Incorporated in 2006, Timescan Logistics (India) Ltd does business of providing customs clearance & surface logistics services viz. goods transport service along with warehousing facilities. The company provides complete range of services like Freight Forwarding (Sea & Air freight), Custom Clearance, Warehousing, Multimodal Transportation, Project cargo, Third Party Logistics, Packaging, loading/ unloading and unpacking of items to facilitate our customers with end-to-end solutions and other related value-added services. They have asset light business model which allows for scalability of services as well as flexibility to develop and offer customized logistic solutions across diverse sectors.

In January 2022, company came up with an Initial Public issue of 9.44 Lac equity shares at a price of ₹51/- per equity share. Total equity capital of the is 3.49 crores. Promoters hold 73% of shares.

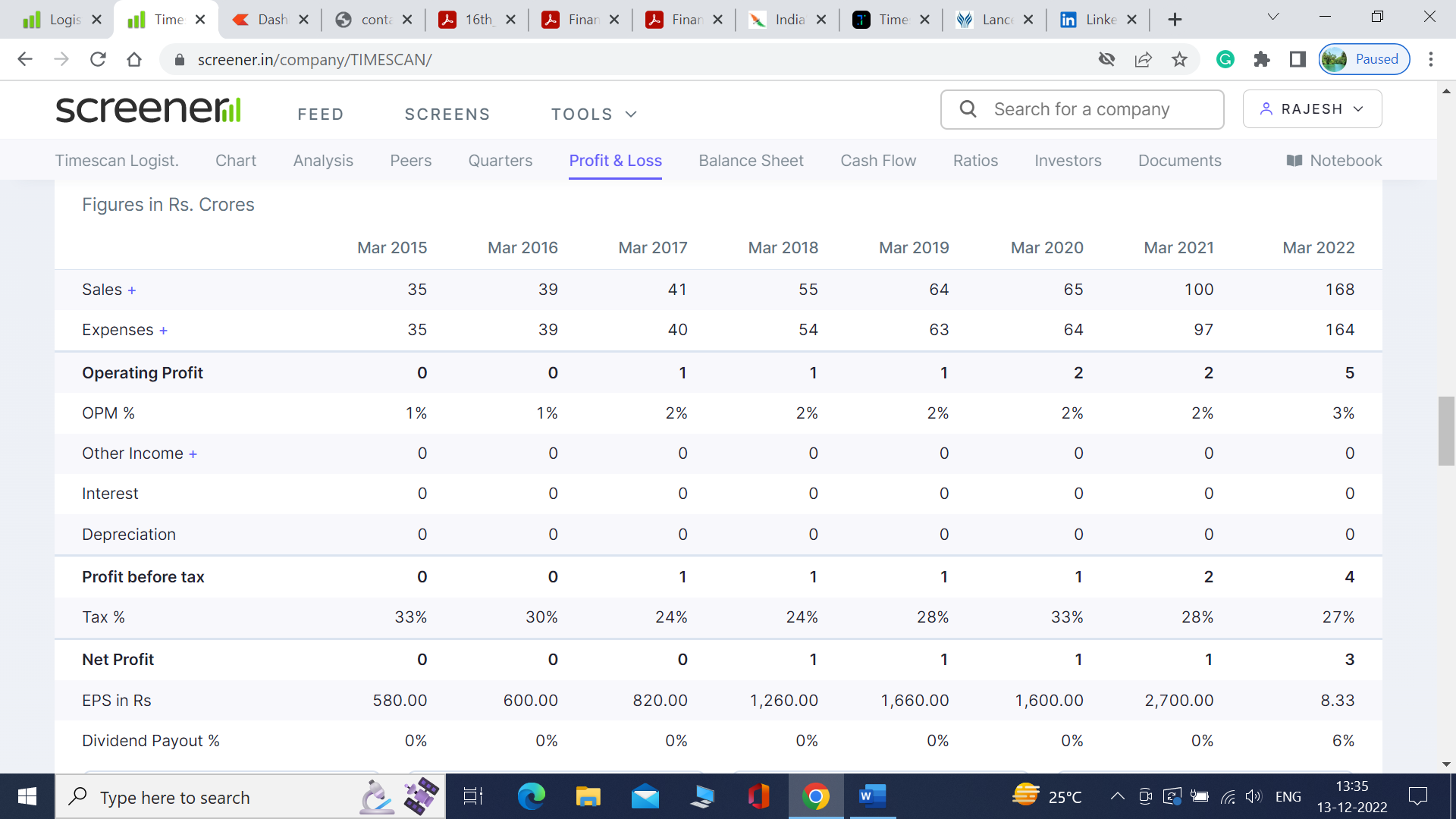

Financials:

The company is a micro cap company [M-cap of around 50 crores, Equity capital 3.49 crores and current market price Rs. 142]. Last 8 years financials are as follows- [From Screener.in],

The company is growing at a decent pace, whereas in the last 3 years the pace of growth has been accelerated. The company has put up very good performance in H1-2023,

Based on past growth, and H1 results, I expect the company to do a topline of 250 Crores, with net profit of 5 crores in the FY 2022-23.

Based on the above estimate, eps shall be Rs. 14. Market is being traded at 1/5th of expected sales of 2023. Further, the company gave maiden dividend of 5% in 2022, we can expect the dividend payment to go up going forward.

Business:

On the face of it, logistics looks like a commodity business. There is no reason for a customer to pay higher price. However, such companies have a benefit- from the customer’s point of view it is “salt in the kitchen”. Cost of logistics is miniscule as compared to the cost of goods. Thus, customer’s may not be very price conscious in this business, and an efficient player can gain an upper edge.

The sector is undergoing a transformation. With mandatory E-way Bills and electronic invoices, the business is shifting from unorganized to organized sector and probably listed players will benefit from that.

Asset light business model allows the company to generate decent RoE on thin margins. Promoter and management team seems to have reasonable amount of experience in logistics industry.

Investment Thesis:

-

A logistics company is available at an attractive valuation- 1/5th of current year topline, 10 times current year eps. The company is also dividend paying.

-

The sector is great tailwinds in terms of shifting of business from unorganized to organized sector.

Risk:

-

Investing in Micro-cap is extremely risky, it can result in lost of 100% capital.

-

The company is still reporting negative cash flow from operating activity.

Disclosure: Invested. Planning to add more.