Time Technoplast – Market Overreacting to Tariffs?

US Tariff Concerns Eased: Despite market jitters, management has clarified that US tariffs have no significant impact on operations. Additionally, Trump has announced a 90-day pause on tariffs, offering India time to negotiate a deal.

Localized Manufacturing in US: Time Technoplast manufactures Intermediate Bulk Containers (IBCs), QT Drums & PE Drums through its Houston (USA) based subsidiary Core Plastech International, effectively hedging against tariff risks.

Strong Global Position in IBCs: The Group is the world’s third-largest manufacturer of IBCs, marketed globally under the GNX brand. IBCs are a value-added, eco-friendly, and reconditionable product with global demand.

Cost-Efficient & Scalable: IBCs offer space efficiency and durability, making them a preferred solution in industrial logistics and storage. They contribute meaningfully to the company’s value-added product portfolio.

Positive Outlook: Tariff headwinds appear to be overestimated by the market. Strategic US presence and global demand for IBCs position Time Technoplast well for long-term growth.

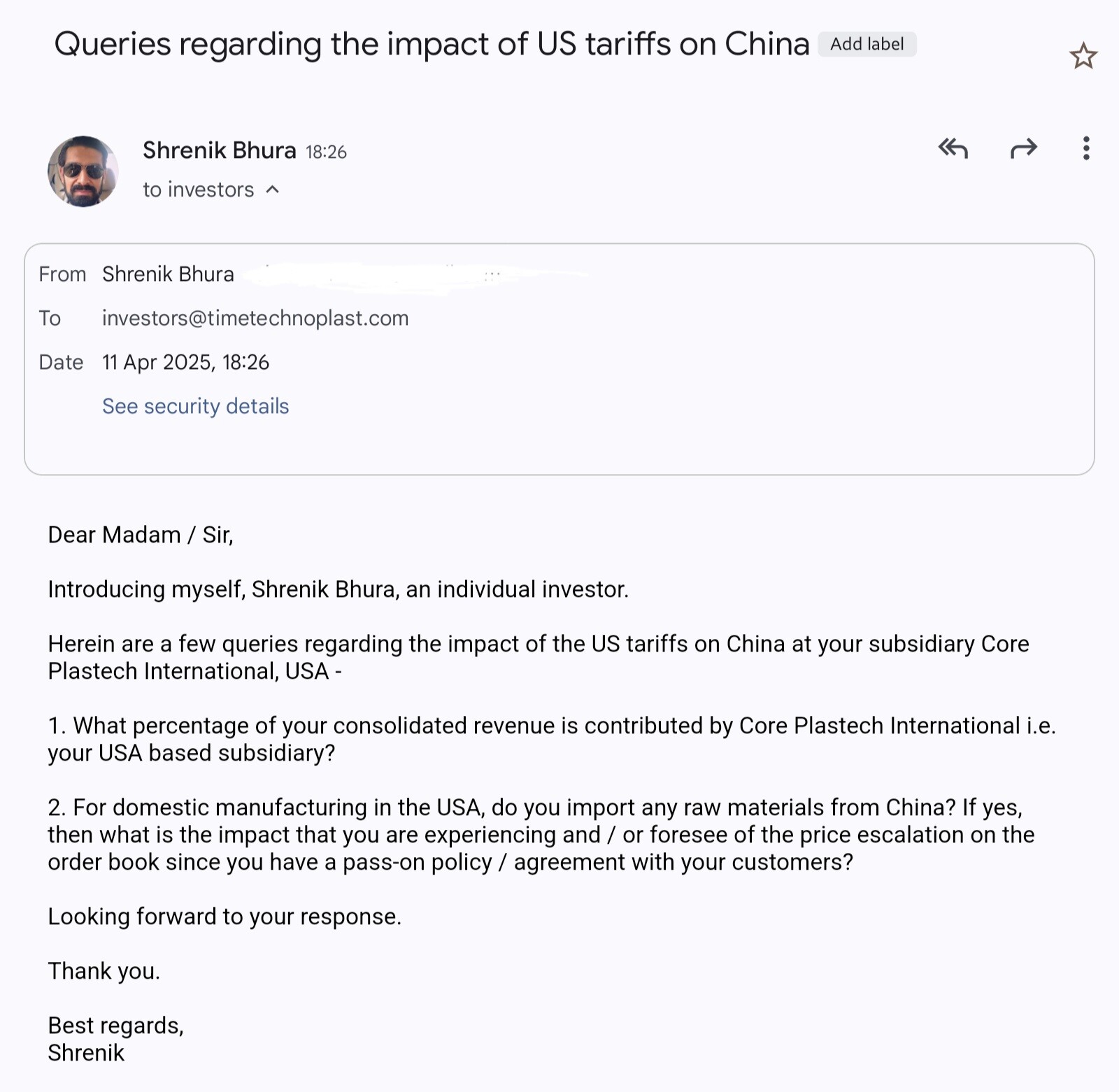

Thanks for the information. Have 2 queries :

i) For the Localized Manufacturing in US, do they import RAW material from China?

ii) Since the Crude oil prices have fallen sharply, does it impact it’s revenue numbers? Means Revenue will decrease but profit and volume of sale will increase?

Can anyone please help in answer this query..

Thanks

IBC demand is bound to be affected in this tariff turmoil. Yearly export of China to US is more than 700 billion $. How much of this is now affected is anybody’s guess. May be more than 80%. The 10% uniform traffic will certainly affect traffic. And after 90 days, what will happen? All these are not good for trade. So in the short term performance will be affected despite assurances of management and falling crude price.

To understand the raw materials used by Core Plastech International for their Intermediate Bulk Containers (IBCs), we first need to consider the general materials used in IBC manufacturing. IBCs are typically made from a combination of materials to provide structural integrity, chemical resistance, and ease of handling.

Common Raw Materials for IBCs:

High-Density Polyethylene (HDPE): This is the primary material for the inner container (bottle) of most composite IBCs. HDPE is chosen for its excellent chemical resistance, durability, and suitability for blow molding.

Galvanized Steel: Used to construct the outer cage that provides structural support and protection to the inner plastic container. Galvanization prevents corrosion.

Polypropylene (PP): Sometimes used for components like valves and fittings due to its chemical resistance and strength.

Steel (various grades): For rigid IBCs, stainless steel (304 or 316/316L) or carbon steel can be used for the entire container.

Composite Materials: Combinations of steel and plastic are also used to leverage the benefits of both.

Sealing Materials: Elastomers like EPDM (ethylene propylene diene monomer) or FPM (fluorine rubber) are used in valves and closures to ensure leak-proof sealing.

Raw Materials Used by Core Plastech International:

Core Plastech International, as a subsidiary of Time Technoplast Ltd., likely utilizes similar raw materials for their IBCs, focusing on composite IBCs with an HDPE inner bottle and a steel cage. Their product range includes “GNX composite intermediate bulk container (IBC)”. Based on the general knowledge of IBC manufacturing and Core Plastech’s likely focus:

HDPE granules: For blow-molding the inner, chemically resistant container.

Steel tubes and sheets: Likely galvanized steel, to fabricate the protective cage structure.

Polypropylene (PP) or HDPE: For manufacturing valves, spouts, and other fittings.

Sealing materials (EPDM, FPM, or similar): For ensuring the integrity of closures and valves.

Sourcing of Raw Materials from China:

Information specifically about Core Plastech International’s raw material sourcing from China is limited in the provided search results. However, we can make some inferences:

Time Technoplast Ltd. has a global presence: The parent company, Time Technoplast Ltd., has manufacturing facilities in over 11 countries. This suggests a potentially diverse supply chain for raw materials.

General Global Sourcing: It’s common for manufacturing companies to source raw materials globally to optimize cost and availability. China is a major global supplier of plastics and steel.

Indirect Evidence: One search result indicates that Core Plastech International Inc. has imported shipments from India and Singapore. This shows they do import materials, but doesn’t specify if they import from China. Another result mentions a Chinese supplier of PE film.

Based on the available information, it’s difficult to definitively state how many of the raw materials used by Core Plastech International are sourced from China. While it’s plausible that they source some materials like HDPE granules or steel components from China, the exact number and proportion cannot be determined without specific sourcing data from the company.

To get a precise answer, you would need to contact Core Plastech International directly or consult their official reports and disclosures regarding their supply chain.

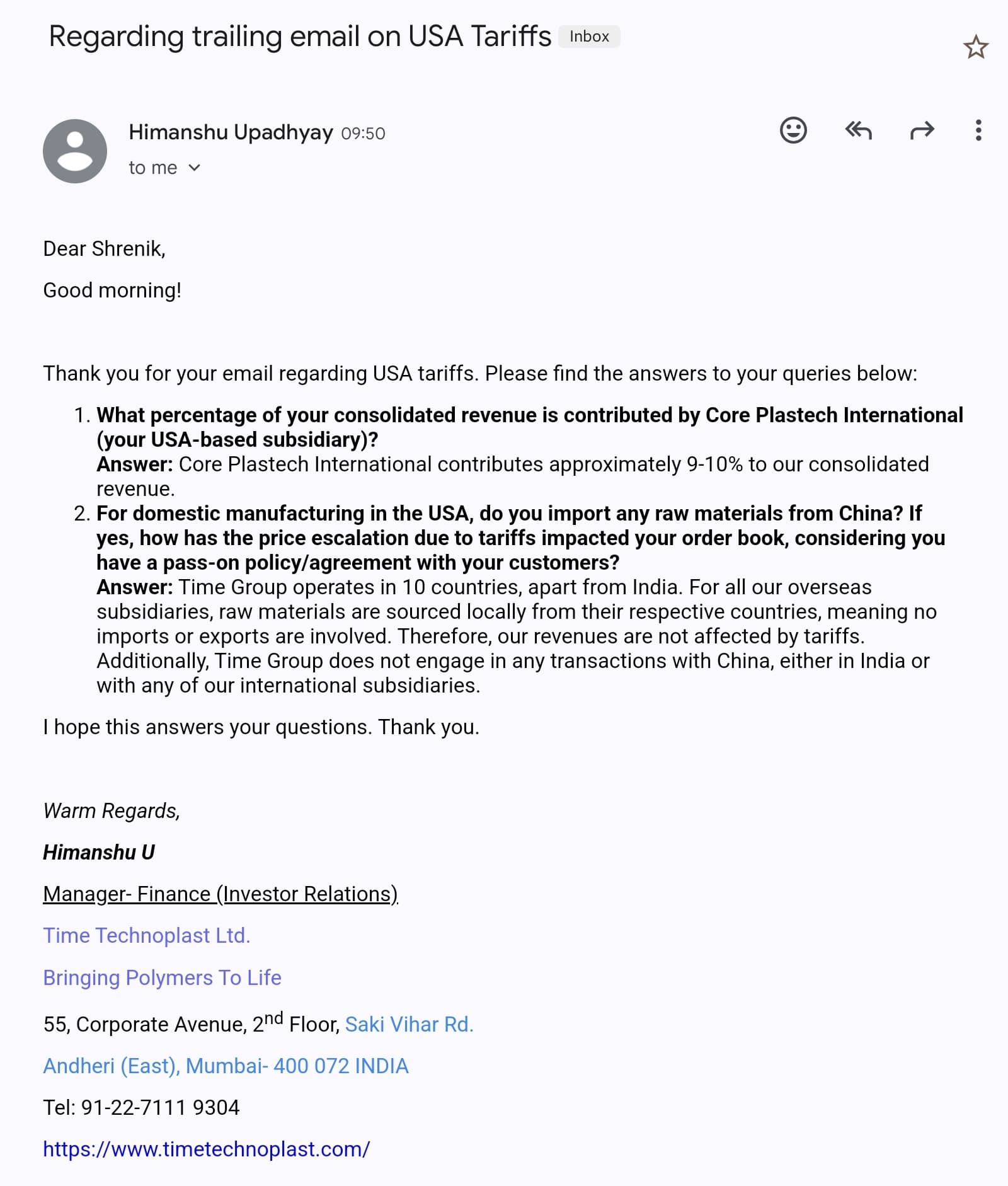

Have written to the investor relationship team requesting an answer -

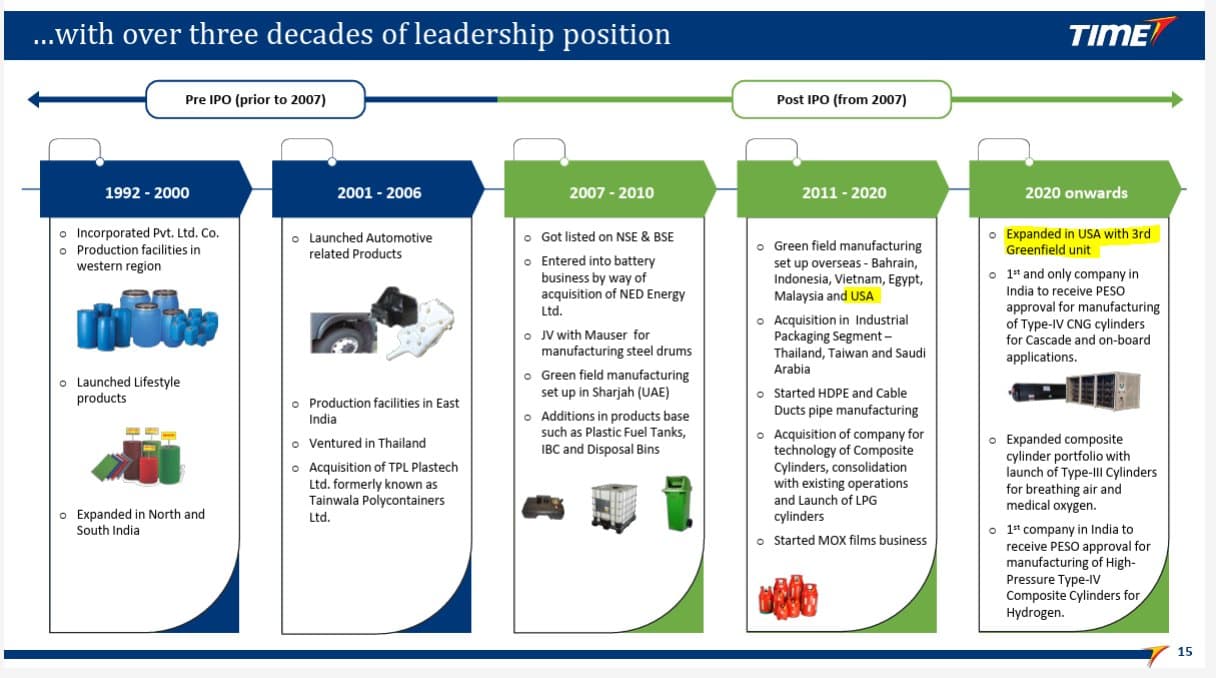

This query has been answered in detail with examples and explanations multiple times in the last concall. Please refer to that. Am attaching a snapshot below for quick reference -

Pls pardon me, generative AI generating too many lines..its how we over analyse.

1.Core Plast doesnt necessarily need PP or Any type of PE Granules from china. USA is leader in both.Rather certain PE grades r imported to china from USA (exxon etc have monopoly in many specilised binder,tie materials used to bind/tie two layers of plastics at a time of molding/extruding). Reliace has pretty much competitive priced granules,they also offer discounts.they likely imported from India bt granules r readily available in USA.

IMO - None/Negligible tarrif impact for US operations.

2.Crude down means downstream petrochems r down(COGs of IBC down) means margins UP.

Time Techno has a major role to play in the energy supply chain as it provides storage infrastructure. Stock price can be delusional but the company has solid value intact with no deviation by the owners hence sticking to the story. Energy requirement is only going to increase. Like drone hydrogen cylinders , portable type 4 cylinders for various usage etc. Entire LPG supply chain is still dependent on metal cylinders which has to change.

I have been tracking it to fall close to or below 50 WMA which it has now. It is a more comfortable price for new entry and addon. Fundamental wise its not expensive at all.

Time Technoplast Ltd. has launched a new subsidiary, Time Ecotech Private Limited (TEPL), focusing on recycling and reprocessing industrial plastic packaging. Incorporated on May 9, 2025, with an authorized share capital of ₹25 Crores and a paid-up capital of ₹50 Lakhs, TEPL aims to support India’s circular economy. Time Technoplast plans to invest ₹120 Crore to set up four automated recycling plants across India, processing 60,000 metric tonnes of plastic waste annually. This strategic move positions the company as a leader in sustainable waste management.

From setting up a subsidiary to getting approvals for products globally, a lot of things are coming together for Time Technoplast.

There are times when promotors go on front foot & define the next leg of growth for businesses. Time Technoplast just seems to be falling into that bucket.

The difference between a fund manager and an individual investor is huge, they are paid to churn money, which they call managing money. You have an advantage here: the stream of products is increasing, brand equity is building, and there is a current market downturn which means you are getting your pizza cheap. Why will you sell now if you already own? The best time to sell was technically in stage 3, not late-stage 4 or stage 1where it is at right now.

Had a 13% volume growth while only 9% sales growth, due to lower raw material prices.

The strongest performer was CNG composite cascade segment with a growth of around 28%.

In composite cylinder they have an order book for approximately 185 crore and 445 crores in domestic and international market in industrial packaging division.

Sold more higher value products which lead to higher margins with a total contribution of 27% in the total sales which they want to bring to 35% in the next 2-3 years.

They have got approvals for Type 3 cylinders and have been sent to drone manufacturers for testing. Type 4 cylinders also have approval however commercial production will start after CNG plant expansion is completed. Commercial production in the expanded plant was delayed due to approval issues and geopolitical tension and now will start production in Q3FY26 and will also cater to production of hydrogen cylinders.

CNG Capacity expansion from 480 to 1080 cascades and revenue potential of 800 crores from 350 crores.

Expect a 30% growth in the cascade business (CNG+LPG) vs 10-12% in their other business due to the lower base with a target of 1500 crores sales (CNG + LPG + Hydrogen) within 3 years.

Long term target of 2500 crores sales from composite products in 5 years

Expecting a 20-30 bps improvement in margins until they achieve the target of 15.5% margin in 3 years. This will happen as the high margin product share will increase going forward. Still committed to be debt free in 2 years.

They achieved 18% ROCE this year and aim for 20% next year.

Middle east is 30% of their total revenue. They plan to cross sell steel drums to their existing customers who require them. Steel drums have a 5x revenue per capital employed albeit with lower margin while plastic ones have 2.5x

Capex would continue to be below 200 crores - 80 to 85 crores of maintenance capex while 120 crores for new products in LPG and CNG, etc.

The delay in order from IOC for 14.2 kg composite LPG cylinders was due to change in the leadership at IOC.

The existing order of 10kg cylinder is progressing while the delay is on 14.2 kg cylinders

They expect order visibility and capex in H2 of the year. The QIP is also tied to how the approval happens. Capex for the bigger size cylinder will take 4-6 months.

They are also exploring exports in Kuwait, Saudi, Oman and have started supplying in Taiwan

Receivable days split - 45-60 days for composite products while 75 days for packaging products and PE pipes. Average receivable days is 69 days

They are H2 heavy business with a 45:55 split in the business between the two halves.

The non core assets which they plan to sell include land parcels worth 20 crores, small businesses which are not atleast having a revenue potential of atleast 40 crores

Sale of e-Rickshaw to start from H2 of the fiscal with an expected sales of about 30 crores with a focus on aftermarket rather than OEMs. The TAM for the battery market is about 5000-6000 crores and since the life of these batteries is 1-2 years, it is a repeat business.

Thanks for the details @Naman_Gupta1 . I see that the recording is uploaded in timetechnoplast website. However may I know how you are getting the transcript of this so soon? From which website?

As Gyanesh told. I use notebook lm for transcript.

Also since they are not that good. So I also listen to the concall side by side pause and note down anything which I feel is important.

Thanks @Naman_Gupta1 and @GYANESH - I have been using NotebookLM to upload transcripts in PDF or by extracting transcript from Alphastreet Youtube channel. But never thought of downloading MP3 concalls and uploading in NotebookLM. This is great for immediate checking after concalls!

Personally I like the tool NotebookLM, seems providing good enough responses.

Al-together seems Time Technoplast has a good future! The next real trigger can be the announcement of approval of 14.2 Kg LPG composite Cylinder!