Here you go

1 Like

Time Technoplast (TTL) is a market leader in manufacturing of polymer drums. Out of the total drums requirement in India, 55% is polymer based and 45% is steel. The drums market was 100% controlled by the steel drums before the company started its operations. The company is pioneer in substituting steel drums with plastic in India. TTL has a 70% market share in polymer drums (Balmer 15%, Unorganized 15%) contributing 60% to the company’s total revenues.

Product-wise revenues split (FY20)

The company was founded in 1992 by 4 promoters viz. Anil Jain (Founder), Bharat Vageria,

Raghupathy Thyagarajan and Naveen Jain.

All the promoters used to work at Prestige HM-Polycontainers before leaving their jobs and starting

Time. Interestingly, all the promoters are holding the same position in Time (Anil Jain-Overall, Bharat

Vageria-Finance, Raghupathy Thyagarajan-Marketing and Naveen Jain-technical) as they held in

Prestige.

Total Indian drums market size is ~20mn, of which, 55% is polymer and 45% is steel. Out of the 55%,

TTL has a 70% market share, followed by Balmer Lawrie with 15% and unorganized markets holding

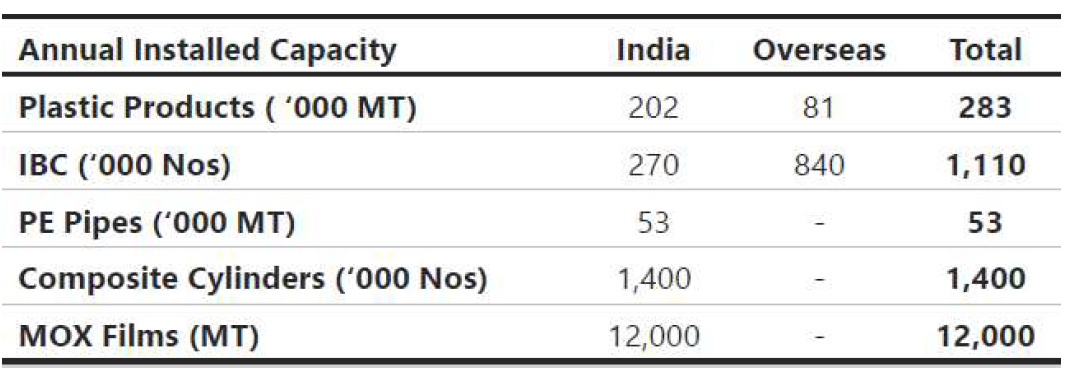

the balance. TTL has a manufacturing capacity of ~2,80,000 tons (~2L in India and 80,000 in

Overseas). Each ton yields 117 drums (large size viz. 200 liters).

70% of the company’s revenues is generated from packaging products viz. Polymers and IBC (Intermediate Bulk Containers) The company has lot of marquee names in its clientels viz BASF, Clariant and Dow Chem.

IBC is equal to 4 large drums size. Each IBC has a storage capacity of 1000 litres.

The packaging biz of the company fetches ~14-15% EBITDA

In the balance 30%, company has pipes (PE and DWC), MOX films (higher value version of tarpaulin), Composite LPG cyliders (2kg-22kg) and balance is batteries & automotive components.

Company bifurcates its product line in two categories: Established (EBITDM% 14-15%, 80% of total sales) and Value added (EBITDM% 16-19%, 20% of total sales)

The company has done aggressive capex in the past 7-8 years, the results of which are yet to be fully optimized. At an avg asset turnover of 2.2x, the company has potential to generate INR 5000-5500cr topline (FY20 revenues 3600cr) from the existing asset base

Value added products: IBC, Cylinders and MOX films

Established: Pipes, Drums, jerry cans, pails, batteries and automotive components

Valuation

The company is trading at 4x P/E, 0.5x P/B, 0.26x Sales and 3x EV/EBITDA.

In 2016, one of the company’s global competitor Mauser was acquired by a PE fund at 1.5x sales, 8x EV/EBITDA and 8x P/B). TTL looks extremely attractive at the current juncture.

Capacities

The company has an existing gross block of ~INR 2500cr and the management states that it has an

asset turnover of ~2-2.5x which translates into INR 50-60bn topline with the existing base, reflecting

sufficient headroom available.

Overhang on the stock price:

The promoters created a pledge 3-4 years back (and also sold some stake). Today, the pledge stands at 17% of total shareholding and 34% of promoters shareholding. Promoters holds 52% stake in the company.

As per the concalls, the promoters created this pledge to develop a land parcel they held in the personal capacity. Although the pledge is there, it is very less relatively.

The company ventured into a non core venture viz. battery business. Battery biz is a small part of company’s total turnover but it has a lower ebitda margin and higher receivable days. As per the concalls, the management has expressed their desire to hive off the battery biz at various times. Nothing has been done as of today.

Except the above two, there are no other negatives which I could see in the company

Cash conversion is healthy. CFO/Op. EBITDA 0.77x for past 10 years avg

There are various marquee names in the shareholding of TTL. HDFC holds 9% stake. I will leave upto you guys to figure out the other names ![]()

Before 3-4 years, the company did a QIP at 95-96 per share. Not posting details of products here as lot of information is available in their investor presentations.

Happy to know about your views ![]()

3 Likes

Media Release regarding receiving approval for Fully

Wrapped Carbon Fibre Reinforced Type-IV Composite Cylinders for CNG Cascades.

Company had been working relentlessly for the last 3 years for developing Fully Wrapped Carbon Fibre Reinforced Wrapped Type-IV Composite Cylinder (No metal) for CNG Cascades. We are pleased to inform that Company has successfully developed and has finally received coveted approval from Petroleum And Explosives Safety Organization (PESO) (formerly CCOE) and Bureau Veritas under International Standard ISO: 11119-3:2013 as applicable. This is the first time in India that locally produced Type-IV CNG Cylinder has been accorded this approval for CNG Cascades. This puts Company amongst top 5 manufacturers worldwide (nearest South Korea and Norway) who have necessary approval for Carbon Fibre Type-IV Composite Cylinders for CNG Cascades.

…

It is estimated that the present market for CNG Cascades in India is around Rs 600 - 800

crores per year with high double digit growth. With PESO approval in hand, Company will

aggressively participate to tap significant market share in India and explore large export

potential.

Additional Media Release clarifying usage of

similar CNG Cylinders for On Board Application (Cars, Trucks, Buses, Three Wheeler etc.).

The Cylinders are in advanced stage of formal testing / approval by Petroleum And Explosives Safety Organization (PESO) and Bureau Veritas. Company is expecting the necessary approval to be in hand not later than 31** December, 2020.

…

Company shall be the only producer of Type-IV CNG Composite Cylinders in India for On Board

application.

Several automotive companies have evinced interest in Carbon Fibre Reinforced Type-lV Cylinders

as a replacement for Steel Cylinders owing to several technical and operational advantages (75%

reduction in weight, EXPLOSION PROOF, Corrosion & Rust free, etc.)

1 Like

In today’s board meeting, company reduced the vesting price of outstanding options from 93.58 to 43. For doing this, isn’t a shareholder voting required (special resolution)? If anyone with relevant expertise can clarify this, it will be great

1 Like

As per my understanding, shareholders approval is required, what they said is board has given approval to put this resolution in front of shareholders for voting.

We will find it for voting in sept.

1 Like

This resolution wasn’t passed with both majority of promoters and institutional shareholders voting against this resolution.

5 Likes

JM financial and it’s subsidiaries have released about 5.35% of the shares in the nature of encumbrance from the total holding of 8.5% that were held as collateral.

Would this be a good news for the company & promoters as this could reduce the pledged % ?

I’m confused and don’t understand how to interpret this.

JM Financials sold 5.35% of pledge shares or released pledge shares?

From whatever knowledge I had , I could interpret it like Financing institution have given back the part of held shares as collateral back to the promoters if I have to put it in simple terms based on the below pointers mentioned:

I. These shares were held as collateral to secure the loan sanctioned / given to the borrower(s) as on October 23, 2018.

II. These shares were held as margin from the clients as on October 23, 2018.

III. This disclosure is made since the release of encumbrance (gross) on shares exceeded the threshold limit for disclosure

on December 21, 2020.

IV. These shares are held as collateral to secure the loan sanctioned / given to the borrower(s) as on December 21, 2020.

I could be wrong so wanted to get the perspectives from this group as well to check for my understanding on this disclosure.

1 Like

Last Month, the company had published Update on Promoter pledge and loans (outstanding)

…

Promoter Group Companies namely i) Time Securities Services Private Limited ii) Vishwalaxmi Trading and Finance Private Limited that both the Companies have repaid loan of Rs 20 crores (Rs 10 crores by each) to lender out of Rs 70 crores loan (Rs 35 crores in each), after repayment the balance principal outstanding of loan stood at Rs 50 crores (Rs 25 crores in each).

…

We also have been informed by both Promoter Group Companies that pledged shares will be released (partly) based on current market price and principal outstanding loan.

JM Financial mentions the Mode of Sale as “Release of encumbrance”. Seems like it’s a release of pledge and not a sale

1 Like

Hi, have any about market potential of TCP’s new product CNG cascade and new USA plant?..

I think the capex for the new USA plant is ~USD15mn. My view is it won’t impact the revenues by any significant percentage.

About the new product CNG cascade, it will take time to ramp up and all. They have given the market size etc on the concalls, you can check there.

Disc.: Exited

If you are into plastics industry, its better you check the flexible packaging films industry. Available at good discounts vis a vis the rigid container/rigid packaging stocks such as this.

The Indian flexible packaging industry has grown at more than 15% for more than 10 years in the past. The growth is expected to accelerate in future given the increase in consumption of flexible plastic packaging against cardboards/metal/glass packaging. Also, the online market (packaging used by Amazon etc) is fueling the demand of the flexible plastic packaging

The flexible packaging industry might be growing at only 5-6% globally, but in Asia (more in the developing economies), it is growing at a much faster pace due to the lower per capita consumption of flexible packaging in the developing economies than the developed economies.

2 Likes

Just started researching Time Techno Plast. Starting with past numbers as the company has been listed for a long time. The Cash flow from the firm is disappointing and doesn’t inspire any confidence to research further.

Here are my observations just from the numbers:

Low Revenue growth rate of 7-8% between 2015-20.

In the meanwhile Net Working Capital doubles while revenue only goes 1.45 times.

Cumulative Net Free Cash flow to owners (CFO-Net Capex-Interest payment) is -2Cr. over the period of 6 years. This firm has not generated cash for its owner in 6 years.

Bondholders enjoy all the capital generated by the firm.

Did a share issuance in 2017-18 at a very elevated level. Good for the firm, bad for the shareholders. There has been a negative return to the shareholders from there on.

I am just looking at the past numbers, past numbers are no guarantee for future performance. I don’t have any insight into the industry and just beginning my research on Time. However, the numbers don’t inspire any confidence. Let me know if I’m missing any key links.

2 Likes

Yes, as you rightly pointed out the past numbers are no guarantee for similar future performance.

What TT is banking on is their new products, which they have developed over the the last 2-3 years, please go through their concall.

Currently all the major OMC are using steel cylinders which are highly hazardous imagine the demand once the OMCs start consuming the composite cylinders

CNG cascade and CNG Type IV Composite cylinder as huge scope

PowerPoint Presentation (bseindia.com)

TIMETECHNO Stock | Time Technoplast Ltd Q3 FY21 Earnings Call - YouTube

2 Likes

I have a different view. company generating substantial owners earnings compared to the market valuation.

Management have acknowledged this issue and guided to correct this in next three years

That is because they are re-investing owner’s earnings back in to business for growth.

I think this was a good decision.

very big opportunity ahead for this company… This is the only CNG cascade supplier in india… Very few companies are manufacturing CNG CASCADES globally…

3 Likes

How important are Cascades for a CNG filling station? Should they not be able to operate without one?

Also Supreme has the same type 4 cylinder product, maybe longer than Time, but no sales bump. More competition coming in soon possibly.

Will OEMs replace steel with plastic soon? They need to consider their product need and may not be able to just swap one for the other.

Disc: not invested

Each CNG Filling station require 3 cascade vehicles, one at station, one in Transit & one at CNG plant.

Supreme has LGP cylinder which is low pressure type, CNG cylinder is high pressure type, only two players manufacture that in the world.

Disc.: Invested heavily at lower levels

5 Likes