiyon and Ladies, we live in a world where Bhoot Police makes 25cr plus more royalties and some Bollywood wedding makes 80cr.

So, what is the point of all this data you ask?

Enter Tips Industries (Special Situation- Demerger):

- Tips Mcap is 2111cr today.

- Tips Music-Tech division is expected to earn Revenue of 150cr approx with PAT of 55cr in FY23 (estimated).

- The Music-Tech business with near 50-60% PBT margins, no debt, extraordinary FCF, 25-30% growth is available at just 38x earnings.

- That leaves us with the production business where Bhoot Police jaisa movie earned 20-25cr. What if they can do 2-3 such releases per year post demerger without shareholder pressure anymore?

- The production entity could earn 40-60 crore per year (pre tax) potentially?

- So how do we value such a business? Maybe 20x-25x PE? (Is potentially 1000cr worth of valuation hidden away inside Tips?)

You do the Math.

16 Likes

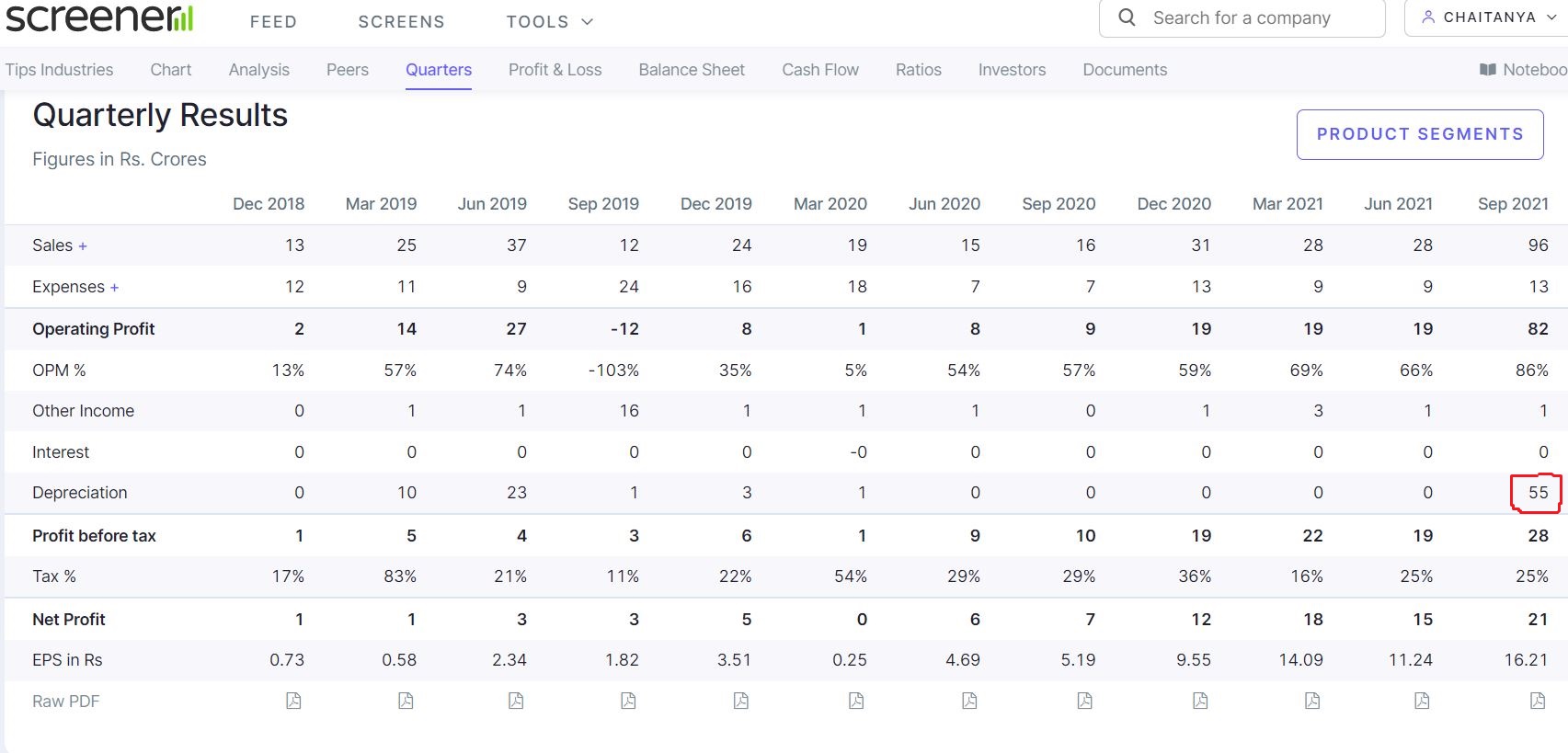

Can someone please explain how they suddenly got such a high depreciation cost? Is it because of the sale of ‘Bhoot Police’? If yes, can someone please explain the logic behind this?

1 Like

exactly what i tend to believe !

Tips has aggressive cost absorption policy in first year itself for content, believe it was discussed in concalls.

2 Likes

Yes, but why has this been considered in depreciation, you can see that in the previous quarters when they acquired music they font have any depreciation cost.