Sorry if I’m asking this again. What’s the difference between Sales growth and Volume growth? What’s the interpretation here and why are those numbers different? If you can explain please with an example. Thank you.

Sales Growth = Volume Growth + Price Growth

If a company raises prices but sells the same quantity, sales will grow, but volume won’t.

If a company sells more units at the same price, both sales and volume will grow.

If the company sells fewer units but at a higher price, sales may grow while volume declines.

Basically we are trying to gauge the reason as to whether its a volume led growth or not (to some extent)

18 Likes

Q3 FY25-

Topline decline bcz of reducing raw material prices and as per their policy they pass on both price hike and price fall to end customers, so revenue decline, but guiding for Volume growth of 18%.

VAP currently- 25-27%, will take it to 35% in next 3 years.so after 3 years OPM will become 15%

OPM range- 18-22%,but guiding 18%

Become net debt free in next 2 years

Composite hydrogen cylinder used in Drone, lighted than battery

Capex- 200cr bifurcation-

Started making E- ricksaw batteries-

Screenshot 2025-02-18 143147.png 128.67 KB

Screenshot 2025-02-18 143121.png 156.17 KB

IOCL started using name - INDANE LITE for composite cylinder that we used in our home, it will replace Metal cylinder-

****Also started making Composite Fire Extinguisher.Huge opportunity here.

17 Likes

Q3FY25:

• The Company has committed to transform 75% of its electricity consumption to green energy within the next two years by tie up with solar power generating Companies. This transition will not only result in cost savings but also contribute to a significant reduction in carbon emissions.

• Company had identified non-core assets for disposal with an estimated realization value of Rs. 125 Crores (approx.) which has now reduced to Rs. 51 Crores being balance amount already realized,

• Our subsidiary i.e. Power Build Batteries Private Limited has developed a low cost, high-performance E-Rickshaw battery in the brand name of “e-START with SELENIUM”, With advanced lead-acid technology and enhanced with selenium, these batteries offer superior performance, safety and efficiency.

• Debt Equity Ratio - 0.23

• Total Debt reduced by – 9MFY25 – 92.5cr

• 33% Composite Cylinders growth (CNG) – 9MFY25

• ₹ 435cr Confirm Tender received for Supply of Packaging Products

• ₹ 160cr order book- PE Pipes

CONCALL NOTES:

• Our internal trial for the drone application is on with tie-up with some of the local company so that we can prove the results of the hydrogen Type-III cylinder for the application and use in the drone.

• We are not reducing any kind of our guidance for the period ahead as targeting to growth in the range of volume growth,

• VALUE ADDED PRODUCTS MARGIN: We are quite comfortable as far as EBITDA margin in the range of, I say, 18% to 22%. And you know very well the volume will justify the prices in market. We have the first mover advantage. We are the first company in India. So, we have the first mover advantage. So, when my volume increase, I will definitely offer competitive prices and we’ll able to maintain our EBITDA margin, which currently we are getting.

• LPG CYLINDER DEVELOPMENT:

o We have been asked by the government authorities, oil gas marketing companies (All 3 – BPCL, HPCL, IOCL) to develop the cylinder of 14.2 kg, which is equivalent to the metal cylinder, which is presently in population. Currently in market, 50 crores metal cylinders are present for 14.2 kg size and current ongoing active connections are 32.68 crores. The government do not want the differentiation between the metal cylinder and the composite cylinder. So that process is under development. And development will be completed in the next 4 to 5 months’ time. (By March, the approval of the design will be taken place then the 4 months will take the tool development. We estimate in the first half, ready with the tool development and everything. The second half will be available for the supply and commercial supply.)

o By that time, we’ll need the expansion, looking to the requirement of the government company.

o 75% growth in composite LPG cylinder us according to IOCL internal reports.

o Every year, government is buying 6% of the total population cylinder, which is in the range of 2.5 crores to 3 crores cylinders they are buying every year. And again, current capacity of we and Supreme together is less than 2-million-cylinder capacity which is less than 10% of the total requirement of the yearly requirement.

o So, as this product is approved, we have ourselves keep ready for QIP because then the major investment is required, looking to the size of the tender of each oil marketing company

o We have taken 4 countries, another under approval. That’s called one is in Kuwait, second is in Saudi, third one is Oman and Sudan. Those 4 countries, we have submitted our sample of approval and we estimate to get the approval in the next 3 to 4 months’ time.

• CNG Cascade expansion will be completed by Q1FY26 (delayed by 3-4 months).

• CNG AUTOMOTIVE APPLICATION: When the capacity expansion will come, we have already started groundwork with the automotive companies, OEMs directly, what types of the requirement they will have, various sizes for them depending on their vehicle sizes they need. So that development is already ongoing, but it is the initial stage of drawing level. We will develop the tool based on their individual vehicle requirement. But we are sure that currently, wherever they are using the metal cylinder, there it is going to be replaced in the next, I can say, 2 to 3 years’ time by way of a CNG composite cylinder plus hydrogen cylinder because hydrogen cylinder is also overseas countries, many countries are using hydrogen cylinder, which in India ahead of that, but we have the first mover advantage.

• PE pipe business was affected this quarter because of uneven rains during the quarter. I had estimated growth of 30%, but I’m able to get only 10%.

• GREEN ENERGY AND COST REDUCTION: 30 to 35 savings in energy cost through solar power. Current consumption is 18cr units. Assuming 75% conversion (13.5cr units) and 2.5rs per Unit savings.

• I have a very clear guidelines from my committee and my Board. If any investment we justify a payback period within less than 3 years, keeping the eye close, we should make the investment.

• 17% to 18% growth in the Middle East to MENA region. Around 14%, 15% growth in the U.S. and the Southeast Asia, 8% to 9% growth in Taiwan. So combined overseas business, it is expected to grow at 15%.

• E-RICKSHAW BATTERIES: Today, the 15 lakhs E-Rickshaws are available in the market as of 2023. And every year, 4 lakhs new rickshaws are coming, E-Rickshaw. And each rickshaw needs 4 batteries. And the cost of the battery is less than INR10,000. So, in terms of the revenue, I can say the market size, which is 2024 is INR2,500 crores, which is growing every year by INR600 crores, because every year, we will find 4 lakh rickshaws means 16 lakh batteries. So, what we are projecting, we are now very much eager, but we are targeting to have in the 3 years down the line, we would like to have INR100 crores business from E-Rickshaw market. That’s what our team is targeting considering the quality of the batteries and the very good performance of the batteries.

We have estimated to launch this product at the end of the March. So next year, 2025-'26 with the existing capacity, we are estimating to take the business of INR50 crores from this battery itself.

• COMPOSITE FIRE EXTINGUISHER DETAILS: We are manufacturing these composite cylinders for fire extinguisher and then this will go to the companies who are filling the chemicals in this and making a complete fire extinguisher supplying in the market. So, BIS is required for a complete fire extinguisher not on the cylinder only for the fire extinguisher. So those companies will take the BIS approval on the fire extinguisher and supply in the market. We have already submitted the samples to these companies, which they have tested and found these cylinders were compatible with their requirement. And now they have submitted the application to BIS, which takes about 3 to 4 months’ time for the approval. So, once they get the BIS approval, we will start the supplies of these cylinders.

It is a huge market.

THINGS TO TRACK:

• CNG CASCADE DEMAND: Will demand get hurt by recent developments regarding reduction in APM gas to CGD’s? Or will the trend of conversion of steel cylinders to composite cylinders continue? How will Supreme Industries entry into this segment play out?

• LPG 14.2KG CYLINDER PROGRESS

• PROGRESS OF NEWER PRODUCTS: Drone application, fire extinguishers, water heaters, oxygen cylinders.

• PROGRESS OF AUTOMOTIVE APPLICATION

• RAMP UP NEW CNG CYLINER CAPACITY

10 Likes

The LPG 14.2kg cylinder could be a game changer for TTPL’s growth trajectory, given that all 3 OEM’s are participating in development and the fact that management has kept a 1000cr QIP enabling resolution ready for capex because the demand could be huge.

4 Likes

I feel this a long shot..i couldnt find any local company doing drone with Hydrogen. is it a proprietary infromation to know this local company ?..anyone aware ?

D - Holding

4 Likes

The management has said they were able to increase the volume by 15% but value growth is 5% which worrying as they passed on the less RM cost to their customers . Company got no moat . how are they going to reduce their debt burden , invest for future capex . dec qtr results big surprise on value growth . QIP will dilute the existing share holders EPS growth

3 Likes

As majority of the company’s business is B2B, fluctuations in polymer (raw material) prices are passed on to the customers. Both increases or decreases. They work on EBITDA per ton basis. So that’s why volume growth is the key metric

The industrial packaging business is indeed a commodity business and here Time’s size, market leadership and scale becomes it’s competitive advantage.

7 Likes

Drone application was and is a long shot. If something/anything tangible comes out of it, then it’s a bonus for us shareholders.

The main growth drivers would be CNG cascade & automotive cylinders and LPG cylinders.

Also, fire extinguishers could become big (But again too early there)

Composite gas heaters have a lot of potential as well

What is heartning to see is that the philosophy of the company is clear and focused. Where can we replace traditional material with composite materials and use our expertise with the composite material to drive innovation and growth.

7 Likes

why its felt there is no moat? the products developed are niche and they have 1st mover advantage. Which are the competitors who has developed similar products like the cylinders?

2 Likes

In addition to this below is snippet from Supreme Industries Q3 con call, which also validates Time Techo mgmt’s statement on same.

Blockquote

Rishab Bothra: Okay. And with respect to the LPG cylinder, I think Supreme and Time Techno are the two

players currently. Are there any other players who are supplying to the composite cylinders?

P.C. Somani: As of now, no.

M.P. Taparia: Not to our knowledge.

Rishab Bothra: And lastly, what is the market size of this cylinder and how much market share do we want to

gain?

M.P. Taparia: Market size is more than 40 million cylinders.

Rishab Bothra: More than 40 million, sir. Thank you, sir.

M.P. Taparia: Our capacity & Time together is not even 2 million cylinders.

Rishab Bothra: So, we want to scale up the capacity in cylinder also quickly?

M.P. Taparia: Capacity will be going on increasing based on the demand coming from the oil marketing

companies.

Rishab Bothra: Okay. I will come back in queue, sir. Thank you.

M.P. Taparia: They have to decide how much they want to switch over from the metal to plastic.

Rishab Bothra: Okay.

M.P. Taparia: Plastic is safe material. As we saw yesterday in Kumbh Mela, the explosion took place because

it was metal cylinder. Plastic cylinder would not have exploded. It would have burned out. The

damage would have been minimal.

Rishab Bothra: So, will lobbying help and consumer awareness for marketing companies help?

M.P. Taparia: Only by the oil marketing companies…

Rishab Bothra: Okay. Thank you.

12 Likes

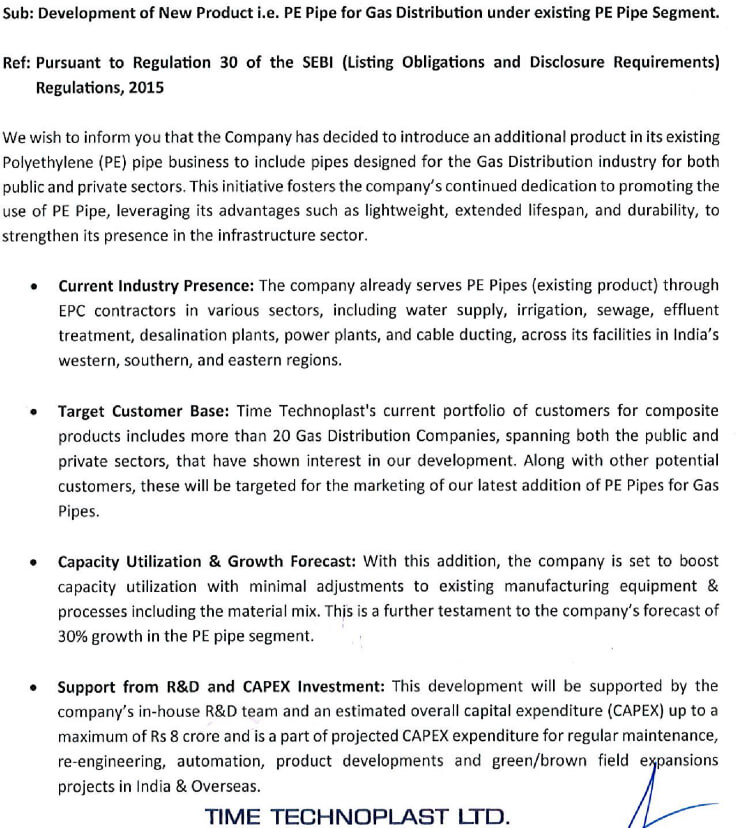

Time Technoplast

Replacement of traditional PE pipes for enhanced durability beneath roadways

PM Ujjwala Yojana : Smart city projects

Innovative and keeps slogging

12 Likes

What is this ?

Talking concall things …like summarizing concall in US accent.

All Rosy and pretty much generalized statements… “they are accellerating growth, massive expansion, debt-free by 26…talking about risk mitigation and talked about systems in place to identify potential threats”

Is this AI audio made out of concall transcript?

@Gautam_Chopra , Django bhei…what do you make out of this video ? what are the news towards topline growth, any topline numbers for FY26 ?

D-Holding

Notebook LLM summarizes and turns it into a podcast.

VAP currently- 25-27%, will take it to 35% in next 3 years.so after 3 years OPM will become 15%

OPM range- 18-22%,but guiding 18%

Become net debt free in next 2 years

This should be easy to track. Rest new products are anyways being announced, so track BSE annoucements

3 Likes

Time Technoplast -

Q3 FY 25 results and Concall highlights -

Company’s products -

Polymer products like - Drums, Jerry cans, Polyethylene pipes, turfs and mats, disposable bins, MOX films, steel drums

Composite products like - Intermediate bulk containers, composite cylinders, Auto parts, energy storage devices

Out of the products listed above, the value added product segments include - Intermediate bulk containers ( IBCs ), Composite CNG,LPG cylinders and MOX films

Established products include - Drums, Jerry Cans, auto components, air and hydraulic tanks, their Lead - Acid batteries, door mats, PE pipes. Their batteries are used in Telecom sector, railway signalling and other Industrial applications

Q3 FY 25 outcomes -

Revenues - 1388 vs 1325 cr, up 5 pc

EBITDA - 201 vs 191 cr, up 5 pc (margins 14.6 vs 14.5 pc)

PAT - 102 vs 93 cr, up 10 pc

India volume growth @ 10 pc, International Volume growth @ 15 pc

India : International revenues @ 64 : 36

Value added products grew by 13 pc while established products grew by 2 pc YoY ( in volume terms )

Polymer : Composite products revenues @ 63 : 37

Polymer : Composite products margins @ 13.9 : 15.7

Established : Value added products revenues @ 71 : 29 ( for 9M FY 25, this ratio stood @ 73 : 27 )

9M FY 25 highlights -

Revenues - 3991 vs 3601 cr, up 11 pc

EBITDA - 574 vs 507 cr, up 13 pc

PAT - 278 vs 218 cr, up 28 pc

For 9Ms, VAPs grew by 17 pc and established products grew by 9 pc ( in volume terms )

Reduced Gross Debt by 92 cr in 9Ms

Net Cash from operating activities in 9Ms @ 285 cr

Capex spends for 9Ms @ 150 cr

Confirmed orders received for supply of packaging products @ 435 cr. Order book for Composite Cylinders @ 175 cr. Composite cylinders grew by 33 pc in 9M FY 25

Developed and launched E-Rickshaw batteries under the brand name - ’ E Start Selenium’. Addition of Selenium to lead acid batteries improves their performance meaningfully

The Company has committed to transform 75% of its electricity consumption to green energy within the next two years by tieing up with solar power generating Companies

The Company has made a strategic decision to consolidate its products and manufacturing units. This includes Brownfield expansion and adding New Units, which will better align with evolving market demands

Have got India approval for supply of HP Composite cylinders for UAVs / Drone applications

Company has manufacturing plants across India, UAE, Egypt, Saudi, Bahrain, US, Taiwan, Indonesia, Malaysia, Vietnam, Thailand, Bahrain

Breakup of company’s overseas business between ME, SE Asia, US stands @ 30 : 50 : 20. Confident of growing the total International business @ 15 pc kind of rates for foreseeable future

Topline growth for 9Ms, 3Q has been lower than volume growth because of reduction in RM prices

28 pc jump in PAT in 9Ms led by reduction in finance and depreciation costs

To continue to reduce Debt going forward

Have secured an approval to raise 1000 cr via QIP ( equity ) - aimed at reducing debt + capex. The approval is valid till 27 Nov 25

Aim to keep growing volumes @ 15 pc for foreseeable future

Composite Cylinders that company makes are for - LPG, CNG, Oxygen, Hydrogen

Company aims to be Debt free in next 12 - 18 months. They currently have a debt on books of 700 cr

Time Techno and Supreme Industries r the only 2 govt approved suppliers for LPG cylinders

In next 3-4 years, company expects all the CNG cylinders in the Auto sector to be replaced with composite cylinders

Expecting substantial pickup in demand for PE pipes ( mostly used for sewage and drainage applications ) from the Govt sector in Q4 ( as the Govt capex picks up )

Over medium term, company expects its packaging products to keep growing @ 10-12 pc while composite products to keep growing @ 30 pc

Company expects the VAP share of total revenues to reach 30 pc vs 25 pc currently ( over next 3 yrs ). That should help the company post > 15 pc EBITDA margins on a consolidated level

Once company transitions bulk of its energy consumption from renewable ( solar ) sources, it should help them save 30-35 cr / yr

Currently, total no of E-Rikshaws on Indian roads are aprox 15 lakh. Yearly addition to this number is to the tune of 3-4 lakh / yr. Each E-Rikshaw uses 4 Lead - Acid batteries costing aprox Rs 10k each. Clearly the Mkt size of E-Rickshaw batteries is huge and expanding rapidly. Company aims to clock 100 cr kind of annual sales from this segment in next 3 yrs. EBITDA margins in this segment should be around 12-13 pc

The metal cylinder used in households for LPG supply is of 14.2 kg. Currently, the company is supplying 10 kg composite cylinders as its replacement ( currently supplying to IOC + BPCL + HPCL ). These composite cylinders are growing > 50 pc CAGR. Company has now been asked to develop 14.2 kg cylinders by the Govt Oil Marketing PSUs. Should be able to start supplying these in H2 next FY. Once 14.2 kg cylinders r approved, the growth rates in this segment should increase further !!! Company may also be required to undertake capex for the same. The QIP money should then come handy

The difference between volume growth vs EBITDA growth ( former being higher than the latter ) is because of inventory losses that company has had to bear because of fall in RM costs

Composite Fire extinguisher cylinders is another good opportunity for the future. The light weight benefits should really help them replace the existing metal - heavier cylinders at a rapid pace. Plus the Chemicals used in fire extinguishers corrode the metals. So, use of composite material has two fold benefits

Company believes that piped gas connections are not a long term threat for their business as it’s not economical to supply them in Individual houses. They r economical only for flats in a high rise buildings

Disc: holding, added recently, biased, not a buy / sell recommendation, not SEBI registered

14 Likes

In the last couple of days promoters have bought shares worth Rs 3.8 crores from open market.

5 Likes

Another market purchase of around 1.10 crores

5 Likes

Revenue Outlook

The company anticipates a 15% annual volume growth over the next three years, fueled by packaging (10-12% growth), composite products (30% growth), and PE pipes (30% growth).

The composite segment, which includes LPG, CNG, and oxygen cylinders, is expected to witness robust expansion, targeting ₹22bn in five years.

Margin Improvements

The firm is focused on raising EBITDA margins by 25-30 basis points per year, with a long-term goal of reaching 15.5% in five years.

Composite products, which currently yield an EBITDA margin of 18%, will be a crucial contributor to margin expansion.

Composite Cylinder Opportunity

Government programs to phase out metal cylinders in favor of lightweight, explosion-resistant composite cylinders (LPG, CNG, and oxygen) offer significant potential.

The LPG cylinder segment alone demands 3 crore replacements yearly, whereas the current composite production meets only 6-7% of this demand.

Industry Trends

India is expected to have 30,000 CNG stations by 2030, doubling from 15,000 currently. Government incentives promoting CNG vehicles are projected to drive higher cylinder demand.

Expansion in Capacity

The company is scaling its CNG cylinder production (36,000 units) by Q1FY26E and is set to ramp up LPG cylinder manufacturing post-approval for 14.2 kg cylinders in late FY25.

Geographical Growth

New production facilities in the US (Georgia) and Belgium will bolster international sales, which are already expanding at a 15% annual rate.

Automation Initiatives

Technology investments are aimed at enhancing productivity by 10%, minimizing costs, and improving profit margins.

Optimized Working Capital

Working capital days are projected to decline from 120 days to 90 days.

The firm aims to be debt-free in two years, using internal accruals for a ₹2bn capital expenditure plan.

Note : Supreme Industries dominate the composite LPG cylinder market apart from our Time techno, with stringent regulations creating high barriers to entry.

The company is also a leader in IBCs, benefiting from strong global branding and quality-focused operations, reducing risks from new competitors.

16 Likes

The stock broke out of the 40 WMA in May’23 and never came close to even retesting it. It has always shown tremendous resilience bouncing back from every price shock over the past year. Things have changed technically now. Had been surfing the 40WMA since mid Jan’25 and now the tariff saga has convincingly pushed it below for the first time in over 22 months. Management has come out and reassured that the tariffs has no significant impact but the price action tells a different story. Is the great turnaround story still in tact? Only time will tell.

9 Likes