Good thread on TTL

2 Likes

Ttpl results:

Great revenue growth (higher than any pre-pandemic sep quarter)

Ebidta margin (14.4%) increased yoy and qoq (which is surprisingly excellent given all the cost inflation going on)

(also shows their ability to pass on cost increases)

Composite products showing robust growth and high profits

(value added products revenue share - 22%) (ebidta margin-17.4%)

Current type iv cylinder order book at over 150cr in a very short time span

Cash flow generation is good

Valuation - If I extrapolate current half year earnings (ebit) (first quarter was significantly hit by covid) and discount it by 10% COC, value per share is coming at 109rs.

If current quarter earnings are extrapolated, than value per share is coming at 130rs.

1 Like

This is old order for CNG Cascade.

Overall the result is good. However, Lets wait for Managements comment on EVs destruction on CNG. How EV is going to affect CNG vehicle adaptation…

I am more bullish on LPG composite cylinders than CNG. Let’s see whether piped PNG will have any impact on LPG. Let’s wait for concall to get these updates…

Also, I am bullish on HDPE & DWC pipes. HDPE pipes can be used instead of Ductile Iron pipes for under ground Fire fighting & Potable water applications…Because HDPE pipes are cheap, easy for handling and installation. HDPE pipes are long lasting, have no effect on water quality and easy to repair compared to ductile iron pipes.

I don’t think that growth in EV is any way going to impact CNG and cascade business in the next 10 years…

1 Like

I participated in concall today… Management is very much bullish on future growth potential…According to management

- EV (for Cars and Heavy vehicles adaptation) is not so easy as projected. It will take 10 more years for widespread adaptation even if everything goes smooth. Lithium iron batteries are mostly coming from China.

- Instead Management feels hydrogen vehicle will be widely used in future. Company is working on composite Hydrogen cylinder which will require to withstand 1250 bar pressure. Reliance is working on hydrogen fuel technology in India.

- Company got another 30,000 LPG cylinder order from OMC. Getting continuous orders from overseas. If demand from India picks up, existing capacity will not be enough to handle orders.

- Expecting more orders for CNG cascades.

- Next 2 quarters results will reach to pre-Covid level.

- Got some battery order from Tesla. Getting many inquiries. But company not interested in Battery division. Planning to divest/exit as committed earlier.

5 Likes

Audio recording of concall

5 Likes

Prestigious Single Order Of INR 80 Crores (Appx) For Type-IV Composite Cylinder Based CNG Cascade

We are pleased to inform that the Company has received a prestigious single order from renowned

Public Sector Gas Distribution Company for supply of Cascades with Carbon Fiber Reinforced Type-IV Composite Cylinder. This order is in addition to earlier communicated order booking of INR 150 crore (approx.).

No further details are available in the note…

3 Likes

2 Likes

Latest management interview

Here are my notes from their December concall.

08.12.2021 (Investor meet)

- CNG cylinder business and other value added business can achieve EBITDA margins of 20% with lower working capital requirement. Company is already transitioning the value added business segment to cash and carry model leading to improved working capital

- Pricing contract with customers: 40% on quarterly basis, 40% on monthly basis and the remainder on spot basis

- Gas cylinders: The only two domestic players are Supreme (capacity: 0.5 mn) and Time technoplast (capacity: 1.4 mn). The current tender orders from OMCs will be served by these two. Next 2-years capacity of Time Technoplast is fully booked

- Will reach pre-covid business levels in FY22

- 12-15% EBITDA margins on packaging business with ROCE of 13-14% which can go to 17%. Cannot improve working capital situation much due to industry structure

- Imports 60% of raw materials, with new HEML plant coming up import will be gradually reduced to 40%

- Battery segment will be divested, currently its getting very good traction with orders from reputed clients like Tesla in their solar segment. The orders will increase visibility so that the entity can fetch good value

- FY25 revenue target is ~5000 cr. with ROCE of 20%, with established to value added products mix of 55:45 (a similar debt profile as of today will be maintained with debt not exceeding 2x EBITDA)

- FY22 CAPEX ~ 140-150 cr. (growth capex of 70-80 cr. and remaining is maintenance capex)

- For a 1 mn cylinder capacity, capex required is 60-70 cr. and project completion is 6-8 months. Not planned any capex for the pipe and tehpaulin products

- Current capacity utilization: 70-72% (on consolidated basis), Division wise breakup

o Packaging: 70%

o IBC: 75%

o Battery: 50%

o Infra related business: 50%

o Automotive: 50%

o LPG Cylinder: 75%

o CNG cylinder: 90% (on a small base) - Based on existing capacities, company can achieve annual turnover of ~4000 cr. For the additional 1000 cr. to reach 5000 cr. by FY25, cumulative capex that is required is 500-600 cr. (including maintenance capex)

Disclosure: Invested (position size here)

6 Likes

Current turnover is 3500cr and it is trading at Mcap of 1750cr. They will only increase turnover by 1500cr by 2025?

Top line may grow at 15% CAGR but bottom line profit expected to grow at 25% CAGR. It is trading at 10 PE and below book value. If it grows by 25% bottom line and 20 ROCE, there will be PE re-rating.

4 Likes

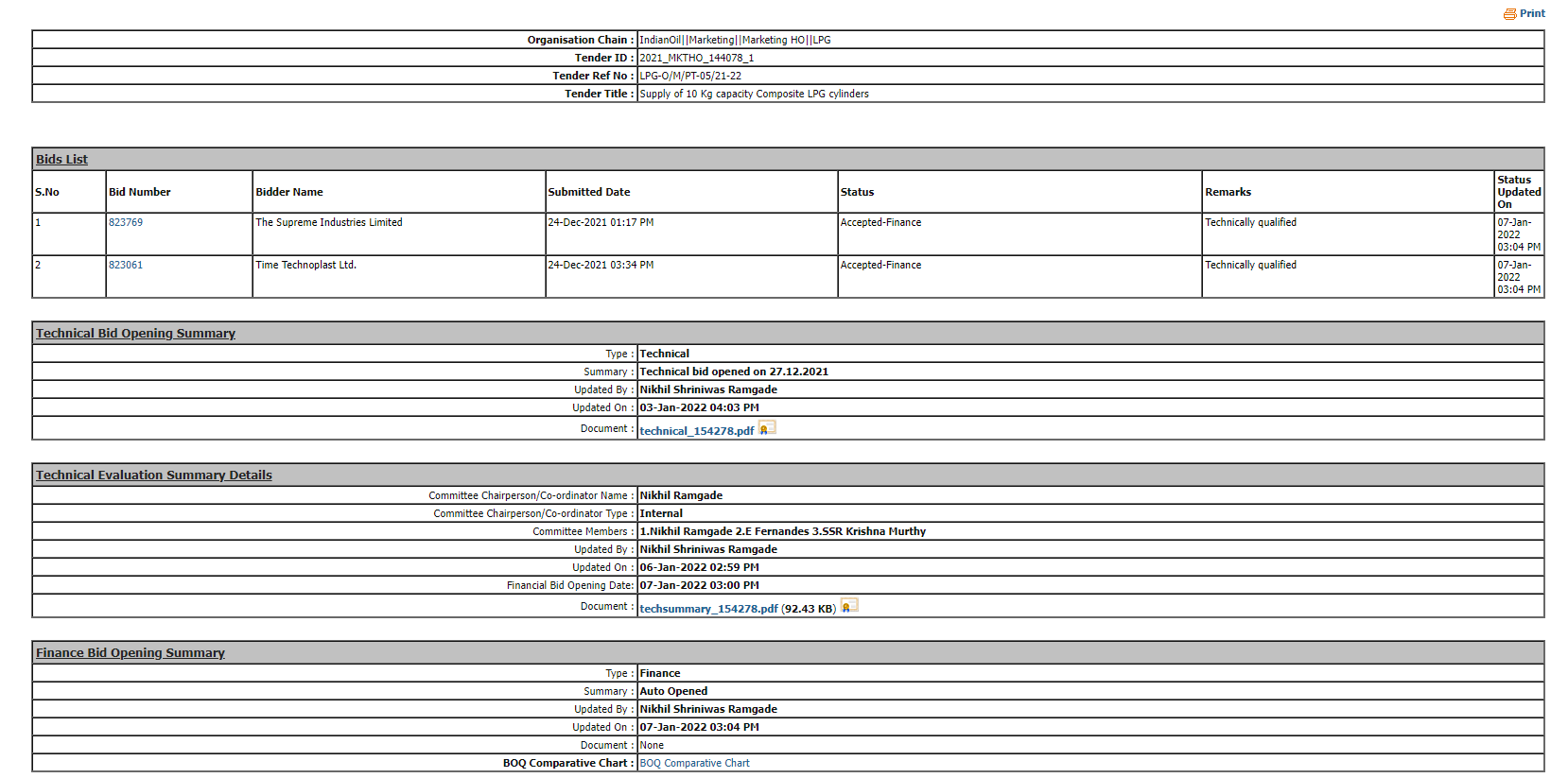

LPG Composite bid tender financial bid status is released. Time Techno plast & supreme indusdries are going to get orders of 7.49 lakh cylinders (each) worth 180 Cr(each). Official announcement is expected any time soon. Note the below screenshot from IOCL tender website.

9 Likes

Nice to see the LPG cylinders have hit the market, going by some of the Indane tweets retweeted by the LiteSafe handle

At roughly Rs.2400 per cylinder (going by the tender post above), what is the opportunity size for LPG cylinders? Has anyone done the math? Am assuming there are about 200 million households and at 98% penetration, the number is quite large at close to 50k Cr, assuming each of those steel cylinders get replaced over time. Not sure if this is the right way to calculate opportunity size here though. If the adoption and market response is good (first signs are encouraging), this can be a huge opportunity.

Steel - Composite cylinder price differential narrowing can also drive demand up, along with the operational cost savings from the weight reduction by 50% and the transparent window offering good customer experience in knowing when the cylinder will get over.

Disc: Invested from around 78 levels last month

10 Likes

Promoter and MD Mr. Anil Jain passes away and is replaced by another promoter director (Bharat Vageria). This is sad news, Mr. Jain was quite young. From a succession planning point of view, its probably okay because all the 4 original cofounders are still directors in the company, but its quite sad news.

2 Likes

Very sad to hear the demise of Mr.Anil Jain. It is big loss for TTP. He is a kind and ambitious person. He answered all my queries in concall patiently.

Rest in peace sir.

3 Likes

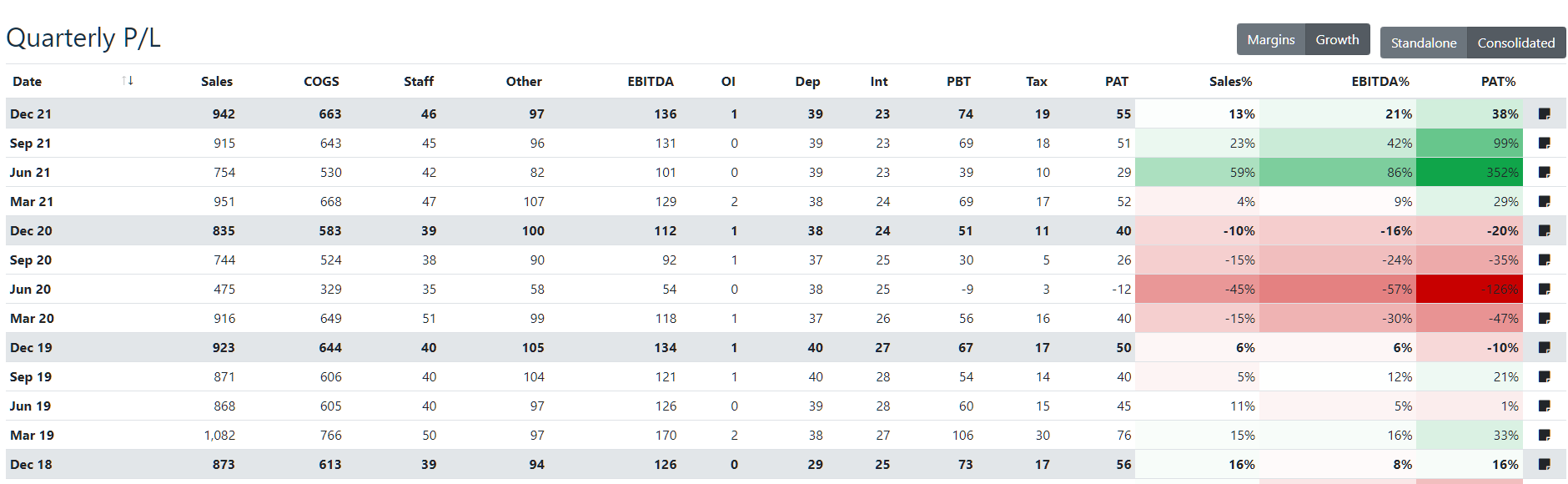

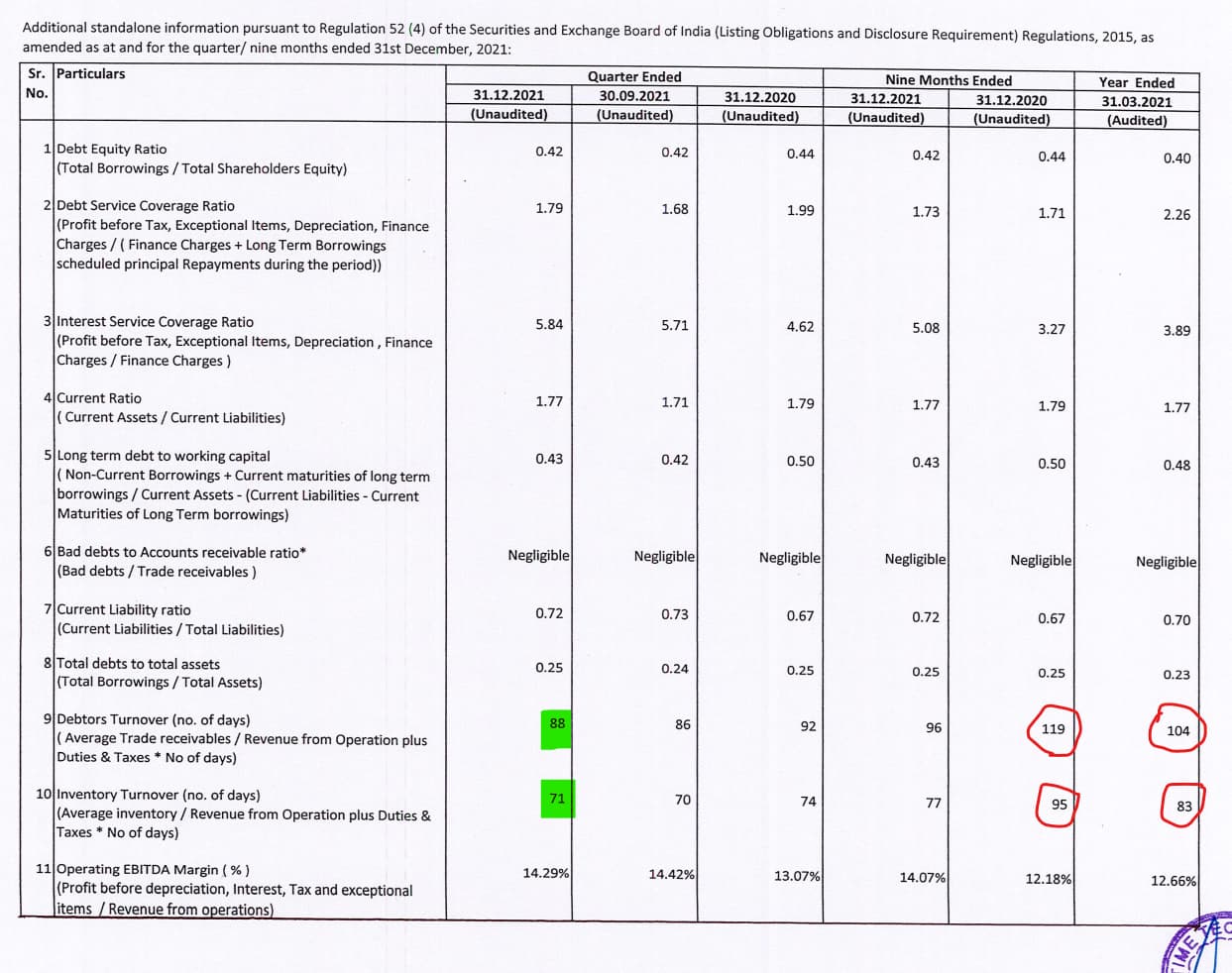

Pretty good results. I was expecting a 200 bps margin compression (12% OPM) but they have delivered a 14% margin like usual which is great. Healthy growth continues and now the business is back at pre-pandemic levels and near all-time high EBITDA although price is trading 65% lower than ATH

There are reasons for that though, even before the MD’s unfortunate demise. FY21 not only saw deterioration in performance in PnL but also in working capital.

However this has been management’s focus through this FY and there are significant improvements showing already. Thankfully this business reports working capital metrics quarterly, which not many do.

With debtor days of 88 and inventory days of 71, the working capital as well should be now close to a 100 days (103, if we keep payable days same as 56 or an all time best number of 89, if we take pre-pandemic payable days of 70).

So more than the PnL being a beat, it is the working capital improvement that is more encouraging. Also the RoCE should return to close to 15% and climb up towards 20% as well in the next year or so.

The cash profits have consequently been going up as well. Although the reported PAT is around 50 Cr, the cash profits are around 90 Cr. If we take 9month, this cash profit number is 252 Cr. So for FY22, its possible that we close at a cash profit of 350 Cr and with current valuation the business is available at less than 5x cash profit.

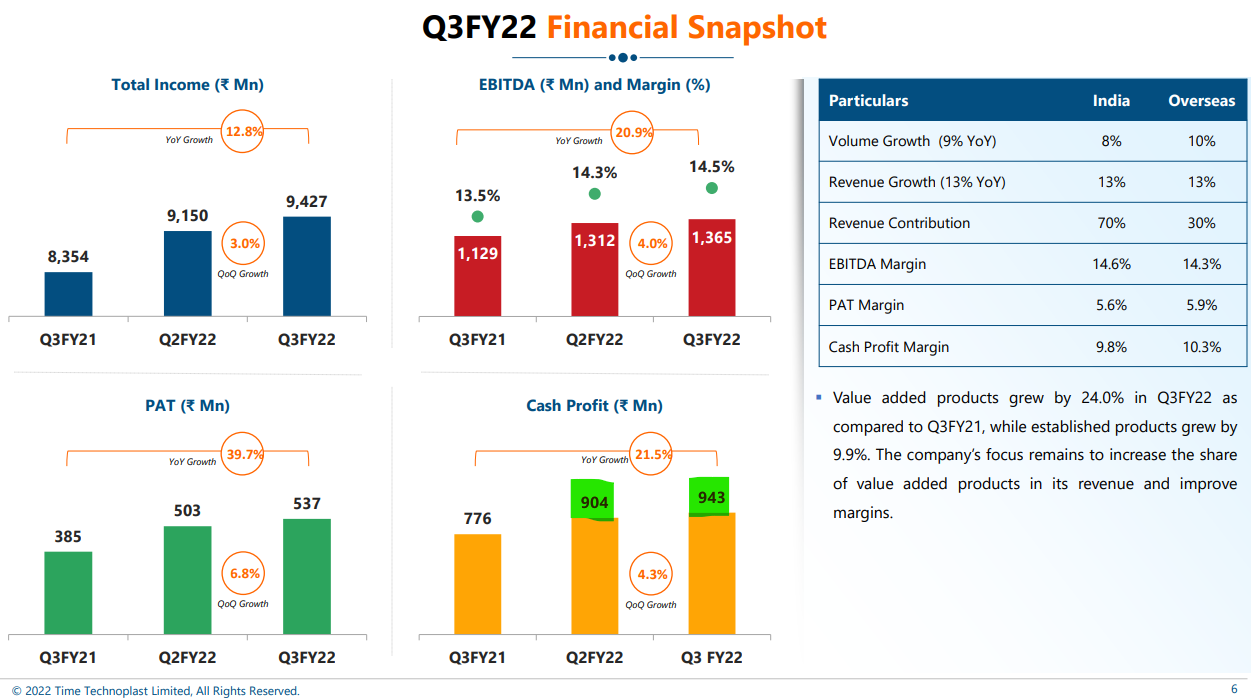

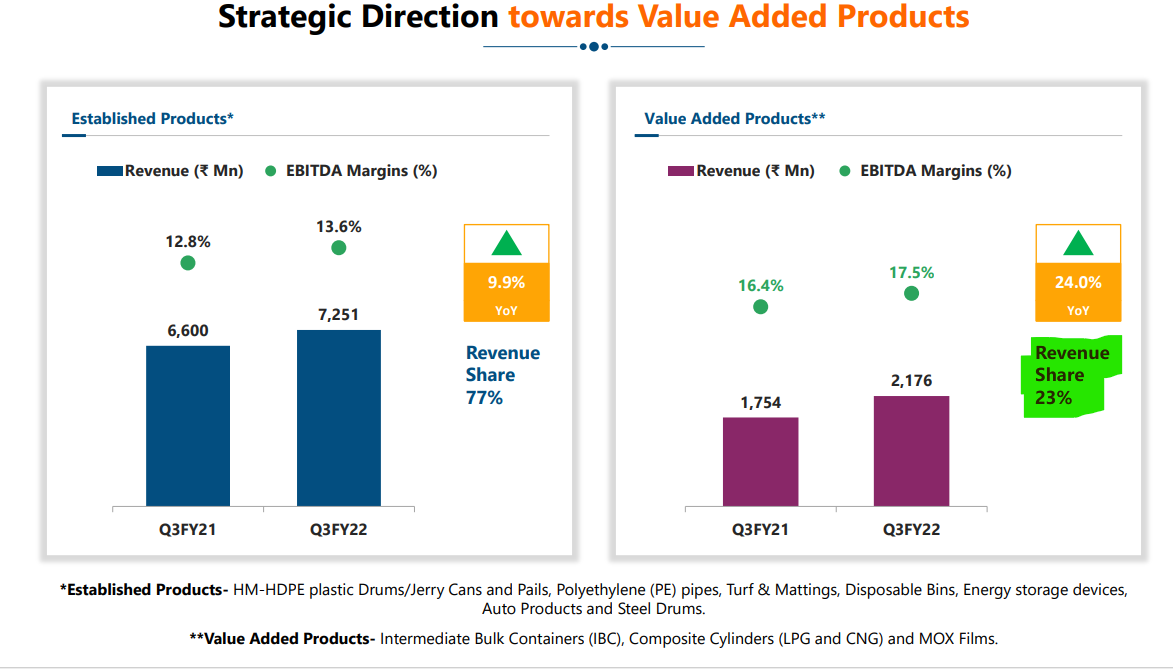

Value-added products has been increasing in revenue share with a healthy growth

Some highlights from the presentation on composite product order in the last 9 months. CNG cascades are doing well and the LPG composite cylinders as well are breaking through with first orders after the trial order.

A brief on the products, sectors and clients

Disc: Invested. Have position around 78.

20 Likes

Its indeed surprising that they have been able to increase margins in inflationary times.

Your observation about working capital improvement is also something management talked about in great length in their December call. They are moving their value added business to a cash and carry model, which implies that working capital situation should improve further as value added business becomes a larger part of the pie. About valuations, its still very cheap.

Disclosure: Invested (position size here)

6 Likes

FY22Q3 notes

- Vishal Jain (son of Anil Jain) has been appointed as additional non-executive director. Shares held by Anil Jain is being transferred to his wife and they wont be sold

- Target FY25: Working capital: 85-90 days, ROCE: 20%, Value added business: 32%, Consolidated margins: 14.5-15.5%

- Maintenance capex: 70-80cr.

- Planned growth capex of 175-200cr. for fulfilling current orders

- US revenues: $36mn in FY22 ($18mn in FY21). Expecting $80mn by FY25. EBITDA margins are 13-14%. Currently operating at ~60% of capacity utilization

- Existing steel cylinder market ~ 36cr., 2cr. is annual replacement demand. Time Technoplast can do annualized sales of 2-2.5cr. in composite cylinders. Expecting to do 500cr. in FY23 from composite cylinder (against 250cr. in FY22; 164cr. done in 9MFY22)

- CNG type 4 cylinders: CNG cascade market is high growth (and highest priority). Also working with OEMs (second priority) and retrofitters (last priority) for on-board cylinders in passenger cars and buses. Take 2-3 years of development timeframe to get orders from OEMs

- Fulfilled 5cr. worth orders to Tesla, working on other segments (like lithium ion battery) with them. Might have 180cr. business with them by FY23. Will sell that business line at appropriate valuations

- Non-core asset divestment (extra buildings, furniture, etc.) in US. Should generate ~60cr. Looking to finalize in 6 month time (for sure by end of FY23)

- Value added working capital cycle is ~60 days (mainly because of raw material and finished product inventory to be maintained). Margins here is 18-22% (will do margins closer to 19-20%)

- Oil and polymer prices are not directly related, 30% increase in crude prices has not translated into proportional increase in polymer prices

- Debt should not increase over 2x EBITDA

Disclosure: Same as before

6 Likes

CNG growth is here to stay for at least 1 decade. Increase in number of CNG station and vehicles will have a positive impact on TTPL.

The current valuation gives lot of factor of saftey. Promoters are professionals and first generation entrepreneurs. Gone through concals of last 2 to 3 years, Mr Vagheria has clarity on Business outlook and is open for discussion, clarification and disclosure with Investors. Overall the Company seems to be investor friendly.

The Company apparently seems that it will take care of minority shareholders once performance further improves.

Disclosure: Invested and forms 5% of my portfolio.

5 Likes

When the management mentions that they supply batteries to Tesla, are they referring to Musk’s Tesla?

I have my suspicions that they’re talking about this company https://teslapowerusa.in which I found while randomly searching on Google

4 Likes